- Humana collects 90% of its revenues from federal and state government health programs

- Humana’s generates big profits serving the riskiest and poorest populations (Seniors and Medicaid)

- The Company raised its full-year 2022 guidance and full-year 2025 guidance indicating a 14% CAG

Health insurance and wellness provider Humana (NYSE: HUM) stock has been outperforming the benchmark indexes trading up 4.6% for the year versus (-31%) for the Nasdaq (NYSEARCA: QQQ) and (-16%) for S&P 500 (NYSEARCA: SPY). Healthcare is considered a recession proof business that continues to rise in costs at a 5.8% annual rate accounting for nearly 20% of the U.S. GDP. Humana is an integrated managed care insurer and healthcare provider like UnitedHealth Group (NYSE: UNH), Cigna (NYSE: CI), and Aetna (NYSE: CVS). It benefits from the secular trend of a growing elderly population opting to join Medicare Advantage HMO plans. For senior patients, this makes solid economic sense. Patients on traditional Medicare coverage have the responsibility of paying the remaining 20% of a medical bill after Medicare has paid its 80% portion according to their fee schedule. This can be nerve wracking and expensive especially on a fixed income. However, a Medicare Advantage plan covers literally everything leaving the patient only responsible for a co-pay amount ranging from $10 to $40. Humana collects over 90% of its revenues from Medicare and Medicaid programs. Ironically, these are the two riskiest populations for coverage under a fee-for-service model. However, Humana is proving it to be very lucrative under its value-based vertically integrated managed care model.

MarketBeat.com – MarketBeat

The Evolution of HMOs

There used to be a time when health insurance companies were just payors and doctors were the medical providers. They were two separate parties. Doctors would treat patients and bill the health insurance companies for their services. Insurance companies would find creative ways to deny claim payments (referrals, authorizations, statute of limitations for claims, etc.) in an attempt to maintain profitability. It used to be a cat and mouse game. In a nutshell, doctors would overcharge, and insurers would underpay under a fee-for-service model. You were either a provider or a payor. Managed care also known as health maintenance organizations (HMOs) disrupted the reimbursement model by introducing capitation payments. These were fixed monthly payments regardless of visits paid to the doctors based on the number of patients signed up to them as their primary care physician in the network. Doctors would receive their monthly capitation payment and collect a co-pay per visit. This helped HMOs turn wildly profitable while doctors often got a pay cut. Doctor’s offices would be swamped with appointments causing much longer wait times for patients to schedule or meet with their doctors.

Vertically Integrated Healthcare

Eventually, the insurers also became providers by building (or acquiring) their own medical care centers stocked with in-house doctors and specialists. Doctors worked on a salary and the HMOs became vertically integrated providing all the healthcare and collecting all the premiums and payments. The best example of this would be Kaiser Permanente. It’s integrated healthcare system provides a complete eco-system for its members inside each facility containing labs, radiology, primary care doctors and specialists. Humana has also evolved into a vertically integrated healthcare and wellness company as it grows its primary care clinics under the CenterWell and Conviva Care Solutions brands. One important distinction is that Kaiser Permanente doesn’t own hospitals, nor does Humana. It sold off its hospitals in 1993 to HCA Healthcare (NYSE: HCA). Apparently, hospitals don’t work well in a vertically integrated healthcare model, just clinics, urgent care facilities, and medical centers.

Earnings Continue to Grow

On Jan. 27, 2022, Humana reported its fiscal Q2 2022 earnings report for quarter ended June 2022. The Company reported an earnings-per-share (EPS) profit of $8.67 excluding non-recurring items versus consensus analyst estimates for a profit of $7.68, a $0.99 beat. Revenues grew 14.6% year-over-year (YoY) to $23.66 billion beating analyst estimates for $23.44 billion. Humana CEO Bruce Broussard commented, “We are pleased with our significant progress in growing the business, including our primary care clinics and our organic expansion of Medicaid membership, combined with the initial rollout of our value-based home care. In addition, our strong 2022 EPS growth of 20 percent, and the investments our one billion-dollar value initiative allowed us to make in our 2023 Medicare Advantage product offerings demonstrate our commitment to balancing our long-term membership and earnings growth targets.”

14% CAG Rate to 2025

On Sept. 15, 2022, Humana raised its full-year fiscal 2022 EPS to $25.00 from $24.75 versus $21.85 consensus analyst estimates. It also provided a mid-term adjusted EPS target of $37.00 for fiscal full-year 2025, representing a 14% compounded annual growth rate (CAG).

A Simpler Structure Focuses on Seniors

Starting in 2023, Humana will structure itself into two units under the Insurance Services and CenterWell. Insurance Services will house the Retail and Group, and Specialty segment handling claims processing. CenterWell will house the Healthcare Services segment. CenterWell Senior Primary Care is the nation’s largest primary care provider focused on seniors comprised of 222 clinics serving 180,000 Medicare Advantage patients. It plans to open 250 clinics by the end of 2022 and an additional 30 to 50 clinics with nearly half by acquisition annually through 2025. It expects to earn $100 to $200 million in EBITDA operating 400 to 450 centers either wholly owned or through JV by 2025. Humana expects its primary care business to contribute $1 billion in EBITDA by 2032.

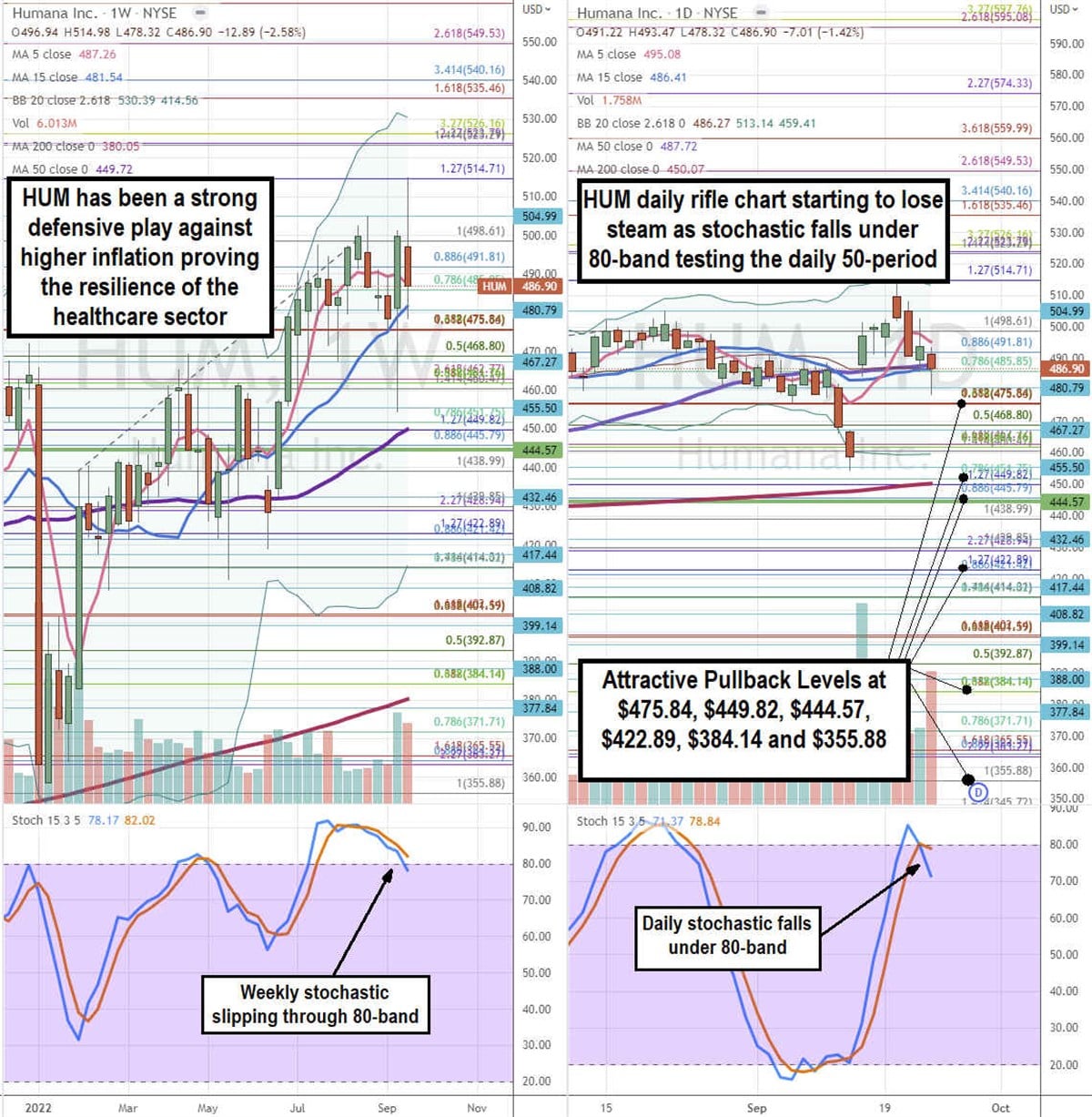

Attractive Pullback Levels

Using the rifle charts on the weekly and daily time frames enables a precision view of the price playing field for HUM. The weekly rifle chart peaked around the $514.71 Fibonacci (fib) level. The weekly rifle chart pup breakout is stalling as the 5-period moving average (MA) support starts to slope down at $487.26 tightening the channel with its 15-period MA at $481.54. The weekly 50-period MA support is rising at $449.72. The weekly stochastic is forming a mini inverse pup as it falls through the 80-band. The weekly market structure low (MSL) on the breakout through the $444.57 level. The weekly upper Bollinger Bands (BBs) sit at $530.19 and lower BBs rising near the $414.02 fib level. The daily rifle chart uptrend is losing steam with a falling 5-period MA at $495.08 and overlapping daily 15-period MA at $486.41 and daily 50-period MA at $4878.72. The daily 200-period MA sits at $450.07. The daily stochastic has fallen through the 80-band setting up a potential oscillation down and MA breakdown. The daily lower BBs sit at $459.41. Attractive pullback levels sit at the $475.84 fib, $449.82 fib/weekly 50-period MA, $444.57 weekly MSL trigger, $422.89 fib, $384.14 fib, and the $355.88 fib level.

{kind=link}