Executive Summary

2022 marks the 50th anniversary of the enrollment of students into the first Certified Financial Planner (CFP) course, and in the years since then, financial planning (and the process of creating a financial plan) has changed extensively. Early on, the ‘financial plan’ was primarily used as a way to demonstrate a prospective client’s ‘gaps’ and needs for products such as mutual funds or life insurance (which the advisor would then be ready to sell to the client). Eventually, as client relationships grew to be more ongoing and less transactional, financial planning grew to encompass other areas of clients’ financial lives, such as taxes and estate planning. Today, the financial plan itself is increasingly becoming not just a ‘value-add’ supporting other services like portfolio management, but rather the whole purpose of (and primary value proposition for) the client relationship to begin with.

In 2018, we released the first Kitces Research study on “How Financial Advisors Actually Do Financial Planning”, which examined how financial planners today are actually executing their financial planning processes, delivering their financial plans, what technology tools they are using, and how they price their services. In 2020, we conducted a second survey to further explore the changing trends in financial planning brought about by improvements in advisor technology, shifts to the advisor business model, and changes in the regulatory environment.

Our 2018 and 2020 studies revealed some surprising insights into how advisors spend their time – namely that for the ‘typical’ financial planner, only about 20% of their working time is actually spent meeting with clients, while over twice that amount (45%) is spent on behind-the-scenes tasks like preparing for client meetings, running financial planning analyses, and managing investments (with the remaining 35% being split between business development and other management/administrative tasks). What’s notable, however, is that the most ‘productive’ (i.e., top-earning) advisors, on average, spent ‘only’ about 10% more of their time on client meetings compared with the least-productive advisors while reducing their back-office work in turn. In other words, by leveraging back-office support, the most-productive advisors added roughly 4 hours per week – totaling around 200 hours per year – on the high-value task of meeting with clients… and nearly doubled their income in the process!

A lot has changed since 2020, though. Most notably, during the COVID-19 pandemic and its aftermath, many advisory firms embraced technology, allowing them to work and meet with clients remotely. Likewise, other developments – such as the implementation of the SEC’s Regulation Best Interest rule and the CFP Board’s updated Financial Planning Practice Standards – have necessitated changes to many advisors’ financial planning processes. And, as always, technology continues to evolve to provide opportunities to streamline the ways advisors provide value (and deepen the value they do provide).

Accordingly, we’re excited to announce the third Kitces Research study, which will once again examine the process that financial advisors go through to create and deliver a financial plan. Following on the themes of the 2018 and 2020 studies, this research will seek to uncover more insights about what distinguishes the most productive advisors from the rest, what factors (such as how they spend their time, what tools they use to support their process, and how they price their services) drive that productivity, and most importantly, what actions other financial advisors can take to improve their own productivity (and consequently, their income and well-being!).

So whether you’re frustrated that your financial planning software doesn’t do what you need it to in order to demonstrate its value, or are simply looking for ideas to refine your financial planning process to be more time-efficient or cost-effective (or valuable and able to command a higher price!), I hope you’ll take a few minutes to participate in this year’s Financial Planning Process survey and help the world better understand what real financial planners actually do!

What Does It Really Mean To Be A ‘Productive’ Advisor?

At the most basic level, ‘productivity’ is a measure of how much output can be produced for a given level of input. Factories try to become more productive by engaging in process improvement to gain efficiencies and produce more ‘units’ from the same factory equipment. Businesses try to make investments into productivity by investing in new tools or equipment that can make their people more efficient, or by buying technology that can automate processes entirely (thereby improving productivity by increasing output without needing to hire more people).

In the context of financial advisors, ‘productivity’ improvements often similarly revolve around leveraging technology or support personnel to reduce the time it takes each advisor (the ‘input’) to produce a financial plan or provide ongoing financial advice and service to clients (the ‘output’). As, in a service-based business like financial advice, time is the ultimate constraint. We’re all limited by the same number of hours in the day, week, month, and year, and how many of those hours can effectively be spent creating value for clients.

Of course, different advisory firms engage in different service models and charge different price points for the value they provide. As a result, one of the ‘purest’ ways to measure advisor productivity is simply by the amount of revenue that can be generated by that advisor. Historically, this was measured by GDC (Gross Dealer Concession), or the total amount of commission revenue that the advisor generated. For those who charge by the hour, revenue is simply the total amount of fees they generate. In the context of advisors providing ongoing services to ongoing clients (i.e., for an ongoing subscription or AUM fee), the advisor’s ‘revenue productivity’ is the total amount of client revenue they’re responsible for managing and retaining.

In other words, by measuring revenue per advisor, advisor firms can view a common-sized measuring point to understand the total value of the ‘output’ that is being generated by the advisor. And advisors who can generate more revenue (their output) with the same overall capacity (the same time constraint) are effectively generating more output (that clients will pay for) with the same input (it’s still only one advisor with the same time constraints), showing them to be more productive.

The significance of measuring advisor productivity in terms of revenue is also that it implicitly captures a lot of the intangible underlying factors where value is being added to the client relationship and/or the way the advisor is delivering it. For instance, advisors might systematize their process or better leverage technology to save time on each client and be able to serve more clients. But they could also enhance their expertise, being able to solve more complex and ‘valuable’ problems (that clients are willing to pay more to solve), generating more output (higher-valued units of advice) and thus more revenue with the same amount of time. Alternatively, advisors might also make other business refinements – from investing in support staff – to better allocate time across the firm and give their advisors more available time capacity to support more clients and revenue.

What We Learned About Advisor Productivity In The 2020 Kitces Research Study On The Financial Planning Process

To delve deeper into how financial advisors can be more efficient, in 2018, Kitces Research began a series of studies on advisor productivity – or more broadly, on what advisors actually do when they deliver financial planning, from their process to where their time actually goes.

Overall, we found that for the typical financial advisor’s day, nearly 15% of their time is spent on prospecting and business development, along with 20% of their time going to various ‘overhead’ tasks (administrative, management, and professional development), and almost 2/3rds of their time is spent on client-related activities. However, ‘only’ about 20% of their time is actually spent in client meetings! In turn, the typical advisor spends almost 36% of their time preparing for client meetings, running financial planning analyses, and handling the client servicing tasks and follow-up that comes from those meetings, plus another 9% of their time on investment-related tasks. Which means in the aggregate, advisors, on average, spend more than 2 hours ‘behind the scenes’ for every 1 hour they spend in client-facing meetings!

Some might be surprised to see that the typical client-facing time of financial advisors is this low. Although notably, it’s almost another 15% of time engaged in business development trying to find new clients, so the total ‘client-or-prospect-facing-time’ is almost 35%. With a ‘typical’ 1-hour meeting, this still amounts to an average of more than 12 meetings per week, or 2-3 per day.

It’s notable, though, that when we look at the highest-income, most-productive advisors, though, the allocation of time isn’t actually all that different!

When it comes to the most productive advisors, their client meeting time is ‘only’ about 10 percentage points higher than the least productive advisors – though this amounts to roughly 4 hours per week, which at 1 hour per meeting adds up to nearly 200 (!) additional client meetings throughout the year, allowing them to substantially lift their total client engagement (which in turn supports a higher number of clients and/or more affluent clients who pay higher fees but expect more service). Which comes by reducing the amount of time they spend on ‘middle’- and back-office tasks for those clients by leveraging staff support.

Nerd Note:

While front-office tasks are generally client-facing and revenue-generating, middle-office tasks tend to support front-office activities (and tend to be more knowledge-based than back-office tasks, which are more administrative and operational in nature). In the context of an advisory firm, the ‘middle office’ is where investment management and financial planning support activities happen (e.g., analysts who research investments, paraplanners who construct plans, etc.).

In fact, our results show broadly that advisors who have any kind of staff support – from being in an ensemble firm, a siloed advisor on a platform (e.g., with an independent broker-dealer or an affiliated-RIA platform), or simply hiring their own staff support – generate significantly more revenue and income, including (and especially amongst) the top advisors. Where those in siloed models (e.g., IBD or affiliate-RIA) earn 80% more than what standalone solo advisors do, and top advisors in ensemble firms or who build their own support teams earn more than double the top solo advisors (the leverage tends to be greater because the staff resources are even better aligned to the needs of the advisor when they hire their own staff infrastructure, or work in an ensemble firm where shared vision means better alignment of shared resources).

Notably, though, greater advisor productivity isn’t just about staff infrastructure. It’s also about expertise, as our research shows that advisors who have greater expertise – as measured by having the CFP marks – are able to get through the financial planning process more quickly. They can ask better and more knowledgeable questions of clients to get to the heart of the matter faster. They need to research less to develop recommendations because of their accumulated knowledge. And as advisors get more experienced – and tend to attract more complex clients that demand more sophisticated advice solutions – the gap grows into what we’ve dubbed the “Experience-Expertise Gap”. Such that the most experienced CFP professionals get through the financial planning process more than 40% (!) faster than non-CFP professionals at similar experience levels, producing a huge difference in productivity and client capacity!

More broadly, though, time efficiency and revenue per advisor are themselves really just proxies for the implied hourly rate of a financial advisor. As even if the advisor isn’t paid by the hour – for instance, if they operate on an AUM Model and are responsible for $300,000 of annual revenue – then over the span of a week, the advisor is likely to spend about 25 hours per week (roughly 2/3rds time) on client-related activities (meetings or the client work that happens behind the scenes), which over the span of a 50-week year (with 2 weeks for vacation!), amounts to about 1,250 ‘billable hours’ of client work. Which means the advisor is generating an implied hourly rate of about $300,000 ÷ 1,250 hours = $240/hour for the base of clients (and associated revenue) they’re serving.

And in practice, our Kitces Research data shows this actually is typical. Overall, our latest research showed that the average AUM advisor is responsible for approximately $346,000 of revenue and spends 65.5% of their 45-hour average work week on client-related activities, which over the span of a 50-week work year amounts to an effective hourly rate of $235/hour, very similar to the $250/hour average hourly fee (of advisors who operate on the hourly model). (Though notably, our research also shows that hourly advisors tend to do more work than they bill for, so the effective rate on time for AUM advisors is higher than where hourly advisors finish in practice.)

In this context, our research shows that the most productive advisors are, not surprisingly, generating a much higher hourly equivalent at more than $600/hour. Which is most commonly associated with advisors who have greater expertise and experience, working with clients who are more affluent (and thus tend to have more complex problems to solve, and more financial wherewithal to pay higher fees to have an advisor help solve those problems).

Which means, indirectly, that one of the biggest productivity lifts of financial advisors is simply being able to move ‘upmarket’, by investing in their expertise and building the experience it takes to service more complex clients with higher-stakes problems to solve… and commanding a greater premium on their time!

The Limitations Of Technology And The Efficiency Of Client Focus

One of the other interesting aspects of our Kitces Research on Advisor Productivity is what is not associated with significant increases in advisor productivity. For instance, our Research did not show that common financial planning automation tools (e.g., account aggregation tools) are actually associated with doing financial plans faster and more efficiently!

Instead, going back to our original 2018 study, we found that advisors who use account aggregation tools to automate data gathering actually spend more time going through the initial financial planning process! As while the data input process itself is faster (as account aggregation connections upfront reduce the amount of data that must be keyed in manually), the fact that advisors get better financial data upfront using the technology allows them to conduct deeper discovery meetings with clients that result in longer and more time-consuming (but more meaningful and impactful) conversations. Which can lead to more value to clients, higher planning fees, and being able to better attract and retain more affluent clients… but the improvement in productivity is not because the advisor is faster, but because their planning is better by going deeper and can command a higher fee (that more than offsets the additional time spent).

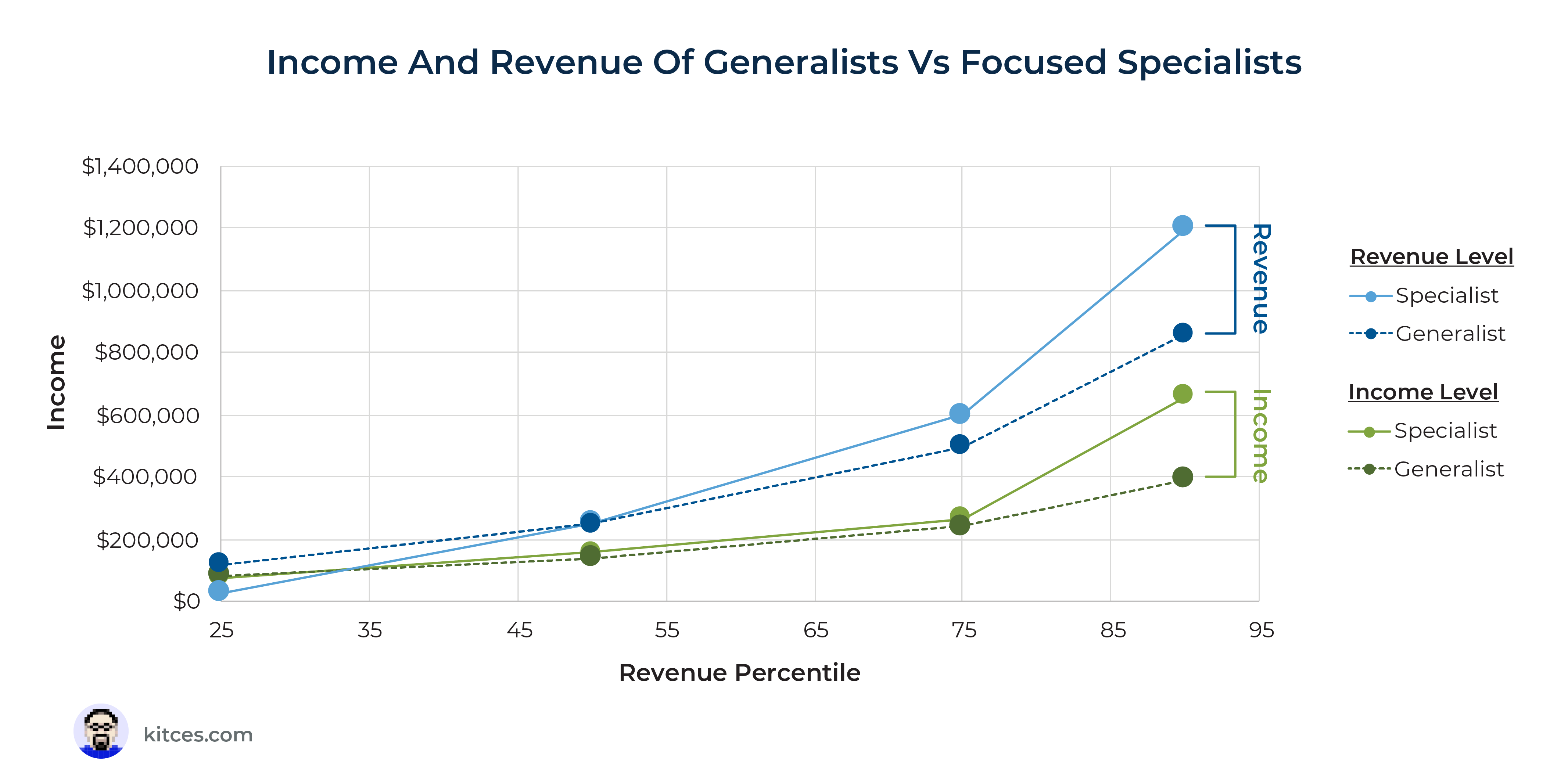

In fact, our research indicates that doing less broad and comprehensive planning – and instead going deeper and getting more focused with more sophisticated analysis in the key areas most relevant to the client – is actually a greater driver of productivity.

As a result, advisors who form a specialization or otherwise narrow down to a more focused niche clientele are able to service fewer clients and spend more time per client, and also command a higher fee for their time and hours worked with clients, given their more specialized expertise… leading to a significant increase in productivity for the top advisors who transition away from being generalists.

Overall, though, the key point is that what really drives advisor productivity isn’t about time savings to do the same (or more) client work in less time, per se – the classic view of efficiency and productivity – instead, it’s more about being able to engage in tactics that allow advisors to command a higher premium on the value of their (more expert) time, and then focus their time on those highest-revenue-generating tasks.

Which means using planning software not to get faster, but to go deeper and be better. And leveraging a team so advisors can focus more on client meetings and being involved in as much (but only as much) of the shadow work outside those meetings as is necessary to add that value. And getting CFP marks (and other advanced ‘post-CFP’ designations) so their time is more valuable. And then looking to move ‘upmarket’ to solve more complex client problems for which clients will pay a higher implied (or actual) hourly rate for those solutions.

Participate In The New 2022 Kitces Research Study On Advisor Productivity

In our new 2022 Kitces Research Study On Advisor Productivity, we’re aiming to dig even deeper to better understand the factors that distinguish the most productive financial advisors from the rest, across the core domains of how they spend their time, the financial planning process they engage in, the tools they use to support the process, and how they price their financial advice (and the clientele that they serve). In the hope that by better understanding what really influences advisor productivity, we can help advisors (and the technology and service platforms that support them!) focus on the right factors that really lead to greater business and financial success.

We hope you are excited about this new advisor research as well, and that you can support us by participating in our new Advisor Productivity survey (at least for those readers who are financial advisors!).

We’re also excited to announce that this year’s survey is being implemented using a new technology platform integrated directly into the Kitces website, which will make it possible to save your progress and come back (so you don’t have to do the whole survey in one sitting!), and, in the future, will also allow you to recall the answers you’ve provided to previous Kitces research surveys, so you don’t have to enter the same data repeatedly (to save you time when taking part in new surveys!).

In addition, all participants will receive a free copy of the final Kitces Research white paper that we produce, providing you with our latest research on what drives advisor productivity… and hopefully giving you some ideas about the changes you could make in the future to improve your own productivity!

Thank you in advance for taking the time to participate in this important financial planning research study!

{kind=link}