As Chris Giles

explains here,

Chancellor Hunt is gaming his fiscal rules. He is not the first

Conservative Chancellor to do so. In particular, it is now routine

for Conservative Chancellors to announce that they are freezing fuel

duty, but they then tell the OBR that they will raise them with inflation in

every forthcoming Budget. They have repeated this fiction for the

last dozen years. The fiction that the duty will be raised in the

future, just not now, flatters future revenue projections and makes

it easier for the Chancellor to meet his fiscal rules.

This particular

problem arises because the OBR is legally obliged to produce a

forecast on the basis of what the government claims is its policy.

However there is the letter of the law, and there is politics.

Suppose the head of the OBR decided next year that it would ignore

the government and instead use past data to assume that fuel duty

would not be uprated in future, what exactly would the Chancellor do?

Fire him? It just wouldn’t happen.

I know the previous

head of the OBR thought about doing this. The current head, Richard

Hughes, would have his hand strengthened considerably if the Treasury

Select Committee stated that in future it expects the OBR to do this.

This committee has to approve senior appointments to the OBR. Whether

the Committee has the political courage to do this is another matter.

In the longer run the legislation governing the OBR should be changed

so as to allow it to base its projections on what it believes the

government will do in the future. [1]

Much the most

difficult and serious element of gaming, that I mentioned

myself after the budget, involves the projections for

public spending. As was clear from the last Autumn Statement, the

Chancellor’s plans involve two things that almost certainly will

not happen. The first is that we have a renewed round of public

spending cuts, in a public sector that is already cut to the bone.

The second is that the relative pay of public sector workers

continues to be reduced relative to other workers, in a situation

where public sector vacancies are at critical levels and public

sector workers are either striking or have won awards that exceed the

government’s assumptions. This bit of gaming is more difficult to

fix, yet it risks making a mockery of the whole Budget forecast.

Some might say that

fiscal rules are a fiction anyway, so who cares about this. I don’t

like the particular fiscal rules the Chancellor has chosen [2], but I

do think fiscal rules are there for a good reason. I partially disagree

with Stephen Bush on why they are important. They are

not there to keep the markets happy, and nor are they required to

keep departmental spending in place. The purpose of fiscal rules is

to stop the Chancellor fooling voters, by for example cutting taxes

just before an election and pretending that these cuts are

sustainable. Voters deserve to know whether pre-election tax cuts or

other bits of fiscal largesse are bribes that will disappear once the

government is elected or something that is more permanent. That is

why gaming the fiscal rules matters.

If we go into why

the rules are currently being gamed, it helps to understand why it’s difficult to stop. Paragraph 4.46 of the OBR report explains

why assumed pay growth for the public sector is about 1% lower than

that for the private sector, thereby continuing the relative fall in

the pay of public sector workers that we have seen since 2010/11.

There are two points to make. The first involves implausibility,

given the increase in vacancies, quit rates and strikes we are currently

seeing in the public sector. But just because something is

implausible doesn’t mean it is impossible. The second is visibility

– you have to dig deep in the OBR’s report to find this analysis.

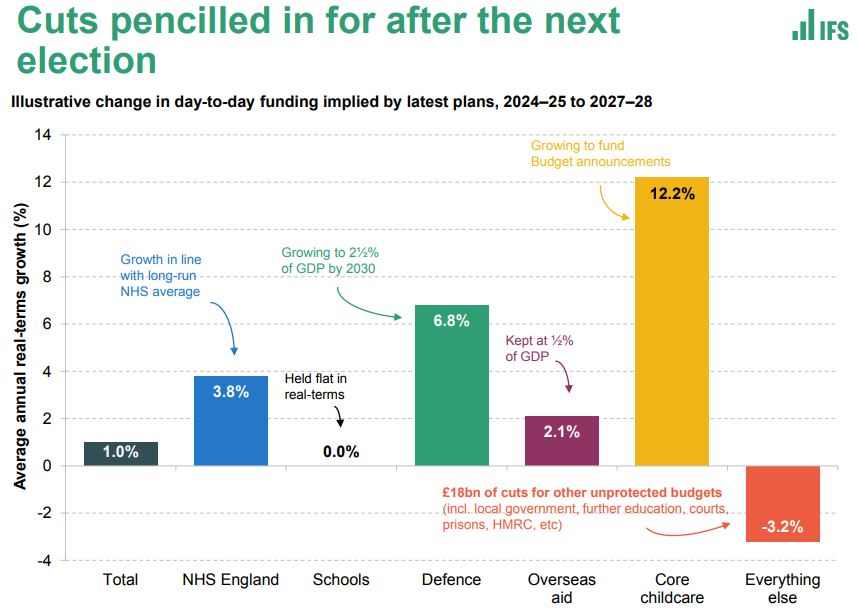

On public

spending, the numbers the government have pencilled in are broad aggregates, so you have

to make some assumptions to see what this means for individual

departments. Luckily the IFS post-budget

analysis has a go in the chart below.

NHS spending increases are at

the past long term average, which is the minimum conceivable in that

it does nothing to relieve current pressures. Spending on schools

declines as a share of GDP, while it is announced policy that defence

spending does the opposite. That leaves an annual real term fall in

spending of 3.2% in everything else. We have the same two problems.

The government’s assumptions are opaque, so they can always say

they don’t ‘recognise these numbers’, and they are highly

implausible but it is hard to say they are totally impossible.

So the OBR under its

current remit cannot say that these projections cannot happen, but

because the detail is hidden (pay) or not spelled out (departmental

totals) the Chancellor bears little cost in putting these implausible

numbers forward.

One way around this

problem is to make fiscal rules apply to the short term rather than

medium term, but there are excellent

reasons why this cure would be worse than the disease.

A much better option is to strengthen the watchdog role of the OBR,

to make it more in line with some

other fiscal councils. This would require two changes

to the legislation that set up the OBR.

First, the OBR needs

to be able to do policy variants: simulations/forecasts where policy

variables are different from the government’s announced plans. That

goes well beyond the minor tweak suggested for fuel duty, because no

evidence would be required that this would be what the government

might actually do. The Treasury were insistent that the OBR would not

be able to do this when it was set up, partly I suspect because it

didn’t want to see alternatives to austerity.

Second, the OBR

would be mandated to comment on the feasibility of aggregate public

spending plans, and if the government’s projected plans were

unlikely to be feasible, to prepare an alternative forecast based on

plans that were feasible. Very quickly this alternative, more

plausible forecast would be the one that everyone quotes.

Of course neither of

these things will happen under the current government, so what is to

be done next year if, as some

have suggested, the government not only cuts taxes but

pencils in even more tax cuts, and combines these with even more

unlikely paths for public spending than are already there. The IFS

and Resolution Foundation will no doubt call the government out on

this, and the text in the OBR forecast will provide plenty of hints,

but both are likely to pass most voters by.

Ironically the

government will see these tax cuts as a ‘trap for Labour’. If

Labour say they will not implement these tax cuts if they win the

election then they give a real ‘higher taxes under Labour’ weapon

to the Conservatives. If they say they will cut taxes then

journalists, with some justice, will ask Labour about the clear

implications for public spending. A compromise for Labour would be to

accept the immediate cuts, but not future cuts, saying the

Conservatives couldn’t afford these either. There are no easy

answers here, but these dilemmas stem from the government’s ability

to game the system. The government’s ability to game the system in

turn stems from the weakness of the OBR as a watchdog.

[1] Another example

of possible gaming that Giles and others have mentioned is investment

allowances for firms. In the OBR projections this is a three year

policy, but Hunt announced that he would like to make it permanent if

and when resources allow. There is the expectation that the

Chancellor probably will make it permanent at some point, but this is

based on politics rather than experience. In this case the OBR would

have little past evidence on which to warrant overruling what the

Chancellor says his current plans are. For that reason I don’t

think this is an example of gaming the rules. Chancellors should be able to announce

aspirations, but if the fiscal rules don’t allow those aspirations

to happen I can see no reason why the OBR should do otherwise than

take the Chancellor at his word. I think this is an example of the rules working.

[2] I have always

argued that falling debt to GDP is a silly rule, and I’m glad the

consensus seems

to be shifting that way even if Labour policy is not.

In addition, targeting the total deficit rather than the current

deficit that excludes private investment is wrong both in principle

and in practice.

.

{kind=link}