Kyle Prevost, editor of Million Dollar Journey and founder of the Canadian Financial Summit, shares financial headlines and offers context for Canadian investors.

With earnings season in full swing, there’s a lot to catch up on this week, as we try to make sense of the markets that defy being described by a simple narrative.

For some time, I’ve been writing about inflation—and the accompanying responses from governments and central banks around the world—as a dominant theme moving the markets. That appeared to be largely the case this week again, as the U.S. Federal Reserve raised its benchmark lending rate by the expected amount of 0.75%. This brings the key rate to 2.5% and it’s now equal to that of the Bank of Canada.

The markets appeared to take the move in stride, and they seemed reassured by Federal Reserve chair Jerome Powell’s comments in regards to possibly easing off the interest rate throttle in future months. That’s provided inflation numbers begin to make their down from recent highs.

While Wal-Mart Inc. (WMT/NYSE) broke news early in the week with a recession-y announcement that its full-year profit would be falling 11% to 13% this year. Many other companies appear to be right on track when it comes to bottom lines.

Commentators continue to debate exactly what kind of recession we’re in or not in, but I think sometimes the actual businesses of profits can get lost within these abstract debates.

No need to panic over technology earnings

Here I summarize the key earning reports. All amounts in this section are U.S. currency.

Microsoft (MSFT/NASDAQ): Microsoft shares were up 5% on Tuesday, despite small misses on earnings and revenues. Investors agreed to agree with the company and its long-term guidance to remain unchanged for the rest of year. The strength of the U.S. dollar was cited as the main reason for not quite meeting expectations. Earnings per share were $2.23 (versus $2.29 predicted) and revenues were $51.87 billion (versus $52.44 billion).

Alphabet (GOOGL/NASDAQ): In a similar story, Alphabet shares also rose despite investors receiving less-than-stellar news on the quarterly earnings call. Earnings per share came in at $1.21 (versus $1.28 predicted), and revenues were $69.69 billion (versus $69.9 predicted). Given the headwinds of the U.S. dollar and a supposed advertising budget crunch, most investors are breathing a sigh of relief at the relative strength of its bottom line.

Meta/Facebook (META/NASDAQ): Facebook shareholders looked for the thumbs-down button as the social media giant posted earnings of $2.46 per share (versus $2.59 predicted) and slight revenue miss of $28.82 billion (versus $28.94 billion expected). Revenue was down 1% due to “continuation of the weak advertising demand environment we experienced throughout the second quarter, which we believe is being driven by broader macroeconomic uncertainty,” according to CFO David Wehner. Meta mastermind Mark Zuckerberg responded to investor fears by stating: “This is a period that demands more intensity, and I expect us to get more done with fewer resources.”

Amazon (AMZN/NASDAQ): Fear had dominated trading for retailers everywhere after Wal-Mart’s shocking news at the start of the week. Consequently, when Amazon announced it lost “a little money” instead of “all the money,” the stock bounced more than 13% in after-hours trading on Thursday. Earnings per share came in at a loss of $0.20 (versus a predicted profit of $0.12), but top-line revenues actually beat expectations at $121.23 billion (versus a predicted $119.09 billion). Clearly the inflation battle continues to be the story behind those revenue and profit numbers.

Apple (AAPL/NASDAQ): Apple continues to impress in all interest rate environments, as it innovated its way to an earnings per share of $1.20 (versus a predicted of $1.16) and earnings of $83 billion (versus $82.81 billion predicted).

Shopify (SHOP/TSX): In Canada, Shopify failed to keep pace with their more mature American tech cousins and announced a loss of $0.03 Canadian per share (versus a predicted profit of $0.03 per share). Oddly, shares leapt nearly 12% on Thursday amidst a general tech rally, after falling 14% the day before on big layoff news.

It’s hard to compare the advertising-heavy business models of Alphabet and Meta with the worker world of Amazon’s warehouses, but it’s clear that the demand for sales isn’t the issue—it’s simply a matter of cost control in an inflationary environment going forward. That said, as these companies go from revenue growth darlings to mature cost-conscious long-term profit generators. The New York Times agreed, describing the tech giants as “resilient.”

Old-fashioned durable advantage never goes out of style

With many investors looking to weather the storm in calmer waters after they’ve watched their technology and consumer discretionary stocks get crushed over the last few months, reliable old companies with proven profit margins have begun to get more attention.

It’s unlikely any of the names below will ever see the eye-popping growth they enjoyed a time ago (nevermind that of a tech darling), but this week’s earnings revealed that these corporate stalwarts mostly continue to do what they do best—make money by utilizing long-term competitive advantages.

3M (MMM/NYSE): The folks at 3M announced the big news that it will be spinning off its health-care business into a separate publicly traded company. I’m usually a fan of companies that understand they are better off focusing on core business. Subsequently, I like the general idea of creating a separate entity that will focus on oral care, health-care IT and biopharma. This news was the cherry on top of a tasty earnings report that saw earnings come in at $2.48 per share (versus $2.42 predicted) and a small revenue beat as sales topped $8.7 billion. Share prices of 3M were up nearly 5% on Tuesday after the earnings call.

General Electric (GE/NYSE): The bright lights at General Electric used its massive growth in jet engine business to power their quarterly earnings. Earnings per share for the quarter were $0.78 (versus $0.38 predicted). Revenues also handily beat analyst estimates.

McDonald’s (MCD/NYSE): McDonald’s keeps serving up profits, as its $2.55 earnings per share topped analyst estimates of $2.47. The fast-food king did see revenues come in slightly lower than expected due to the closure of its Russian and Ukrainian locations. Canadian investors can invest in McDonald’s through the MCDS/NEO CDR.

UPS (UPS/NYSE): A strong U.S. dollar and even a slightly declining volume of packages weren’t enough to slow down UPS. The delivery giant raised rates and posted earnings of $3.29 per share (versus $3.16 predicted). Revenues came in at $24.77 billion (versus $24.63 predicted).

Coca-Cola (KO/NYSE): Coca-Cola reported sweet-tasting earnings and revenues this week. Earnings came in at $0.70 (versus $0.67 predicted), and revenues were $11.3 billion (versus $10.56 predicted).

Norfolk Southern (NSC/NYSE): Norfolk Southern profits arrived at the station just slightly behind schedule as its earnings per share for the quarter was $3.45 (versus $3.47 predicted). Both earnings and revenues were up substantially from last year.

Texas Instruments (TXN/NASDAQ): Calculators showed a jump of roughly 2% for Texas Instruments after earnings for the quarter came in at $2.45 per share (versus $2.13 predicted) and revenues topped $5.2 billion (versus $4.65 predicted).

It’s tough to tease out much of a “through line,” other than that these companies continue to win the battle against inflation. For the most part, they’ve been able to keep costs under control while passing along increased prices to consumers without much negative blowback. I recently wrote on my site about similar inflation-beating stocks for Canada.

Is it time to test drive Ford and GM Stock?

Ford (F/NYSE) and GM (GM/NYSE) have been living in Tesla’s shadow for several years now, in terms of investor sentiment and internet hype. When vehicle sales spiked during the pandemic, shares of both companies got a momentary reprieve from their downward trajectory. With both stocks down nearly 50% from their January highs, it may be time to check in on these two legacy automakers. Regardless of what you think of their cars, trucks and SUVs, there is almost always a price point when profitable companies become a good value for investors.

Like a rock—that’s how GM’s stock fell

It was a rough quarter for GM (GM/NYSE) as it announced its adjusted earnings per share as $1.14 (versus $1.20 predicted). Revenues were up to $35.76 (versus $33.58 predicted). The key takeaways from the earnings call were that parts shortages had contributed to being unable to ship more than 100,000 vehicles.

CEO Mary Barra released a statement, saying, “We have been operating with lower volumes due to the semiconductor shortage for the past year, and we have delivered strong results despite those pressures. There are concerns about economic conditions, to be sure. That’s why we are already taking proactive steps to manage costs and cash flows, including reducing discretionary spending and limiting hiring to critical needs and positions that support growth.”

Crucially, Barra reported that GM’s investor guidance for 2022 would remain unchanged, stating “This confidence comes from our expectation that GM global production and wholesale deliveries will be up sharply in the second half.”

Ford, making harder-working electric vehicles

Ford (F/NYSE) had a more upbeat earnings call, as it announced a massive earnings beat of $0.68 per share (versus $0.45 predicted) and revenues of $37.91 billion (versus $34.32 billion predicted). Revenues jumped from $24.13 billion during the second quarter last year.

In other notable comments, Ford shared that it will begin reporting results from three distinct verticals next year: Ford Blue (the old-school internal combustion engines), Ford Model e (electric vehicles) and Ford Pro (commercial vehicles).

The car maker also stated that it’s fully stocked with necessary supply lines to make 600,000 electric vehicles (EV) next year, and planned for that number to rise to two million per year by 2026.

GM and Ford takeaways

In the short term, the narrative battle of “cars are cyclical, and we’re headed into a recession” versus “everyone is trying to buy a car right now, and dealerships are selling them as soon as possible” will determine which way both companies’ share prices go.

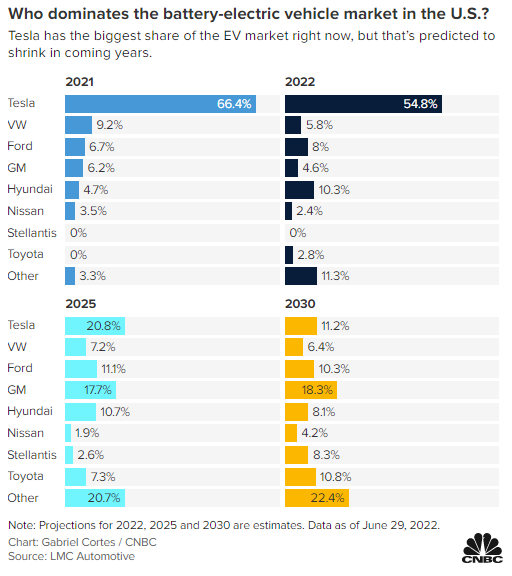

In the long term, though, I think the broader debate over how much of the market Tesla will end up with versus the legacy automakers is still very much open for debate. Tesla investors continue to price the stock for world domination—and maybe they’re right—but it’s tough to ignore the value potential of Ford and GM, if they are able to execute on their EV and cost control plans.

While Tesla’s engineering, marketing and brand management are clearly unparalleled at this point, there will come a time when this hard math will begin to matter. Here are their price to earnings ratios (P/E).

| Vehicle company | P/E |

| Tesla | 100 |

| Ford | 4.8 |

| GM | 5.8 |

With both Ford and GM planning massive investment in EVs, investors are betting that Tesla will absolutely crush the legacy competitors going forward. That’s not a bet I’m willing to make.

Personally, I really like Ford’s 3% dividend yield (which they just raised by $0.15 per share), as it shows a company with the confidence to reward shareholders today, in addition to solid long-term prospects.

As someone who grew up in a rural community, I know many folks whose only vehicle purchasing decision every few years was what colour their F-150 should be. I really think the new electric version of the classic pickup truck might be a watershed moment for EV adoption.

With a starting price point of USD$40,000, this car will immediately be price competitive with the internal combustion trucks currently on the market. Ford has stated the new model can do everything the traditional workhorse can, by supporting a 2,000-pound payload and a 10,000 pound towing capacity. That’s in addition to 130 more horsepower than the current F-150 and a much faster 0-60 speed. Finally, Ford noted that the pickup’s battery could be called upon to power a home for up to 10 days in the event of a blackout.

I know several people who will be convinced to take a hard look at an EV for the first time when they see those numbers.

Canadian railways on track for record profits

My website recently published an article on the dominant market position of Canadian railway stocks and why that made them so valuable. It appears the market largely agreed this week, as someone forgot to tell Canada’s two railway kings that we are supposed to be in a recession.

Canadian National Railway Co (CNR/TSX): Canada’s largest railway reported profits had skyrocketed 28% year-over-year. Earnings per share were $1.93 (versus $1.75 predicted) and revenues were record-setting. Freight rates were up and cost increases were mostly controlled despite inflationary concerns. Clearly there’s a reason why Bill Gates is CNR’s biggest shareholder.

Canadian Pacific Railway (CPR/TSX): As CPR shareholders continue to wait on approval for its big Kansas City Southern acquisition, it enjoyed a solid quarter as well. Earnings per share were $0.82 (versus a predicted $0.80) and revenues of $2.20 billion.

The bottom line is that—despite the inflation fear-mongering, re-emergence of fixed income as a viable alternative, and the crashing to earth of high-leverage growth businesses–large companies with durable competitive advantages continued to make money and reward shareholders this week.

Kyle Prevost is a financial educator, author and speaker. When he’s not on a basketball court or in a boxing ring trying to recapture his youth, you can find him helping Canadians with their finances over at MillionDollarJourney.com and the Canadian Financial Summit.

The post Making sense of the markets this week: July 31 appeared first on MoneySense.

{kind=link}