Executive Summary

Bear markets can be stressful for both financial advisors and their clients – particularly for those clients who are near retirement or have recently retired and are therefore especially susceptible to sequence-of-return risk, as a market downturn in the first decade of retirement can negatively impact a retiree’s sustainable spending rates. At the same time, though, market downturns can create favorable tax planning opportunities, including the ability to maximize ‘discounted’ Roth conversions.

While individuals at any income level can complete Roth conversions (unlike making Roth IRA contributions, which have income limits), it does not necessarily mean that doing so will always be the most tax-efficient decision. Because whether traditional or Roth accounts are better depends on that individual’s tax rate today as compared to their expected future tax rate. Typically, this means that it will be advantageous to make traditional contributions (and reduce taxable income) when a person’s marginal tax rate is higher today than it will be when the funds are withdrawn in the future, and Roth contributions (or conversions) when the future tax rate is expected to be higher than it is today.

For investors who do consider making a Roth conversion, a declining market can effectively put the conversion ‘on sale’ at a (hopefully) temporarily depressed value. This is because, as the total value of the account drops, the dollar amount to be converted to a Roth account will represent a larger percentage of the pre-tax account, resulting in a larger portion of the future growth of the account being shifted into a Roth without moving into a higher tax bracket as a more sizable portion of the account is converted.

Notably, the benefits of Roth conversions during a market downturn can also depend in large part on how an individual sources the funds to pay the taxes on the conversion. And when it comes to paying the taxes due, cash is usually king, since using available cash set aside in a savings account – instead of taking funds that could have otherwise been converted to pay those taxes – will allow a larger balance of the tax-free Roth account to enjoy a market rebound. As while the individual might not have wanted to invest the money in the savings account, by using it to pay the taxes due on the Roth conversion, the savings is effectively paying for the future tax-free growth in the Roth account!

In addition, because Roth conversions can be made throughout the year in any amount, certain strategies can help maximize the value of the conversions, minimize potential client regret, and avoid running afoul of the tax rules that govern conversions. For example, conversion-cost averaging (dividing a selected annual conversion amount into regular, smaller conversions throughout the year) and Roth barbelling (converting once at the beginning of the year and again at the end of the year when the client’s tax picture is clearer) can allow for adjustments of the amount converted if a client’s income changes unexpectedly, among other benefits.

Ultimately, the key point is that a market downturn presents an opportunity to convert a higher percentage of a pre-tax account to a Roth account for the same amount of taxable income, for those who otherwise should be doing a Roth conversion given their current tax rate. Because while a down market can be challenging for both advisors and their clients, the opportunity for Roth conversions ‘on sale’ during these periods (when appropriate!) offers advisors the chance to generate tax alpha for their clients!

Authors:

Bear markets can be stressful for financial advisors and their clients alike. Because while recognizing that markets cannot rise forever is easy in theory, going through a market downturn can be a painful experience, particularly for those who are near retirement or have recently retired (and are therefore particularly susceptible to sequence-of-return risk, as a market downturn in the first decade of retirement can negatively impact a retiree’s sustainable spending rates).

At the same time, a market downturn can create tax planning opportunities for advisors and their clients. For example, a weak market can create opportunities for tax-loss harvesting, as a client is more likely to have investments that have declined in value below their cost basis and can ‘harvest’ the losses to offset any capital gains (or up to $3,000 of ordinary income in a given year).

In addition, though, a bear market can be a particularly opportune time to complete Roth conversions.

The Rules Of Roth Conversions

Roth IRAs have been incredibly popular retirement vehicles since their first introduction under the Taxpayer Relief Act of 1997. In exchange for making contributions in after-tax dollars to a Roth account, growth within the account is tax-deferred, and those gains can ultimately be withdrawn tax-free as ‘qualified distributions’ if certain basic requirements are met.

Because the opportunity for tax-free distributions is so favorable in the long run, individuals are restricted to the annual maximum contribution limit to a Roth IRA (which, in 2022, is $6,000 per year plus a $1,000 annual ‘catch-up’ contribution for those age 50 and older), although some workers have access to Roth 401(k) plans or similar workplace Roth accounts that follow the higher contribution limits for employer retirement plans (in 2022, an annual limit of $20,500 plus catch-up contributions of $6,500 per year).

Beyond making annual contributions to Roth accounts, individuals can build up their Roth balances by moving money from a pre-tax retirement account (e.g., a traditional IRA or 401(k) plan) to a Roth account. Which does not have to be done on an all-or-none basis; rather, IRA owners can choose to convert only a portion of the account (in any amount/percentage they wish). For example, if an individual has a traditional IRA worth $500,000, they could choose to convert the full $500,000 balance, or ‘just’ $400,000, or only $50,000 or $100,000, or any other amount between all of the account and none at all.

However, the IRS imposes a cost on whatever amount is “Roth converted” by treating the withdrawn amount as a taxable event – which means reporting the amount of the conversion as ordinary income for tax purposes. Even though the income is reported and the consequent tax bill is paid, the converted amount is not actually withdrawn, but rolled into a Roth IRA and becomes eligible for the various benefits of Roth accounts. These include the aforementioned tax-deferred growth and tax-free qualified withdrawals, and no Required Minimum Distributions (RMDs) upon reaching age 72.

In addition, similar to the standard rules for Roth conversions, the after-tax “principal” that was contributed (or in the case of a Roth conversion, converted) can also be withdrawn tax-free (though in the case of Roth conversions, there is a 5-year waiting period after completing the conversion to access the conversion principal tax-free).

Notably, while Roth conversions had income limits for more than a decade after their initial creation –households with an Adjusted Gross Income of more than $100,000 were not permitted to engage in any Roth conversions – since 2010, there have been no income limits on those who can complete Roth conversions. Which means that those with higher incomes not only face the decision of whether ‘to Roth or not to Roth’ with their conversions (like anyone else), but also have a means to circumvent the income limit on Roth contributions (through the so-called ‘Backdoor’ Roth contribution strategy).

However, it is important to note (and will be discussed in depth later) that while individuals can make Roth conversions regardless of income, it does not necessarily mean doing so is always the most tax-efficient decision. As while the optionality of Roth conversions can be useful for tax planning purposes, the amount converted often needs to be controlled in order to avoid generating income that would put the individual in a (potentially much) higher tax bracket.

Why Roth Conversions Aren’t Always The Best Choice

With the promise of tax-free growth on qualified withdrawals, Roth conversions might seem like a ‘no-brainer’. But the reality is that while having tax-free growth in a Roth account is clearly better than keeping dollars invested in a regular investment account (that is taxed annually on interest, dividends, and capital gains), the fact that investors have a choice between a Roth-style retirement account and a ‘traditional’ retirement account means the decision is more nuanced.

As contributing to a Roth account does have a ‘cost’ in the form of paying taxes today on the contributed (or converted) amount that would have been tax-deductible today (or remained tax-deferred) and only taxable in the future with a traditional retirement account. Which means that whether traditional or Roth accounts are better depends on that individual’s tax rate today, when the Roth contribution/conversion is made, as compared to their expected future tax rate, when the funds would have otherwise come out of the traditional account.

In fact, it turns out that if an individual’s tax rate is the same in the year they are making the conversion and in the year they withdraw from the account, there is ultimately no difference in having the money in a pre-tax versus a Roth account. This ‘tax equivalency principle’ exists because, in the long run, the additional value of tax-free growth in a Roth is the same as the additional value of the upfront tax deduction for the traditional retirement account.

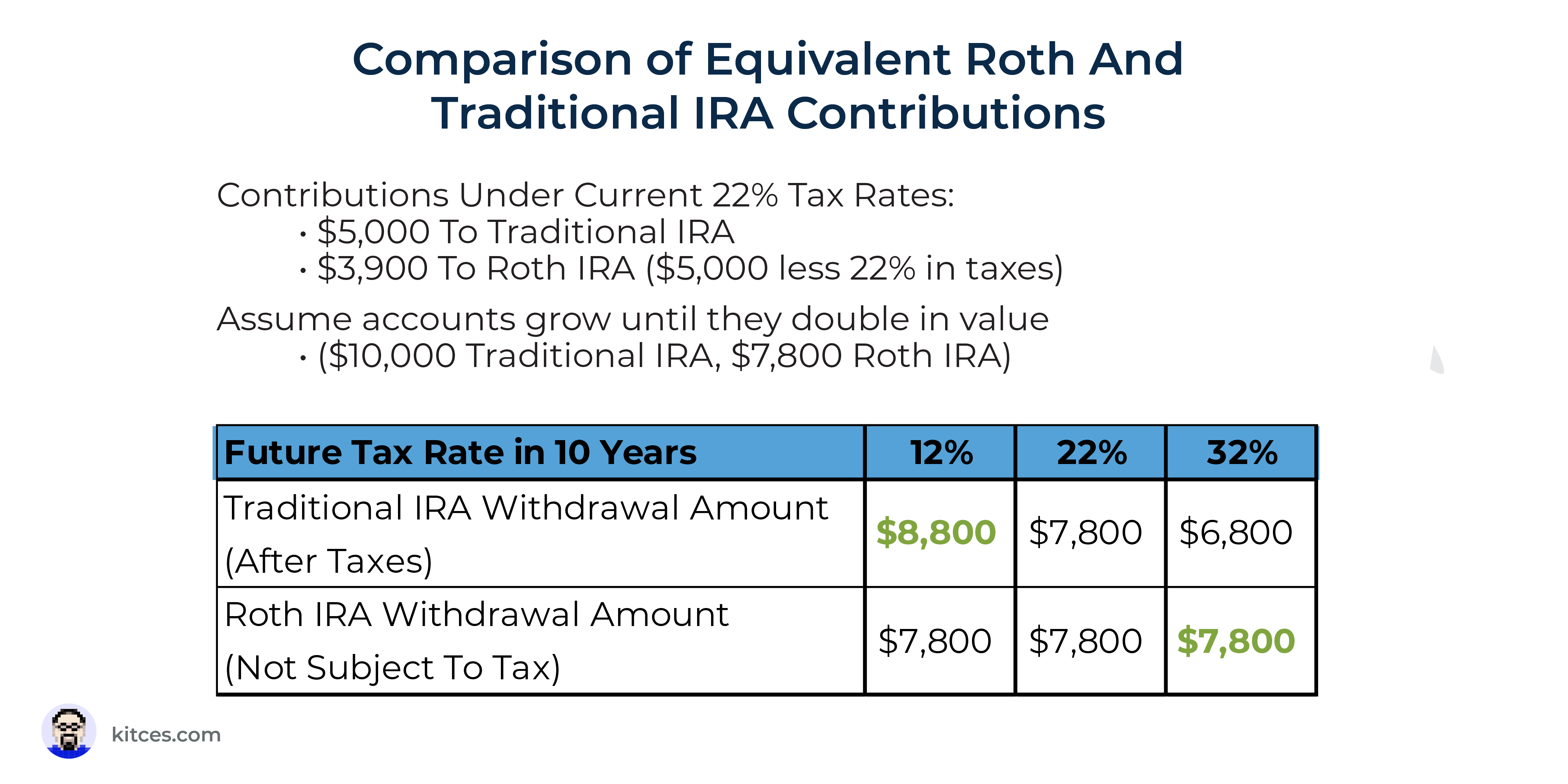

Example 1. Barney has $5,000 to contribute to his retirement account and must make a decision between a traditional retirement account and a tax-free Roth account.

If he decides to contribute the entire $5,000 to a traditional IRA, and if, over the years, the account grows to the point that it doubles in value, the $5,000 IRA will turn into $10,000. However, Barney wouldn’t be able to withdraw and use the full $10,000, because it is a pre-tax account and any withdrawals will count as ordinary taxable income. So, assuming that Barney is in a (future) income tax bracket of 22%, he will owe $2,200 in taxes on the withdrawal, and would only be able to spend $7,800 after taxes.

On the other hand, if he decides to make a contribution to a Roth IRA instead, he’ll need to hold back $1,100 in taxes (assuming a 22% tax bracket and no additional dollars available to pay the tax due), so only $3,900 would make it into the account. In the many years that follow, if the Roth IRA grows to the point that it, too, doubles (with the same investment generating a 100% cumulative return that he was making inside the traditional IRA), the account balance would grow from $3,900 to $7,800, all of which is available tax-free (assuming Barney meets the qualified withdrawal requirements).

The end result is that, regardless of which account he uses, Barney ends out with the same $7,800 of after-tax dollars to spend!

(It is also worth noting that the same principle applies no matter the expected growth rate of the account. If the funds were grown to 10 times the value, the Roth IRA would have grown to $39,000, and the traditional IRA would have grown to $50,000, which after applying a 22% tax rate would be… $39,000.)

As the above example shows, when the tax rates between when the contribution is made and distributions are taken don’t change, there is no advantage – nor any disadvantage – to the Roth IRA.

However, if an individual’s tax rates are expected to be different in the future, the outcome changes. If the future tax rate is higher than today, the tax impact on the traditional IRA brings its future value down below what the Roth would have been (making it better to have contributed to or converted into a Roth account today). Conversely, if their tax rate ends up being lower in the future than it is today, it turns out the best deal would have simply been to keep a good old-fashioned traditional retirement account, and simply pay the taxes on all the growth at that lower future rate.

Example 2: Ted, age 65, is single and expects his taxable income for 2022 to be $80,000, putting him in the 22% income tax bracket. He currently has $500,000 in a traditional IRA. He plans to claim Social Security in 2027, when he turns 70, at which point he expects to have a total of $50,000 in annual taxable income, keeping him in the 22% bracket.

Based on these expectations, completing a Roth conversion in 2022 will not impact the ultimate amount of money (net of taxes) that he will be able to withdraw from his accounts after age 70 when he begins collecting Social Security.

However, Ted plans to retire in 2023, when he is age 66, at which point he will live off of his taxable savings (with only $20,000 in annual taxable income) until he begins to receive Social Security payments at age 70, which will put him in the 12% income tax bracket from 2023 through 2026.

Because he will be in a lower tax bracket for these years (before his taxable Social Security income will put him back into the 22% bracket), Ted could take advantage of his temporarily reduced tax rate of 12% beginning in 2023 (compared to what it will be starting at age 70) and complete Roth conversions.

Notably, though, Ted must be cautious of how much he converts so that he can maintain his lower income tax rate. If he converts a sizable amount of his IRA, it will lift his income to the point that he’s no longer in the 12% bracket but into the 22% tax bracket, which would be no better than if he were to simply take withdrawals from his IRA in the future, at the same 22% rate.

Therefore, to achieve a better outcome, Ted converts only $20,000 each year before he turns age 70, to keep himself in the 12% tax bracket.

As the example shows, for those who face a lower tax rate today than they will in the future, the key is to find a ‘tax equilibrium’ by using Roth conversions (or contributions) to ‘fill up’ the lower tax brackets today… but only until it reaches the point that their tax rate is as high as it’s anticipated to become in the future (e.g., in retirement).

For instance, an individual in the 10% income tax bracket might convert enough to fill the 10% and 12% brackets, but stop before creeping into the 22% bracket. While someone already in the 22% income tax bracket might choose to convert just enough to keep them in the 22% bracket (or perhaps to fill up the 24% bracket, while avoiding the larger jump into the 32% bracket).

On the other hand, a high-income executive who’s already making $500,000+ and is in the 35% income tax bracket today, but expects to fall to ‘just’ $200,000/year in retirement (eligible for the 24% tax bracket as a married couple in retirement), would be better served to use a traditional retirement account that defers the income now (at his 35% tax rate) and is withdrawn in the future at the much-lower 24% rate!

Because an individual’s tax rates can change over time with changes in employment, wealth, and other circumstances, the optimal timing of Roth conversions can itself shift from one year to the next. In particular, rather than always maximizing Roth accounts with contributions and conversions, often the best strategy is to maximize pre-tax accounts during the high-income (working) years, to later Roth convert during lower-income (e.g., early retirement) years, before income lifts further in later retirement as RMDs begin to force dollars out of pre-tax accounts.

Example 3: Robin, age 57, has reached the pinnacle of her career, and is earning more than $300,000/year, which, as a single individual, puts her in the 35% income tax bracket.

Robin maximizes her annual contributions to her pre-tax 401(k) plan, which allows her to reduce her taxable income by $27,000 (at that 35% tax rate) for her retirement account contributions (including catch-up contributions).

Robin opts for early retirement this year, rolling over her 401(k) plan account into a traditional IRA. Furthermore, her income has dropped substantially, as her retirement spending is sustained with income from an $800,000 investment account and some real estate that gives her a total cash flow of $40,000/year, putting her at the top of the 12% tax bracket.

However, Robin’s pre-tax retirement accounts have accumulated more than $2,000,000. Given their potential growth over 15 years, these accounts could generate nearly $200,000/year by the time Robin reaches age 72 when she needs to begin taking RMDs. And this would likely catapult her back into the 35% tax bracket.

Consequently, Robin decides to begin engaging in partial Roth conversions now that she’s retired and in a low income-tax bracket – converting $120,000 of her traditional IRA to a Roth IRA and filling the 22% and 24% tax brackets, without pushing her into the 32% tax bracket. She continues to do this every year for 15 years, until she is required to start RMDs at age 72.

By converting her traditional IRA over the span of several years, Robin can build up a multi-million-dollar Roth IRA – not by contributing to or converting to a Roth account during her working years (when her tax rate was 35%), nor during her later retirement years after she begins RMDs (when her tax rate may again increase to 35%), but during the intervening lower-income years when she can generate tax-free Roth dollars at ‘just’ 22%–24% tax rates instead!

The key point is that strategically using Roth conversions can lead to greater after-tax income in retirement, but it is important to first assess current and expected future tax rates to determine whether (and how much) to convert in a given year!

How A Bear Market Puts Roth Conversions ‘On Sale’

While investors would prefer that the market go up continuously, regular declines are an unavoidable part of the investment process. And while a bear market typically has a negative impact on an investor’s portfolio, it does present tax planning opportunities. Because for those investors who were planning to make a Roth conversion anyway, a declining market effectively puts the conversion ‘on sale’ at a (hopefully) temporarily depressed value.

Notably, the reason that a down market puts Roth conversions on ‘sale’ is not simply because the market rebound means the converted IRA might grow at a faster rate. As shown earlier, thanks to the tax equivalency principle, faster growth rates don’t ‘just’ benefit a tax-free Roth IRA; they benefit the pre-tax growth of a traditional IRA as well, which nets out to the same after-tax value as long as the tax rate doesn’t change.

However, the reality is that tax rates often do change in the future, if only because the compounding growth of a retirement account can eventually add up to such a size that it’s ‘inevitable’ for future tax rates to be driven higher, either because of the sheer amount of pre-tax dollars that must be used to sustain future retirement spending, or because RMD rules begin to force the dollars out in an annual taxable event.

Yet, when an IRA’s value is ‘temporarily depressed’ in a bear market, it becomes possible for an individual to convert a larger percentage of their pre-tax account to a Roth account, making it possible to shift a larger portion of the future growth of the account into a Roth… without moving into a higher tax bracket as a more sizable portion of the account is converted.

Example 4: Marshall and Lily are married, and their combined taxable income of $200,000 puts them in the 24% income tax bracket.

Lily has a $1 million traditional IRA, and the couple wants to convert $140,000 of the account value this year, which they can do without leaving the 24% tax bracket.

If they had completed the conversion at the beginning of the year, the $140,000 Roth conversion would have turned 14% of Lily’s account into a Roth IRA. However, during a mid-year slump in the markets, Lily’s IRA suffers a 20% decline, bringing the account balance to $800,000. Which means that a $140,000 conversion would now allow the couple to shift 17.5% of the IRA into a Roth IRA, while still keeping them in the 24% bracket!

As a result, for the exact same tax cost on the $140,000 Roth conversion, when the market eventually recovers by 25% to bring the account back to its original value, instead of having $1 million (initial balance) – $140,000 (converted amount) = $860,000 in a traditional IRA and $140,000 in a Roth IRA, the couple will hold $800,000 (initial balance) – $140,000 (converted amount) + $165,000 (gain from 25% market recovery) = $825,000 in a traditional IRA, and $140,000 + $35,000 (gain from the 25% market recovery) = $175,000 in a Roth IRA.

As the example above illustrates, bear markets can create an opportunity to accelerate the shift from traditional IRAs to Roth IRAs via conversions – without adding to the tax burden of the Roth conversion – by allowing more of the account to be converted at a bear-market-‘discounted’ rate.

The Best Way To Pay Taxes Due On (Discounted) Roth Conversions

Because a Roth conversion typically creates a tax liability (unless taxable income after the conversion remains below the standard deduction threshold), investors must find a way to pay the tax burden. And while there are a range of options to source the funds to pay the tax burden, using cash on hand, whenever possible, will typically be the best choice.

As in the end, the tax equivalency principle – that it doesn’t matter whether dollars are held in a traditional or Roth retirement account, as long as tax rates don’t change – is only applicable if the dollars remain fully invested in tax-preferenced accounts in all scenarios. If the reality is that the tax liability can be paid with money that wasn’t invested in the first place – e.g., from available cash reserves instead of taken from the funds being converted– then the tax-free Roth account enjoys a market rebound that the money used to pay the taxes never would have benefitted from anyway!

Example 5: Sandy has a traditional IRA with a balance of $100,000. During a market downturn, his balance drops by 20%, bringing his account balance down to $80,000. He believes that it would be to his advantage to do a Roth conversion in 2022 on the full $80,000 balance now, at his current 22% tax bracket while his IRA balance is ‘down’ 20%.

If Sandy has to use the dollars in his IRA to pay the tax liability – amounting to $17,600 at a 22% rate – then his net Roth conversion will be $80,000 – $17,600 = $62,400, which, after the market rebounds by 25% (bringing the account back to its original value), will grow to $78,000.

Notably, if Sandy were to simply keep the $80,000 in his traditional IRA until it, too, recovers after the bear market, its value would rise back to its original $100,000… which, at Sandy’s 22% tax rate, would give him (the same) $78,000 of spendable wealth.

But what if Sandy also has $25,000 available in a bank or checking account that could potentially be used to fund the taxes on his IRA? If Sandy allows his traditional IRA to recover, he would have a $100,000 traditional IRA and a $25,000 bank account, and a true net worth of $103,000 (as $22,000 of the bank account will eventually be consumed by the taxes from his IRA).

However, if Sandy does the Roth conversion while the account is down at $80,000 and uses $17,600 of his bank account to pay for the tax liability, after the market recovery he will have a $100,000 tax-free Roth IRA and $25,000 – $17,600 = $7,400 remaining in his bank account, for a total net value of $107,400… an improvement of $107,400 – $103,000 (net worth without the Roth conversion) = $4,400 by using his bank account to fund his discounted Roth conversion!

As the example above illustrates, using cash to fund a discounted Roth conversion is particularly effective, because when markets are down and the bear market is expected to recover, the Roth IRA can enjoy more of a rebound while uninvested cash, by definition, won’t. Consequently, using an ‘idle’ uninvested asset to fund the tax benefits of a fully invested (Roth) account results in greater wealth.

A similar – albeit not quite as favorable – outcome also occurs by selling taxable investments to generate the cash needed for the taxes on the conversion. As while the investment account may also be down due to the bear market – and thus less desirable to sell to pay the taxes on the Roth conversion – this is still likely to be a more tax-efficient choice (than using a portion of the converted amount to pay the taxes) because the taxable account grows in a less tax-efficient manner (so-called ‘tax drag’ due to the taxation of dividends and capital gains). Especially if the sale can target higher-cost-basis assets (that don’t themselves generate an additional capital gain), and/or if there are any tax losses that can be harvested to offset any embedded gains that are triggered on the sale of taxable investments.

Still, though, the best option to pay the tax due on a discounted Roth conversion typically is to be funding it with available cash. For those who are working, this could be done by increasing tax withholdings throughout the year to cover the additional tax due. An alternative option is to deploy available cash savings to make an estimated tax payment to cover the taxes on the conversion. Because again, at a time when rates on savings accounts and most other savings vehicles are well below 2% (and in some cases are near 0%), the ‘return’ on using this cash used to pay the taxes rather than using a portion of the conversion or selling appreciated investments is likely to outweigh any interest received from the savings.

In the end, the benefits of getting Roth conversions ‘on sale’ during a market downturn depend in large part on how an individual sources the funds to pay the taxes on the conversion. And when it comes to paying the taxes due, cash is usually king, as while the individual might not have wanted to invest the money in the savings account, by using it to pay the taxes due on the Roth conversion, the savings is effectively paying for the future tax-free growth in the Roth account!

Strategies For Managing Discounted Roth Conversion Timing

While it’s appealing to consider a Roth conversion while markets are down to take advantage of a bear market, as with any transaction that is ‘timed’ to a bear market, there’s always the risk that the market will go down further. Which, in the context of managing a discounted Roth conversion in a bear market, raises the question of whether ‘now’ is the time to do the Roth conversion, or if it would be better to wait until the market potentially declines further… at the risk that it rebounds in the meantime and the opportunity is lost.

Fortunately, because Roth conversions can be made throughout the year in any amount, there are different strategies that can be used to maximize the value of the conversions, minimize potential client regret… and avoid running afoul of the tax rules that govern conversions when trying to fill ‘only’ a particular tax bracket.

Using Roth-Conversion-Cost Averaging

Many advisors and their clients are familiar with the concept of ‘dollar-cost averaging’, in which an investor allocates a fixed dollar amount to buy a particular investment at regular intervals, rather than making a single lump-sum investment, to avoid being overly reliant on ‘timing’ the market at a particular investment moment. A similar concept can be used with discounted Roth conversions, where there is a similar challenge of figuring out how to time a conversion when it’s uncertain how markets will perform during the remainder of the year.

Example 6: Continuing the earlier Example 5, Sandy has determined with his advisor that $80,000 is an optimal Roth conversion amount for 2022, which allows him to fill (but remain) in his current 22% tax bracket. Furthermore, Sandy wants to do the transaction on a ‘discounted’ basis while his IRA balance is ‘down’ 20% due to the ongoing bear market, but he is concerned that he may be missing out on an even better deal by waiting to see if the market declines further.

To combat this uncertainty, Sandy’s advisor recommends a Conversion-Cost Averaging approach of converting $20,000 now, in June, and an additional $20,000 every other month through the end of the year, which will still cumulatively add up to four partial Roth conversions of $20,000 each for a total of $80,000, spread out across the year, allowing him to average into the volatile markets over time.

Depending on the size of the Roth conversion and the willingness to engage in the ‘hassle’ of incremental additional conversion rollovers, conversion-cost averaging can be implemented across two transactions within the year, four transactions (e.g., quarterly, or every other month for the remainder of the year), or even more frequently (e.g., monthly throughout the year).

At some point, it may be deemed that the potential tax savings of averaging isn’t worth the time it takes to engage in the additional paperwork (for instance, conversion-cost averaging a $6,000 conversion at $500/month each month of the year!), though the ‘ideal’ threshold may vary depending on the client and their preferences.

Either way, though, conversion-cost averaging offers several core benefits. First, if the market appreciates during the course of the year, at least a portion of that appreciation will be earned within the Roth IRA (thanks to the initial tranche of the conversion cost averaging strategy). This would be beneficial compared to waiting and just doing a single Roth conversion later (e.g., at the end of the year), because all growth, in that case, would have taken place in the pre-tax account if the market rebounded quickly.

Alternatively, if the market declines during the course of the year, the client will be making at least a portion of the year’s conversion total at lower valuations as the market slips further (which helps to ameliorate some of the potential regrets of converting too much up front, albeit not as much as if the full conversion took place after the drop with perfect foresight).

An additional benefit of conversion-cost averaging is the ability to make ‘course corrections’ on the target conversion amount throughout the year as the client’s tax picture becomes clearer. For example, if a client receives a raise or an unexpected bonus during the year, the monthly conversion amount could be reduced (or stopped altogether) to avoid putting the client in a higher tax bracket. Alternatively, if the client decides to leave their job mid-year, the monthly conversion amount could be increased to convert more dollars while remaining in the desired tax bracket.

Example 7: Continuing the prior Example 6, it turns out that, mid-way through the year, the bear market and the underlying economic recession become so bad, that Sandy is laid off from his job, resulting in a significant drop in his annual income.

As a result, even though the original plan had been to convert $20,000 every other month using a conversion-cost averaging strategy (for a total of $80,000 this year) to fill up the 22% tax bracket, due to Sandy’s decreased income from losing his job, Sandy and his advisor decide to increase the remaining Roth conversions if the market stages a rally, giving him more money in the account to convert.

It turns out that after Sandy converts $20,000 in June, a 10% market rally leads his IRA (at $60,000 after the June conversion) to grow to $66,000. And so, Sandy increases the final 3 conversions to $22,000 each, boosting his total Roth conversions to $86,000 this year instead of ‘just’ $80,000, to take advantage of the additional room in the 22% tax bracket after Sandy lost his job.

Of course, in the end, the ‘ideal’ outcome for a discounted Roth conversion would simply be to do the conversion right at the market bottom, converting the maximal amount at the most discounted value. However, given the inherent unknown nature of market volatility and trying to perfectly time the market, conversion-cost averaging helps to minimize the risk of regret about getting the timing wrong – converting too much too early or, in retrospect, waiting too long – by spreading out the conversion into smaller transactions throughout the year.

The Benefits Of Roth IRA Conversion “Barbelling”

Before 2018, individuals who made Roth conversions could later decide to ‘recharacterize’ them back to the original pre-tax account. This was useful for those whose income increased during the year, allowing them to convert more than enough to fill a tax bracket, and then later simply reverse early-year conversions for whatever excess amount turned out to have put them in a higher tax bracket and was in retrospect unnecessary.

In addition, when the market declined in value during the year (negating the benefits of tax-free growth in the Roth account), recharacterization allowed taxpayers to move the converted amount back into their pre-tax account, eliminating taxes due on the conversion that declined, and giving them a chance to re-convert at the reduced account value the following year. However, the Tax Cuts and Jobs Act of 2017 eliminated the ability to recharacterize Roth conversions, increasing the importance of not converting ‘too much’ early in the year (because an individual can now no longer reverse the conversion if their circumstances change!).

Recalling that partial Roth conversions can be made throughout the year, one option that takes advantage of tax-free growth on converted dollars throughout the year (while avoiding converting too much) is to use a ‘Roth barbell’ strategy. With this strategy, up to two conversions per year are carried out; one conversion is made as early in the year as possible, and a second conversion is made much later in the year when the client’s tax picture is clearer (thus forming a ‘barbell’ shape with two big conversions at either end of the year, with little or no conversion activity in between).

With this Roth barbell strategy, the initial converted amount gets the benefit of tax-free growth (if the market rises), while the second conversion can be adjusted based on the client’s actual taxable income for the year (and lets the client take advantage of the ‘sale’ on Roth conversions if the market declines during the year).

Example 8: Billy is single and runs his own fitness studio. While his income has averaged $120,000 for the past few years, it tends to vary anywhere from $90,000 to $140,000 from year to year.

Because his income has averaged $120,000 for the past few years, Billy and his advisor anticipate they’ll want to convert approximately $50,000 of Billy’s traditional IRA to a Roth IRA this year to fill out the 24% tax bracket (which tops out at $170,050 for single filers). However, if Billy has a better year and receives $140,000 of income, the Roth conversion might need to be reduced to only $30,000 to maintain his 24% tax bracket. Alternatively, if business doesn’t do well and Billy only makes $90,000 of income, then he can convert as much as $80,000.

Accordingly, Billy’s advisor recommends a Roth conversion barbell strategy, where Billy initially converts $30,000 – the amount he anticipates for the higher-income scenario – and then waits until the end of the year to see how his business does. If it does well, he may only need to convert another $20,000 (or nothing at all if it does really well and Billy’s income alone manages to fill up the rest of his 24% tax bracket); if it doesn’t do as well, he may be able to convert up to $50,000 or more, depending on how much income his business brings in.

Notably, Roth-conversion-cost averaging and Roth barbells can be used in conjunction with each other as well – for instance, doing a sizable Roth conversion for the initial amount of the barbell to take advantage of current market values, and then a series of smaller conversion cost averaging transactions to both average into the conversion over time, and to be adjusted at year-end with a final conversion amount to account for the client’s individual income tax situation if/when it shifts.

Isolating IRA Basis For More Tax-Efficient Discounted Roth Conversions

Although contributions made to a traditional IRA usually consist of pre-tax dollars, there are occasions when post-tax dollars are included as well. For instance, nondeductible contributions are made when a taxpayer (or their spouse) is an active participant in an employer-sponsored retirement plan, and their Modified Adjusted Gross Income (MAGI) exceeds the applicable limit for their filing status. Rollovers originating from an employer-sponsored retirement plan can also include after-tax funds (which then end out as after-tax dollars in the rollover IRA) if the employer’s retirement plan allowed for after-tax contributions in the first place.

When traditional IRA accounts hold both pre-tax and post-tax dollars, the balance will be subject to the “Pro Rata Rule”, which stipulates that, in general, distributions from a taxpayer’s IRA maintain the same ratable proportion of pre-tax and post-tax funds as the taxpayer’s total IRA balance. Which means that Roth conversions from accounts with a mix of pre-tax and after-tax funds cannot be made on a solely pre-tax or after-tax basis.

For those considering Roth conversions, converting after-tax funds is superior to converting pre-tax funds, as there’s no taxable event on the conversion of those dollars – they are already after-tax – even as all future growth is shifted from taxable (within an IRA) to tax-free (within a Roth IRA!). Therefore, clients can stand to benefit by ‘removing’ pre-tax dollars from their traditional IRA so that only post-tax dollars (and their associated gains) would be converted, and the Pro Rata Rule would no longer apply.

For clients with access to an employer-sponsored plan that allows for rollovers of IRA funds into their employer plan, after-tax dollars in the IRA can be isolated by moving pre-tax IRA assets into the employer plan. Since IRA-to-plan rollovers are restricted to pre-tax dollars – it’s actually prohibited to roll after-tax dollars into a 401(k) plan! – such ‘roll-ins’ can essentially serve to remove the pre-tax balance of a Traditional IRA, maximizing the after-tax balance available for the Roth conversion.

Example 9: With the help of his advisor, Ted decides to make a $50,000 Roth conversion this year. He has a traditional IRA valued at $300,000, which consists of $230,000 of pre-tax and $70,000 of after-tax contributions that have accumulated over the years.

To maximize the tax efficiency of the Roth conversion, Ted establishes an individual 401(k) plan for his architectural consulting business, and then completes a roll-in of the $230,000 of pre-tax funds into the 401(k), leaving only the $70,000 of after-tax dollars in the IRA.

Now, Ted is able to convert the entire $70,000 amount to his Roth IRA from a solely after-tax IRA balance of $70,000, and will not have any tax liability on the Roth conversion because it was done only with after-tax dollars!

For those over age 70 ½, another strategy available to increase the proportion of IRA after-tax dollars is to make a Qualified Charitable Distribution (QCD), as these distributions are also restricted to be done only with pre-tax dollars within the IRA. Thus, as in the case of roll-ins into an employer-sponsored plan, QCDs effectively decant away the pre-tax portion of the IRA account balance, leaving a larger percentage of after-tax funds in the account for Roth conversions.

Maintaining Awareness Of A Dynamic Tax Situation

While Roth conversions can be a valuable tactic (especially in a down market when they go ‘on sale’), their value will depend in large part on an investor’s current and future income tax brackets. Recalling that Roth conversions (and contributions) are preferable when the tax rate is lower this year than it will be when the funds are withdrawn, many investors who are already in high tax brackets would still likely be better off not doing a Roth conversion at all… or at least, waiting until the future when their tax rates are lower, and then doing a Roth conversion at their lower future tax rates.

As a result, those in high tax brackets are often best served to make contributions into traditional pre-tax accounts (getting any available tax deduction now, while they are in a relatively high tax bracket), to further benefit by doing future Roth conversions after waiting for the year when their rates are lower!

Ultimately, the key point is that a market downturn presents an opportunity to convert a higher percentage of a pre-tax account to a Roth account for the same amount of taxable income, for those who otherwise should be doing a Roth conversion given their current tax rate. Nevertheless, the conversion has to make sense for a particular individual, given their current and expected future tax rates in the first place.

In addition, for those who want to do Roth conversions, being able to pay the taxes due on the conversion with cash will get more benefit from the conversion (though there is still at least some value to using taxable investment accounts to cover the tax liability).

And by using conversion-cost averaging or barbell strategies, an advisor can help ensure that the conversion does not put a client into a higher tax bracket now, which can undermine the benefit of the Roth conversion to begin with.

In the end, while a down market can be challenging for both advisors and their clients, the opportunity for Roth conversions ‘on sale’ during these periods (when appropriate!) offers advisors a chance to generate tax alpha for their clients!

{kind=link}