In the early days of investing, stocks were often evaluated in a vacuum: Investors assessed the plusses and minuses of each company’s stock based on its own merits, with little consideration of the relationship between one stock’s performance and that of the market as a whole. Then, in the 1960s, with the advent of the Capital Asset Pricing Model (CAPM), investors began to look at stocks (and by extension, pooled investments like mutual funds as well as entire portfolios) through the lens of a stock’s risk compared to the entire market (and concurrently, the expected return that investors demanded to compensate for that risk). A stock’s ‘beta’ – generally speaking, its riskiness compared to the overall market – was considered a key driver of its future performance.

In the early 1990s, however, the release of a landmark study by Eugene Fama and Kenneth French introduced the concept of “factors” beyond beta that could influence a stock’s performance. Though Fama and French’s study focused on 2 factors (size and value), investment research in the subsequent 30 years has identified hundreds of additional factors that investors can use to adjust their return opportunities and expectations in constructing diversified portfolios.

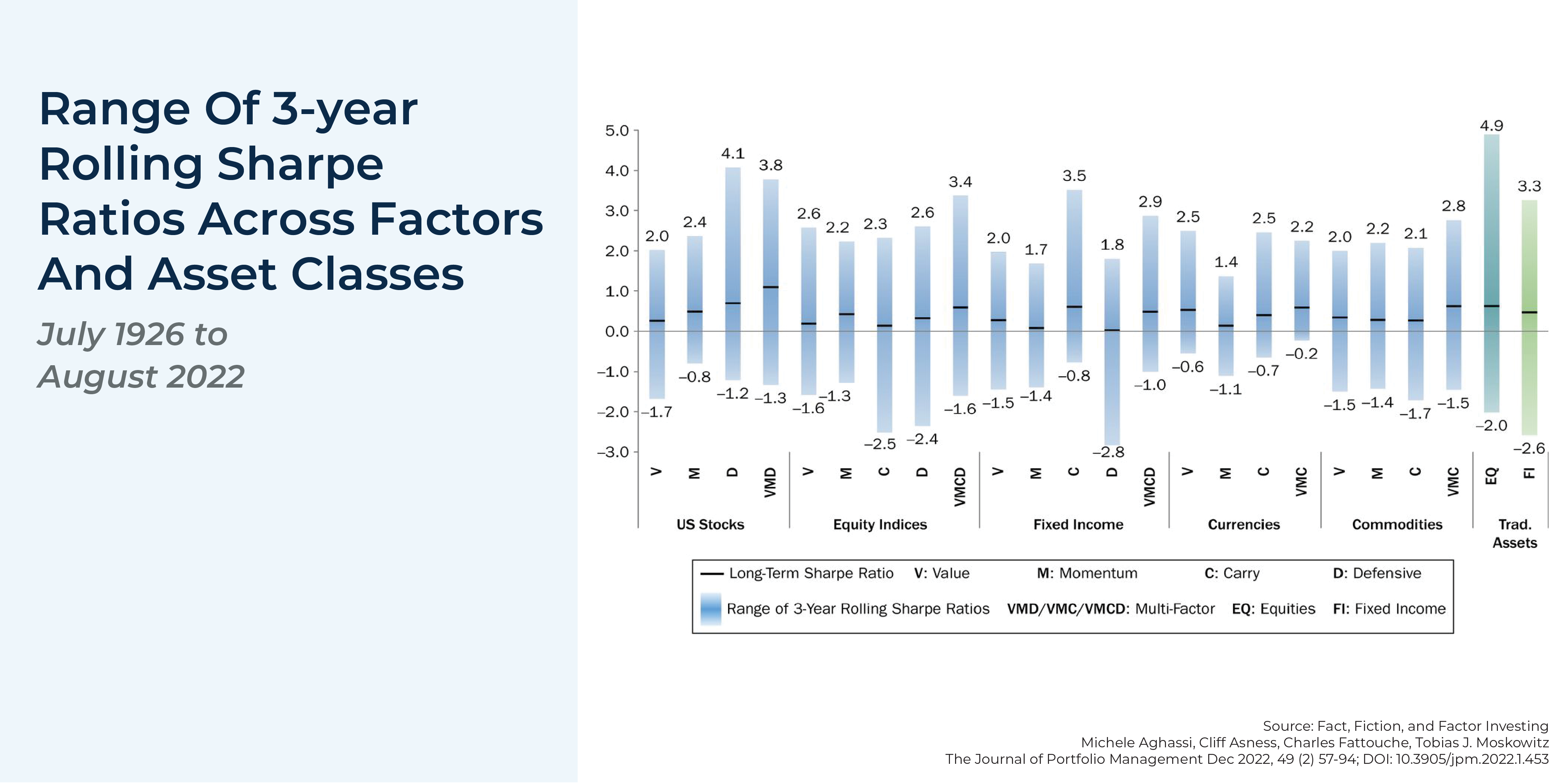

Although the rise of factor-based investing has created many possibilities for advisors to add value by optimizing the risk and return profiles of their clients’ portfolios, the explosion in the number of potential factors creates its own new challenge for investors, from determining how to evaluate the factors themselves to deciding which ones are really useful in making investment decisions. As it turns out, when filtering the “zoo of factors” down to only those that have had explanatory power to predict above-market returns (as well as that meet a series of tests for persistence, pervasiveness, robustness, investability, and the logic of how they operate), there are really only a handful of factors that are truly worthy of investment (including size, value, momentum, quality, profitability, and quality for equity; as well as term and credit quality for fixed income), which make it much more manageable for investors to implement a factor-investing strategy.

Furthermore, focusing on just the most salient factors can allow investors to avoid some of the criticisms of factor investing raised over the years, including that factors are overly risky compared to the market, that factor investing is prone to failing at inopportune times, and that factors have become irrelevant (or perhaps too well-known and ‘overcrowded’ to produce excess return) for investors going forward. In reality, the body of evidence that supports factor-based investing has only grown larger with time – as long as one focuses on just the factors that have actually proven to be effective.

The key point is that while investment risk is impossible to eliminate, factor-based investment strategies have been shown by a wide body of data to create excess returns without adding to a portfolio’s overall risk. While factor investing isn’t a panacea and can itself be prone to long periods of underperformance, the evidence has shown that it can reward investors who are willing to stick with it. Ultimately, factor investing can be almost as much about behavioral factors as economic ones: The fact that so many investors aren’t willing to endure the risk of underperformance creates potential rewards for the ones who are!

{kind=link}