Executive Summary

Traditionally, investment planning has been at the forefront of how financial advisors add value for their clients. From advisors who earn commissions from the sales of financial products to fee-only investment advisors who charge based on client assets under management, the value advisors provide to their clients has often been centered on investment management. But, with the rise of index funds and the commoditization of investment advice, generating sufficient investment ‘alpha’ to justify a fee has become more challenging for advisors. Combined with growing advisor (and consumer) interest in comprehensive financial planning services, the number of ways advisors can add value for their clients has expanded greatly. And at a time when working as a fee-only planner, or even as a fiduciary, is not the same differentiator that it once was, being able to offer a value proposition tailored to the needs of the advisor’s ideal target client has become more crucial than ever before and could be one of the keys to success for advisors in the years ahead!

When an advisor is thinking about their value proposition for clients, they might be tempted to list as many planning value-adds as they possibly can (to reach the broadest possible base of potential clients). But this can create challenges for the advisor as well, as they will have to spend significant time managing the variability of the planning needs of their diverse client base. An alternate approach, however, is for the advisor to focus their client service proposition on the planning needs of a specific target client, which not only increases the efficiency of the planning process, but can also facilitate marketing efforts as prospects who fit the target profile will be most attracted by the depth and specificity of the advisor’s planning services!

To start crafting the persona of their ideal client, advisors can list key attributes of their target client. For advisors at established firms, this could mean thinking about their top clients, while those starting new firms could think about the type of clients they would like to serve. Client differentiators could include age, occupation, personal affinities, professional affiliations, and other criteria. The key is not necessarily to narrow down to a specific niche that meets every trait of the ‘ideal’ client, but rather to generate a sample persona that allows the advisor to start thinking about their ‘ideal’ client’s planning needs.

Once an advisor has a better idea of who their target client is, they can then consider how to tailor their value proposition to those clients. Because the advisor’s target client will probably only have certain planning needs (and may not require others), advisors can offer the value-adds from the hundreds of options available that best serve this target client. By applying the ideal-target-client framework, advisors can not only better target their marketing efforts (as they can align their website and other advertising efforts with their ideal client’s needs), but they can also streamline their day-to-day work, as they will encounter fewer ‘new’ issues as their client base grows.

Ultimately, the key point is that while there are more than 100 different ways to add value to their clients’ lives, the most successful advisors are likely to be those who are able to go deeper into the areas that are most important for their specific clients. In fact, by crafting an ideal target-client persona and shaping their service offering around the value-adds that most apply to these clients, not only can advisors enhance their efficiency, but they can also better differentiate themselves from more generalist firms, potentially leading to more efficient marketing and greater client growth in the long run!

For many years, one of the primary ways financial advisors added value to their clients’ lives was by matching them with mutual fund investments or life insurance policies that fit their needs (hopefully with their best interests in mind) in return for a commission. While the rise of the fee-only planning movement encouraged a shift from commission-based compensation (which relied on selling investment products to clients and emphasizing how well-suited those products were for the client) to one of service-based compensation (which relied on fees charged for broader financial planning services often going beyond portfolio design), investment management often remained at the center of the advisor value proposition.

However, as the field of comprehensive financial planning has continued to evolve, more advisors have begun to focus on new ways of differentiating themselves by offering a wider range of services – from cash flow planning to specialized tax planning – and have hundreds of different ways, in addition to portfolio management, that add value for their clients.

And at a time when working as a fee-only planner, or even as a fiduciary, is not the same differentiator that it once was, being able to offer a value proposition tailored to the needs of the advisor’s clients has become more crucial than ever before, and could be one of the keys to success for advisors in the years ahead!

Shifting The Advisor Value Conversation

Advisors have traditionally been trained to discuss their value proposition with prospects and clients in terms of portfolio management. One reason for this emphasis is that the results of portfolio management are easy to explain and can clearly show how the advisor adds actual value – as one of the more tangible and quantifiable aspects of financial planning, portfolio management can be used by the advisor to point out how much better the annual return on the client’s portfolio was compared to a given benchmark.

But with the rise of index funds and the commoditization of investment advice, generating sufficient investment alpha to justify a fee has become more challenging for advisors. As while an advisor may be well-qualified to construct an appropriate asset allocation for a client, differentiating themselves from all other advisors (including relatively lower-cost robo-advisors) who use a lot of the same investment management strategies has become more difficult.

The centrality of investment management is also reflected in how advisors are paid. Historically, many advisors were paid (and some still are) on a commission basis for the mutual funds or other investment products they sold. Given that the ‘fee’ a client paid through a mutual fund load or other charges was directly tied to the investments they were advised to purchase, investment management almost necessarily had to be at the center of the value conversation. Even if the advisor created a financial plan for the client (going beyond portfolio management to examine other aspects of the client’s financial life), doing so was often simply a way to promote the investment recommendations rather than to provide a standalone value-adding product.

At the same time, many fee-only advisors put portfolio management at the center of their client value proposition as well, in part because of how they charge their clients. For example, charging on an Assets Under Management (AUM) basis can put portfolio management at the forefront of a client’s perception of the advisor’s value because they are being charged based on the value and performance of their assets (rather than on whether they achieve their broader financial goals or other measures).

Some fee-only firms have adopted a fee-for-service model instead of charging on an AUM basis, which allows them to delink fees charged from portfolio performance and potentially reach a broader pool of prospective clients (who might have sufficient income to pay a fee but not enough assets to meet AUM minimums). This structure lets advisors take some of the emphasis off of portfolio management (with some firms not managing assets at all), though with this model it can be challenging to put a hard number to quantify the value the advisor offers (compared to being able to point to specific changes in portfolio value). Yet, for advisors using fee-for-service models, being able to demonstrate value beyond portfolio management is often a necessity to attract and retain clients.

Despite the traditional emphasis on portfolio management among advisors (and some consumers), the growing recognition among consumers of the value of comprehensive financial planning has given advisors the opportunity to change how they discuss their value proposition. Furthermore, because clients today have access to myriad options (from robo-advisors to DIY retail platforms) for setting up an appropriate asset allocation (often at a lower cost than using a human advisor), portfolio management is not the differentiator that it once was.

Which means that advisors now have an advantage when it comes to differentiating themselves based on the comprehensive financial planning services they provide beyond portfolio management, not just by offering services such as tax planning and retirement income planning, but also by providing the type of relationship that consumers can benefit from, that they can’t get from a robo-advisor or DIY platform (e.g., listening to understand their needs and helping them feel understood).

Luckily, advisors have a large number of ways to add value to their clients’ lives (more than 101 in fact!), most of which do not pertain to investment management. Notably, it’s not just the breadth of advisor value-adds that is important to clients, but also the depth of knowledge the advisor has on the issues that matter most to their clients. Which suggests that advisors can consider going deeper into the key planning areas that are most important to their ideal clients, not only to provide a more valuable service offering, but also to demonstrate their expertise to attract more clients in the process!

101 Ways For Advisors To Add Value

Advisors who offer comprehensive financial planning services recognize that they provide significant value to clients beyond portfolio management, but might not have an easy way to quantify how these other ways contribute to their clients’ personal and financial success. And the value that advisors add is not just in broad categories (e.g., the CFP Board’s Eight Principal Knowledge domains), but in the specific services they offer within these categories for their clients. Because while being broadly familiar with the following categories is a necessity for advisors (and is needed to pass the CFP Exam), there is wide latitude within each category for specialization to build a deeper level of expertise and provide higher-level service to clients.

And at a time when generalist advisors can have a hard time differentiating themselves for prospective clients, being able to go deeper with a specific set of value-adds that match the target client’s needs can be an effective way for advisors to grow their business, without having to be an expert in every possible way that they could add value!

Cash Flow Management

When consumers think about cash flow management, the word ‘budget’ might come to mind. But as advisors are aware, there is much more to cash flow management than analysis of regular inflows and outflows (and the less-fun activity of cutting back on spending in certain areas).

For instance, advisors can help clients plan for a major purchase, such as a home or car, from assessing its impact on their broader plan to comparing financing options.

They can also help clients make the most of the money they do spend, for example, by maximizing their credit card rewards.

And because clients will typically keep some assets in cash, crafting a cash-management strategy can be a way for clients to make more from their cash holdings and serve as a measurable way for advisors to generate their value.

For working-age clients, advisors can play a valuable role by helping them navigate the complexities of their career, from analyzing the financial impact of changing jobs, to planning for a sabbatical, analyzing benefits packages, and ensuring their financial plan could survive a temporary bout of unemployment.

Furthermore, many of these clients might be saving for children’s education (or still have student loans themselves!), which means that managing the complexities of student loan planning can not only save their clients money, but also give them greater peace of mind.

Insurance Planning

While insurance planning is not the most glamorous part of the planning process (perhaps compared to hitting a certain asset milestone or saving money on taxes), advisors recognize the importance of proper insurance coverage to preserve clients’ wealth in case disaster strikes.

As some advisors who entered the industry working for a life insurance company may know, the added value of insurance planning can go well beyond proper life coverage. For instance, by reviewing clients’ homeowners and automobile policies, advisors can ensure there is proper coverage not only to replace their home or car if they are damaged (and help them decide whether to file a claim in the first place), but also to provide sufficient liability protection to cover their assets.

Similarly, assessing umbrella insurance coverage (or suggesting that clients purchase a policy if they need one) has the potential to contribute just as much to the success of their plan as proper portfolio management if a major liability event were to occur.

Advisors can also guide clients through health insurance decisions (from choosing the most appropriate Medicare policy for retirees to assessing options during workplace open enrollment periods), as well as ensuring they have sufficient disability coverage to protect their income.

And given increasing longevity and an ever-changing market, advisors who assist clients with Long-Term Care (LTC) coverage can add value by helping them choose the most appropriate LTC policy (or none at all, if it is in the client’s best interest).

Investment Planning

While portfolio management does not always play the same central role that it has historically, it still remains a key part of the comprehensive planning process. As while an advisor’s added value may go well beyond picking stocks or mutual funds (and in fact, advisors are increasingly outsourcing investment selection), a core part of their value often lies in creating an asset allocation that meets the client’s goals (and helping the client develop goals in the first place!), risk tolerance, and other preferences.

Along with designing a client’s asset allocation, optimizing asset location is another way advisors can add value as putting different investments in taxable versus tax-deferred accounts can have a significant impact on after-tax returns.

Another area where advisor expertise can add value for clients is in the decision-making process surrounding employee stock options or an otherwise concentrated stock position.

Further, thoughtful portfolio construction (perhaps using tools like direct indexing) can provide a client with a diversified portfolio that is less subject to market risk than a specific stock or industry.

Advisors can also execute rebalancing transactions to ensure client portfolios remain in line with the desired asset allocation.

Tax Planning

In addition to managing investments, tax planning is another area where advisors can demonstrate their value in dollar terms. This often starts with reviewing the client’s tax return to ensure they received the credits and deductions for which they were eligible.

From there, the advisor can help analyze other factors, such as assessing the potential benefits of tax-loss or capital-gains harvesting or projecting the value of Roth conversions.

Charitably inclined clients can benefit from a planner’s analysis of the best time to give (e.g., whether to bunch contributions) as well as location planning for charitable giving (e.g., donor-advised funds or qualified charitable distributions).

Advisors can help clients who are business owners select the optimal workplace retirement plan to meet their needs, as well as advise on tax planning issues for the business.

Employees can also benefit from a planner’s analysis of how using a Health Savings Account (HSA) or a Flexible Savings Account (FSA) could benefit their tax situation.

Retirement Planning

As prospects often seek out the services of a financial advisor when they are approaching or entering retirement, retirement planning is often at the core of many firms’ service offerings. And given the wide range of options for creating a retirement income plan, advisors have many ways to add value for their clients in this area.

Many of these value-adds begin well before the client retires, such as whether contributions to traditional or Roth accounts would be optimal in a given year and reviewing their annual Social Security statement.

Of course, one of the major questions from clients that advisors often answer is, “When can I retire?” and providing clients with peace of mind in this area is a significant value add in itself, as it involves the complex interplay among a client’s retirement income preferences, cash flow needs, Social Security claiming strategies, available assets, Federal and state taxes, and more.

Whether an advisor prefers to use simple guidelines or more advanced withdrawal strategies, by regularly updating the plan, they can be aware of adjustments the client might need to make to remain on a sustainable path throughout their retirement.

Estate Planning

Because thinking about one’s own death is typically unpleasant, many individuals put off creating an estate plan. This creates an opportunity for advisors to add value, not only by helping clients consider what they would want their estate plan to look like, but also by nudging them to actually have the appropriate legal documents drafted.

And while many clients might already have an estate plan in place, an advisor can add value by regularly reviewing their documents to ensure that they continue to reflect the client’s wishes and that the client’s accounts are titled appropriately.

Advisors can also help ensure that their clients’ estate plans are tax efficient, managing the estate and gift tax exemptions (both Federal and state!), leveraging trusts when appropriate, and selecting the optimal assets for charitable giving.

Psychology Of Financial Planning

When prospective clients approach a financial advisor, many might be looking for help with the technical aspects of their financial lives, from investment management to retirement income planning. But advisors can also add significant value by working with clients to explore their goals and preferences, as well as serving as a steadying voice during turbulent market conditions.

For instance, while some clients might be focused on attaining a certain level of assets or generating a particular amount of income, they might not stop to think about what they actually want to do with the money. Whether it is informal goal-setting or using a more structured method (e.g., George Kinder’s Life Planning approach), advisors can help clients not only build up their assets, but also help them live their best lives with the resources they have.

And sometimes, clients recognize that psychological factors are standing in their way of making better financial decisions. Whether it is helping clients identify and address ‘money scripts’ from their past that shape their views of money to overcoming biases toward financial decision making, or even helping spur conversations between spouses or families to worth through challenging financial discussions, advisors have a range of ways to add value to clients in this area.

Notably, the above list is not comprehensive, as there are countless ways in which advisors add value for their clients. At the same time, though, a given advisor is not likely to have expertise in every area listed (though they can pursue supplemental certifications for areas that are important to their clients), but being able to dig deeper into specific areas can attract an ‘ideal target client’ whose needs match those services.

Crafting A Tailored Menu Of Value Adds For An Ideal Target Client

When an advisor is thinking about their value proposition for clients, they might be tempted to list as many planning value-adds as they possibly can. Because advisors might find it appealing to market to the widest possible base of prospective clients, offering a huge menu with something for everyone (e.g., ‘The Cheesecake Factory’ approach) can be tempting. But this can create challenges for the advisor as well.

Not only will the advisor actually have to gain expertise in a wide range of planning topics, but they will also likely have to spend significant time managing the variability of the needs of their diverse client base. And because of the diverse array of needs, advisors may find themselves challenged to create operational efficiencies to service all of their clients since they all need different services.

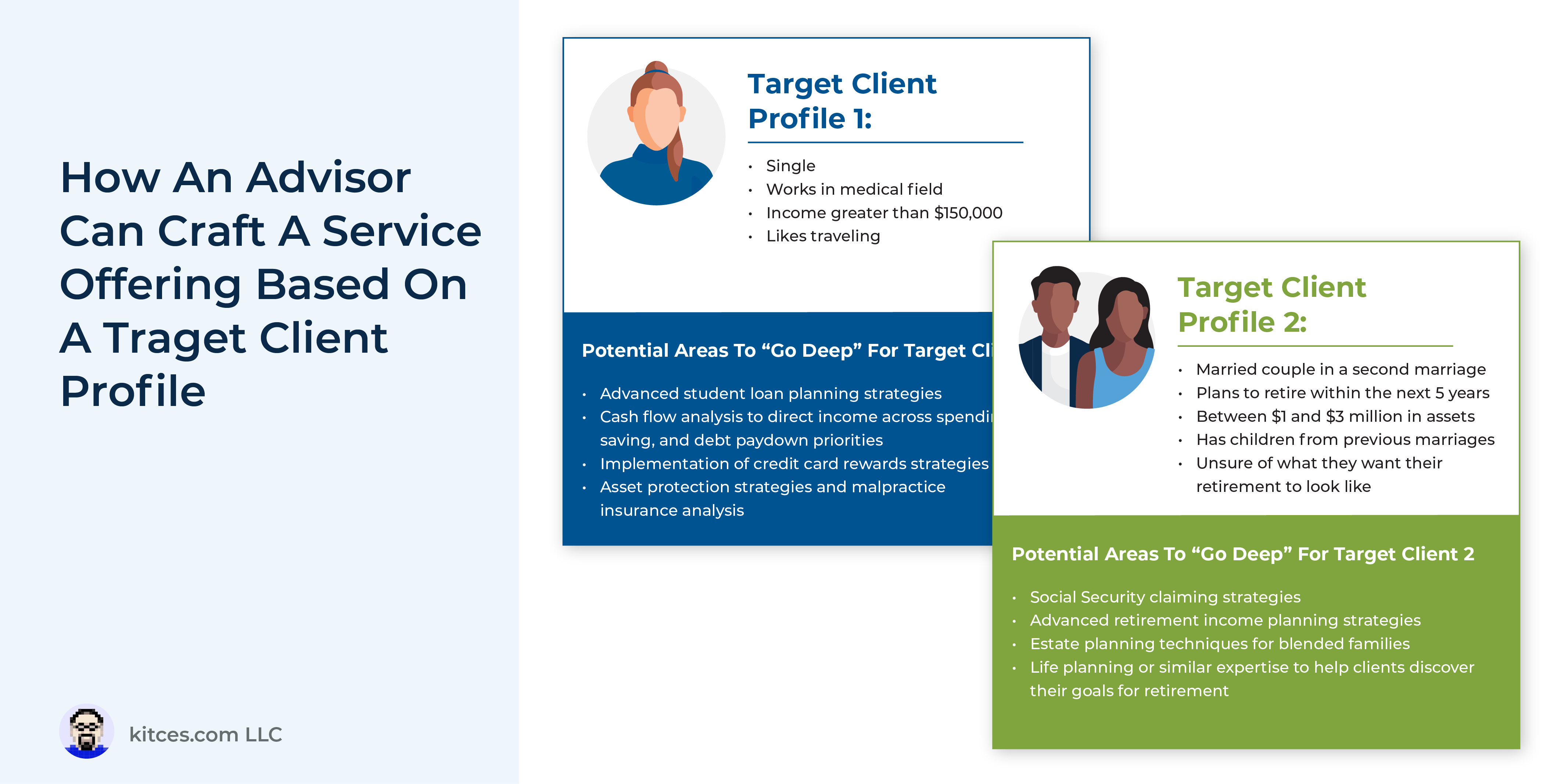

An alternate approach, however, is for the advisor to focus their client service proposition on the planning needs of a specific target client, so the advisor can go deeper on the particular areas required to service their unique clients (whether their ideal clients make up a broad group like pre-retirees or a more specific niche such as clients who work in a given profession) in a way that goes beyond the service of a more generalist advisory firm. Which can not only increase the efficiency of the planning process, but also facilitate marketing efforts, as prospects who fit the target profile will be attracted by the depth and specificity of the advisor’s planning services!

Creating An Ideal Target Client

The first step to creating a more tailored service offering is for an advisor to understand who their ideal target client is. By having a clear idea of the clients that they want to serve, advisors can focus on the value adds that will attract these clients and that will meet their planning needs.

To start crafting the persona of their ideal client, advisors can write a list of the attributes their target client would have. For advisors at established firms, this could mean thinking about their ‘top’ clients (perhaps based on profitability, similarity to other clients, or by those who have needs that match the advisor’s expertise), while those starting new firms could think about the type of clients they would like to serve.

Client differentiators can include age, occupation, location, affinity affiliations, planning needs, and other criteria. The key is not necessarily to narrow down to a specific niche that meets every trait of the ‘ideal’ client (e.g., divorced veterans in their 50s), but rather to generate a sample persona that allows the advisor to start thinking about this ‘ideal’ client’s planning needs.

Advisors can complete Mary Beth Storjohann’s “Ideal Client Avatar” exercise to help them identify the types of clients they want to serve.

Crafting An Advisor Service Offering Based On The Ideal Target Client

Once an advisor has a better idea of their target client, they can then consider how to tailor their value proposition for clients. Because the advisor’s target client will probably only have certain planning needs (and may not require others), advisors can select the value-adds from the hundreds of options available that best serve this target client.

Example 1: Ted has extensive experience creating retirement income plans for clients who retire before ‘traditional’ retirement age and is an avid traveler, so his ideal clients are individuals in their 50s who love to travel and are considering early retirement.

Based on this ideal target client, Ted could focus on adding value to clients through retirement income planning and projections, maximizing Roth conversions and capital-gains harvesting, helping clients take advantage of credit card rewards (to help fund their travel), expertise in health insurance options for individuals who retire before reaching Medicare age, and, given that their retirement could last 40 years, support clients in discovering what they actually want their retirement to look like.

By focusing his marketing on these areas of added value, Ted can attract his target clients, who will see how Ted can potentially address their needs better than an advisor serving more general clientele. And as more of his clients fit this ideal persona, Ted can spend more of his time going deeper on these core value adds and less on other areas that are not as applicable to these clients.

While it might seem like creating an ideal target client and focusing marketing on their needs might be limiting the pool of potential prospects, it can also open the door to clients who might not fit into a more traditional asset-based fee model.

Example 2: Rebecca is a financial advisor and her wife is a doctor, so she is familiar with many of the issues new doctors face, from paying off a large student loan balance to avoiding the temptation of dramatically expanding their lifestyle in line with their higher incomes.

Rebecca decides that her ideal target client will be doctors with student loan balances.

Based on this ideal target client, Rebecca could go deep into areas such as student loan repayment strategies, proper disability coverage for physicians, and cash flow management techniques. Given that newer physicians likely have high incomes but limited assets, Rebecca decides to offer an income-based, rather than an asset-based, fee model so that she will be able to serve members of her identified target demographic profitably.

By applying the ideal-target-client framework, advisors can not only better target their marketing efforts (as they can align their website and other advertising efforts with their ideal client’s needs), but they can also streamline their day-to-day work, as they will encounter fewer ‘new’ issues as their client base grows.

Notably, while having a single ideal target client can promote efficiency, advisors can work with more than one ideal client persona. The key, though, is to create separate lists of value adds for each target client so that each list is maximally relevant to them!

Example 3: Based on his background and expertise, Roy has identified 2 ideal target clients he wants to serve: retirees who are either recently divorced or are philanthropically minded.

While the specific needs of these two groups are different, focusing on these ideal client profiles allows him to better tailor his marketing and provide a deep level of service for their particular planning needs (e.g., cash flow and estate planning needs for clients going through a divorce and advanced giving strategies for his charitably inclined clients).

Altogether, identifying ideal target clients and focusing on the value adds that are most important to them can lead to a better experience for both the client (who can more easily identify an advisor who has expertise in the issues they are facing) and the advisor (who will have more expertise with their clients’ issues and be able to target their marketing efforts accordingly).

And even if an advisor’s ideal target is broad (e.g., pre-retirees and retirees with significant assets), they can still develop their profile around a narrower set of value adds that are most important to their clients from the larger list of possibilities!

Ultimately, the key point is that while there are more than a hundred different ways advisors can add value to their clients’ lives, advisors who are able to go deeper for their ideal target client have hundreds more ways to do so.

In fact, by crafting an ideal target client persona and shaping their service offering around the value adds that most apply to these clients, advisors can not only enhance their efficiency, but also better differentiate themselves from more generalist firms, potentially leading to more efficient marketing and greater client growth in the long run!

{kind=link}