Toby Nangle was formerly Global Head of Asset Allocation at Columbia Threadneedle Investments. Tony Yates is a former professor of economics and head of monetary policy strategy at the Bank of England.

The Bank of England’s rising interest bill has been of increasing focus over the past few weeks. The BOE balance sheet has swollen to close to £900bn after waves of quantitative easing. And while there were fiscal dividends attached to effectively shortening the rate structure — circa £123bn to the end of April — there could be fiscal costs as rates rise. So, what to do?

First, a quick recap of the mechanics.

Almost 15 years in there’s still no agreement as to how QE works as a policy, but operationally it’s straightforward. The BOE bought around £875bn of interest-bearing gilts as well as a few corporate bonds. It paid for these gilts with fresh central bank reserves. As such, the asset side of the Bank’s balance sheet ballooned (gilts!) as did liabilities (reserves!).

Prior to QE, the BOE set overnight interest rates by fine-tuning the quantity of (unremunerated) reserves in the market. Commercial banks would then scramble to borrow or lend them to one another at a price, and that (market) price was Bank Rate.

QE meant vast quantities of reserves were created, so fine-tuning reserve quantities to target price could no longer work. The Bank had lost its ability to put a floor on rates and recognised: a) financial institutions would face problems of such magnitude that negative rates could be contractionary rather than stimulative; and b) there could be some unpredictable adverse consequences of plunging into the world of unmanaged negative interest rates. Paying interest on reserves was a way to keep control of rates, while doing huge amounts of QE.

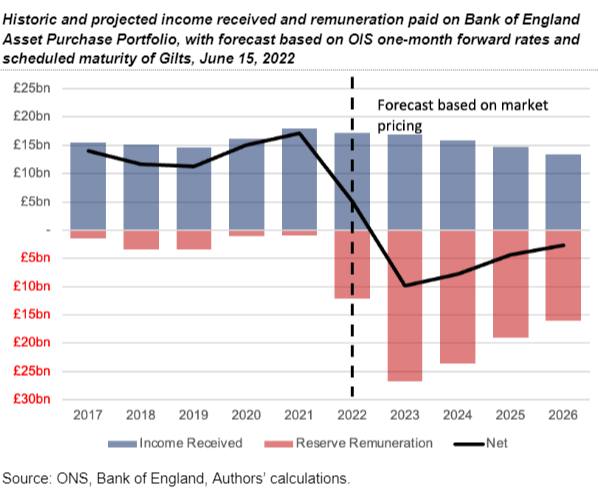

And so QE led to the Bank receiving coupons on the gilts that they had bought and paying interest on reserves. The positive carry was, and continues to be, enormous:

But now, with interest rates rising, the interest costs attached to the liability side of the QE book (interest on reserves) threatens to exceed the income from the asset side of the QE book (the gilts).

Will this bankrupt the BOE? Absolutely not! Leaving aside that it’s hard for a central bank — which can literally imagine into existence as much new money as it likes — to run out of its own claims, the Bank was careful at the inception of QE to ensure that the whole programme was indemnified by HM Treasury. In return the Treasury has received all of that enormous positive carry.

But so far as described, it does sound like taxpayers are on the hook for the P&L of one of the largest long-duration trades in history. At a time when yields are moving higher. And the net cash flow does turn negative once Bank Rate moves north of 2 per cent.

Two UK think tanks, The National Institute of Economic and Social Research and The New Economics Foundation, have published plans to keep that positive carry.

The NIESR plan draws on the insights of Bill Allen, an ex-BoE Head of Division for Market Operations and economic historian who wrote the definitive UK monetary history of the 1950s. At the start of the decade Britain had debt to GDP of 175 per cent and by 1959 this had declined to 112 per cent in spite of modest growth and low inflation. How? Allen argues that outright financial repression — monetary authorities’ direct control of banks and credit — was the answer, and that the lessons from November 1951 can be borrowed to financially repress banks today.

Specifically, NIESR argued last summer that banks should be allocated compulsorily newly created two-year gilts to the commercial banks at non-market prices in exchange for their reserves “as a means of draining liquid assets from the banking system, and of insulating the public finances in some degree from the costs incurred when short-term interest rates were increased, as they were in March 1952”. Failing to follow this plan has, according to NIESR, cost HM Treasury £11bn.

The NEF plan by contrast follows Lord Turner’s suggestion to pay zero interest on a large block of commercial banks’ reserve balances, but continue to pay interest on remaining marginal balances. This approach has international precedent: it’s how things are done in the Eurozone and Japan. NEF reckons that HM Treasury would save £57bn over the next three years if their plan is taken up.

Free money! Where’s the catch?

Well, the NIESR plan is . . . perplexing. The authors admit that its implementation would lead to soaring yields and could disrupt the government bond market in sufficiently unpredictable ways. They recommend that “a modest first step could test the size of such an impact”.

In a world where a central bank forex dealer calling around for live price checks constitutes an intervention, this “modest first step” could end . . . badly?

And any scheme that forces an unplanned and fundamental reconfiguration of every commercial bank’s balance sheet would pose a variety of financial stability questions. It’s probably not a stretch to argue that implementing the plan may even have triggered a financial crisis. Still, the plan would’ve led banks’ income to be £11bn lower and the government’s income to be £11bn higher.

For any policymakers reading this thinking “yeah, but ELEVEN BILLION!?”, a lower risk way to scratch that itch could be to introduce an £11bn windfall tax and maybe not accidentally trigger a financial crisis.

The NEF plan by contrast looks more reasonable. It’s rooted in practices that other major central banks have operated (albeit only during periods of negative interest rates).

But as Bill Allen (of the NIESR plan) writes, it could have adverse consequences for the financial system and would shift QE from an instrument of monetary policy to an instrument of taxation. Moreover, taxation would be ongoing and open-ended, with commercial banks more heavily taxed than less regulated financial channels. Increasing the stock of QE would push taxes on commercial banks higher; unwinding QE would cut taxes on commercial banks. This turns the traditional logic of balance sheet operations (where QE is more normally associated with easing) upside down.

Some argue we should tax the banks more. Others argue that doing so would just push costs across society, heighten financial instability risks and stymie growth. If the Chancellor wanted to tax the banks more, why not … er … tax the banks? Binding this decision forevermore with the decision as to how desired monetary policy stance should be implemented is illogical.

That said, we do see a powerful case to accelerate the Bank’s glacial timetable for unwinding QE, or to auction new sterilisation bonds into the system — and return to the reserve averaging system of yesteryear. Coincidentally, these reserves genuinely would require no remuneration.

{kind=link}