One of my

(partially) unfulfilled quests is to understand why voters think the

Conservatives are better at running the economy, when the objective

data suggests they are hopeless

at it. A part of the answer is that they use their (greater) airtime

much better than Labour, by repeating a few generally misleading

lines to take over and over again.

All this week the

Prime Minister and ministers have deflected questions about partygate

and instead trotted out the ‘real’ successes that Johnson has

achieved. Often these are straight lies, but at other times they

involve cherry picking statistics. The clearest example of the latter

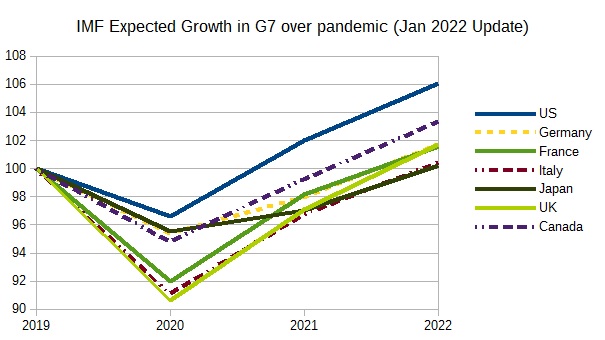

is that the IMF are forecasting the UK to have the most rapid growth

among the G7 this year. This is sometimes linked to a claim that

Johnson has made the right calls over the pandemic.

Here is the IMF’s

latest projection for growth over the pandemic period, where I have

made 2019=100. May contain rounding errors.

It is true that

forecast UK growth for 2022 is higher than any of the other G7

countries. But as the chart shows, all that indicates is that we had

the biggest recession of all the G7 during the pandemic, and so need

faster growth to catch up with pre-pandemic trends. Claiming that

faster growth as an indication that the UK made the right calls

during the pandemic is clearly ludicrous.

However that is not

the point. The point is that ministers and the Prime Minister get

away with misleading the public, because these bogus or misleading

claims are very rarely picked up in any interview. The technique is

simple: make lots of positive claims in an interview about something

other than what the interviewer wants to talk about and the

interviewer will rarely dispute one, let alone them all. Johnson

explains it here.

I first became aware

of this technique in the early Cameron years. Conservative ministers

when interviewed would always claim that they inherited a deficit at

crisis proportions caused by Labour, and therefore they had no choice

but to embark on austerity. Then Labour chose not to argue otherwise,

and I never saw any interviewer question the claim (which was

nonsense on stilts). Together with the right wing press pushing

similar nonsense, the result was a large proportion of voters blame

Labour for austerity.

Today, Labour

politicians understandably talk about the cost of living crisis, but

perhaps they are missing a trick here. Voters do not need to be told

about the cost of living, but they have much less knowledge about

‘the economy’. They will not bother to check the accuracy of Tory

lines to take, and may even think that because these lines go

unchallenged they must be true. As a result, the Tory lead on the

economy may remain

intact. Labour needs to follow the example of the

Shadow Chancellor, Rachel Reeves, who in her recent

speech explicitly focused on how growth had

deteriorated under successive Tory governments since 2010.

Returning to the

Chart above, two points stand out. First, the success story among the

G7 is the US. Only they appear to have got back to something like

where trend growth would be if the pandemic hadn’t happened. The

reason was a large fiscal stimulus, and whether that went too far

I’ll discuss below. Second, everyone has had a (kind of) V shaped

recovery. However with variants appearing just as cases were under

control in many countries, I think the vaccines were crucial in

getting a V shaped recovery.

Without vaccines,

you need regular lockdowns. Even without lockdowns, each new variant

spike will mean many consumers withdraw from social consumption

(travel, recreation, shopping etc). Vaccines gave people the chance

to partially continue social consumption, and largely avoided

lockdowns. It therefore allowed an initial recovery to be sustained.

But is the US really

the success story the chart above suggests, given current 7%

inflation? Did the first Biden stimulus go to far, as some have

suggested? The table below is helpful in this respect.

US Real Personal Consumption Expenditures by Type of Product,

Quantity Indexes (source)

|

2019Q4 |

2020Q2 |

2020Q4 |

2021Q4 |

|

|

Total |

119.929 |

106.418 |

117.023 |

125.303 |

|

Goods |

131.59 |

128.261 |

141.709 |

151.881 |

|

Services |

114.795 |

97.405 |

106.847 |

114.392 |

Note first that the

total hides very different behaviour between consumption of goods and

services. Social consumption is concentrated in services, like travel

and recreation. Both types of consumption fell in the first COVID

wave (2020Q2), but services by much more. From then on, goods

consumption grew quickly, largely immune from the impact of later

waves of the pandemic. (Durable consumption has grown even faster.)

In contrast, service consumption was only just back to pre-pandemic

levels at the end of last year, and it will be interesting to see

what impact Omicron has in 2022.

In our study

of a flu type pandemic ten years before COVID, I assumed exactly this

pattern would emerge. What I didn’t assume, which may also have

happened, is some displacement of social consumption into durables.

As this has been happening worldwide, it is perhaps not surprising

that we might be seeing some inflation in specific goods sectors. One

final assumption I made, which is not unreasonable, is that inflation

would occur just after any pandemic ended as consumers not only

increased social consumption to previous trends, but overshot these

trends initially to partially make up what they had lost.

We don’t know how

much Omicron will suppress social consumption, and whether any new variant waves will be milder or not. At least two scenarios are possible. In

the first, COVID variants become more transmissible but milder (with

the help of vaccines). If this is the case, expect a return to

previous trends in social consumption, with probably a temporary boom

as people try and make good a bit of what they lost. That might add

additional but temporary pressure to inflation. However demand for

goods may plateau or even fall at the same time, relieving some

inflationary pressure from that source. The second scenario is that

new threatening variants continue for a long time, with vaccines

playing catch-up. In that case we may see a medium run shift in the

structure of demand away from social consumption.

Rising world fuel

and food costs have produced inflation in most advanced economies. US

inflation may be the highest because demand there is strongest,

revealing both auto supply problems and reflecting expected house

prices. All of these things are temporary, and price increases over

2021 were unusually

concentrated in particular areas, which does not

indicate persistent inflation. The paragraph above suggests it is

possible that new sources of inflationary pressure may arise if the

pandemic largely ends, but these again are temporary, although

temporary needn’t mean over in a few months.

Temporary inflation

a bit above UK and European levels is a price well worth paying for

output after the pandemic 4-5% higher than most other G7 countries,

including the UK. The only reason not to try and emulate the US in

enacting a strong fiscal stimulus is if you think temporary inflation

becomes embedded in expectations i.e. real wage [1] increases in

excess of productivity gains.

It would be a

healthy sign if interest rates rise a little because Biden’s (now

much more modest) infrastructure plan will maintain demand after all the

pandemic effects are over (if they are ever over). The big danger for

the Fed is if this doesn’t happen, they still raise rates because

of temporary increases in inflation, and the economy dips in time for

political gains for the (now anti-democratic) Republic party.

Just as current US

inflation is unlikely to negate the achievement of having such a

strong recovery from recession, relatively poor performances in most

other G7 countries (UK included) are shown to be a policy choice, in

most part because deficit concerns ruled out a large fiscal stimulus.

Permanently losing a few percentage points of output to the

pandemic is such a bigger cost than temporary inflation at 5% rather

than 7%.

After 2010 everyone

pivoted to austerity outside China, so it was difficult to find a

country that showed its folly. It is a tribute to Biden and those

around him that at least one country has now understood the folly of

worrying about the government’s deficit in a recession. It is the

example of the US that interviewers should mention the next time

Conservative ministers trot out their line to take on the UK

recovery.

[1] By real wages here I mean deflated

by output prices, not consumer prices.