Executive Summary

Cash tends to exist at the forefront of individuals’ day-to-day lives for many reasons: as a stable savings vehicle for near-term goals, a safety net for unforeseen emergency expenses, and, of course, to pay for daily living expenses, just to name a few. And this nearness to daily life means that cash – and how it is used – is also often at the forefront of individuals’ minds. In general, this means that people are more likely to be more aware of how much cash they’re holding than the other numbers in their financial life, like the balances on their retirement accounts (which, being less ‘immediate’ in their intended purpose, are not often at the forefront of most people’s minds to the same extent that cash is).

However, despite the impact that cash may have on a person’s mindset, advisors have traditionally spent little time advising clients on what to do with their cash – except simply to tell them not to hold too much for risk of losing value to inflation. With recent economic changes, though, there are renewed opportunities for advisors to help clients manage their cash more effectively. For example, bank account balances have increased sharply in the last three years due to governmental programs in response to the pandemic and also to generally rising wages and salaries. At the same time, the Federal Reserve has recently raised key interest rates, which has resulted in higher yields on bank accounts, CDs, and other cash-like assets. Which means that, for the first time in years, individuals might start earning non-trivial yields on their cash, and potentially have a higher amount of cash on hand to manage as well. And so advisors have an opportunity to add value in new ways by advising clients on the questions of how much cash to hold and where to keep it!

While high-yield savings accounts at online banks have been a popular place for storing cash for the last decade, in more recent years the FinTech world has developed more options that could create more value for advisors and their clients. One example is cash management accounts developed by digitally-focused broker-dealers and robo-advisors, which while similar to savings accounts from a customer’s perspective, provide key features (like higher FDIC coverage limits and a streamlined experience with the customer’s existing investment accounts) that distinguish them from traditional savings accounts.

Though many of these accounts exist primarily to serve retail customers of broker-dealers and robo-advisors (which might make advisors hesitant to recommend them for fear of introducing customers to a potential competitor), there are also multiple options for cash management accounts developed solely for clients of financial advisors. With these options, advisors can offer a cash management service within the rest of their financial planning ‘ecosystem’, offering competitive yields on cash and FDIC coverage limits of up to $25 million, without having to send clients out to other financial institutions that might want to lure them away from the advisor!

Ultimately, the key point is that while the current economic provides a particular opportunity to focus on cash management, the reality is that the value of cash management can be ongoing despite the ebb and flow of economic conditions. For advisors looking to be paid directly for this value, a small, flat cash-management fee might be feasible without eating up too much of the yield on clients’ cash. However, in most cases, cash management may actually be a worthwhile ‘free’ service – both only as a differentiator for prospects, but also as a way to renew existing client relationships and continually provide ongoing value!

The Importance Of Cash In Everyday Life

Cash is an essential part of many people’s everyday lives. Indeed, people are often much more involved with and aware of their cash on an everyday basis than their invested assets. This can be illustrated in a simple way: if you had to estimate the value of your bank accounts and your investments without looking them up, which one do you think you would be able to guess more accurately?

I conducted a very unscientific survey on LinkedIn using this question, and of 665 respondents, over three-quarters replied that of the two, they could more accurately guess their bank account value. And because the respondents were heavily made up of financial advisors who are already predisposed to be tuned in to their investments, the poll most likely understates how much more aware the general public is of their cash than their investments.

There are several plausible explanations for why cash tends to be closer to one’s top of mind. One possible reason is the inherently more stable value of cash relative to most other investments, which makes it easier to glance at a bank account balance one day and have a reasonable idea of the next day’s balance than it is to estimate the daily balance of a constantly fluctuating investment account.

Another is that financial experts, including advisors, tend to actively encourage investors not to fixate on the everyday value of their portfolios in order to ignore short-term fluctuations and remain invested for the long term.

But an alternative explanation – and one that is potentially relevant for financial advisors – is that the reasons for holding cash in the first place tend to be much closer to peoples’ consciousness.

The most basic way most people use cash is to pay for their day-to-day living expenses, which requires a certain knowledge of one’s bank account balance simply to ensure they don’t run low on (or out of) funds. For instance, if your mortgage payment is due next week, you know exactly how much it will cost and how much you will need in your checking account to make sure you have enough to cover it.

Cash is also the most common vehicle used to save for near-term goals – that is, the goals that are close enough for a person not to want to risk their savings on the fluctuations of the markets. If your child’s first college tuition payment is due in six months, those funds are likely to be in cash, or something else very liquid, to avoid being subject to the market’s ups and downs.

Finally, people often hold cash in their emergency funds for unexpected expenses or unemployment, or as just a ‘safety net’ for other unknown risks. Though it might be a person’s hope that they will never need to use these funds, the presence of this extra cash provides important peace of mind that investments don’t. Indeed, there is evidence that individuals’ “liquid wealth” (i.e., cash in checking and savings accounts) is correlated with their sense of life satisfaction and financial wellbeing and, in fact, is more strongly associated with those feelings than other measures like income, investment balances, or debt. In other words, having a healthy amount of cash on hand appears to make people feel better about their overall financial health, regardless of how much they might have stashed in retirement accounts or other investments.

What’s common about many of the reasons for holding cash is that they are generally near-term in nature – and this nearness in time also tends to bring cash more to the forefront of the individual’s mind. By contrast, invested assets often are intended for longer-term goals like retirement. And when those goals are far enough away, people may not have more than a vague sense of what they are actually saving for – if they even have a fully-formed goal to begin with – making it less important to know exactly how much they have saved for that goal at that moment (so long as they are at least making progress towards it). If you know you want to retire sometime in the next 20 years but have no idea what that retirement will look like, it isn’t possible to have any more than a general sense of how much you ‘should’ have in your 401(k) plan. In other words, keeping tabs on your retirement accounts every day won’t tell you as much about your ability to meet your long-term goals as monitoring cash accounts will tell you about your ability to meet your short-term goals.

Why Advisors Don’t Advise On Cash Management

Because of the important role cash tends to play in a person’s life, it makes sense for their cash balance to be included when considering their overall financial picture, both in terms of their ability to achieve their goals and their sense of financial wellbeing. Yet many financial advisors spend little (if any) time advising their clients on what to do with their cash. And when the subject does come up, it is often in the context of talking about the disadvantages of holding cash and the importance of not holding too much cash that will lose value to inflation over time.

But beyond simply advising clients not to hold too much of it, advisors don’t spend much time talking about the cash that does remain on the balance sheet. Which, given the importance of cash in peoples’ everyday lives, seems like an important oversight and a missed opportunity for advisors to provide value – both in terms of real dollars and the client’s sense of financial security that an ample cash cushion provides. Because cash is such a central part of our financial lives, almost everyone needs to consider at least the basic questions of how much cash to hold and where to keep it; it makes sense, then, that clients would expect (and value) some input on these questions from their financial advisors.

Why have advisors generally not focused on this important element of their clients’ financial lives? One reason could be that, with the Federal Reserve keeping the Federal funds rate (which influences just about all other interest rates) at or near zero for close to a decade and a half (save for a period of slightly higher rates from 2016-2019), there simply hasn’t been much extra value that advisors could provide in recommending one type of cash vehicle over another. With rates so low across the board, the extra yield that clients could achieve by choosing one savings account over another might not have seemed worth the trouble of making cash allocation a central part of ongoing planning.

Another reason could be that, with the majority of advisors being paid based on investment assets under management, those advisors aren’t being directly paid to advise on clients’ ‘held-away’ assets like cash (and even if they were, yields on cash have been so low that practically any advisory fees would have eaten up most or all of the extra value they could have provided).

Whatever the reason, whether it be advisors’ incentives based on their compensation or simply the greater economic environment, cash management – in spite of its importance to clients’ everyday lives – has traditionally played only a small part in financial advisors’ services.

Rising Interest Rates (And Cash Balances) Bring Potential Opportunities To Add Value

If the low-yield environment after 2008 made it difficult to provide value by advising clients on their cash management, more recent economic developments are beginning to change the math in the other direction. In March of 2022, the Federal Reserve started raising its key interest rate in response to the high inflation that has persisted longer than policymakers originally expected. This was after the rate had sat near 0% for almost two years since the beginning of the COVID pandemic in 2020. The Fed has signaled that it will be aggressive in continuing to raise rates for as long as high inflation persists – even at the risk of tipping the economy into a recession.

At the same time, bank account balances increased sharply during the pandemic. Government stimulus programs such as the 2020 and 2021 Economic Impact Payments, the 2021 monthly Child Tax Credit payments, and forgivable small business loans through the Paycheck Protection Program, as well as generally rising wages and salaries, led to more cash on families’ balance sheets across all income levels.

The upshot of the current environment is that, with interest rates rising for the first time in years, clients might be able to start earning non-trivial yields on their cash – and with more cash on hand in total, cash management is likely to have a greater impact on a client’s overall financial picture going forward. Furthermore, the Fed’s stated goal of continuing to raise rates at any cost to tame inflation suggests that, even if the economy slows from its current growth, interest rates might not be going back down to their previous levels anytime soon. As a result, financial advisors might be entering a period where there is an increasing opportunity to add value by advising clients on their cash.

Not All Cash Is Created Equal

The Fed’s action to raise interest rates doesn’t necessarily mean that every cash account’s yield will automatically increase in turn, as banks notoriously tend to respond to overall interest rate increases by hiking the rates they incur on borrowers for holding debt (e.g., mortgages and credit cards) much more quickly than those used to determine how much they pay to holders of savings accounts, CDs, and money market accounts. But even within that bucket of cash savings vehicles, different types of accounts will see uneven increases in their yields as rates rise overall.

As an example, consider that even as the Fed hiked its interest rates up from zero to 2.5% from March through July of 2022 (as the chart below shows), the average deposit rate on all savings accounts rose just 0.04%, from 0.06% to 0.1%, over the same time:

But within that slice of the savings pie, some types of accounts saw much larger boosts in their yields. High-yield online savings accounts more than tripled their interest rates from around 0.5% in January 2022 to over 2% in August. Though yields on cash might not beat the rate of inflation any time soon, the difference between holding cash in an ‘average’ savings account and a higher-yield account has grown substantially so far in 2022, and will continue to do so as interest rates climb further.

It’s Not All About Yield

Helping clients find the highest interest rates for their cash can itself be a valuable service for advisors to provide, but that value is greatly dependent on (and likely limited by) the prevailing interest rates. Finding the cash vehicle that best keeps up with the pace of rate changes may be a valuable service as rates continue to rise. But, in the event that rates instead reverse direction and head back downward, the benefits of yield shopping could be reduced back to a negligible amount, which could lead advisors to once again shift their focus away from cash management.

And yet, even if rates were to decline again, cash would be no less important in a client’s everyday life. Clients will still need to hold some cash regardless of the interest rate they receive on it, and the questions of how much cash to hold and where to keep it will still remain. Helping clients answer these questions has value as well, even if it is not as easily measured in basis points.

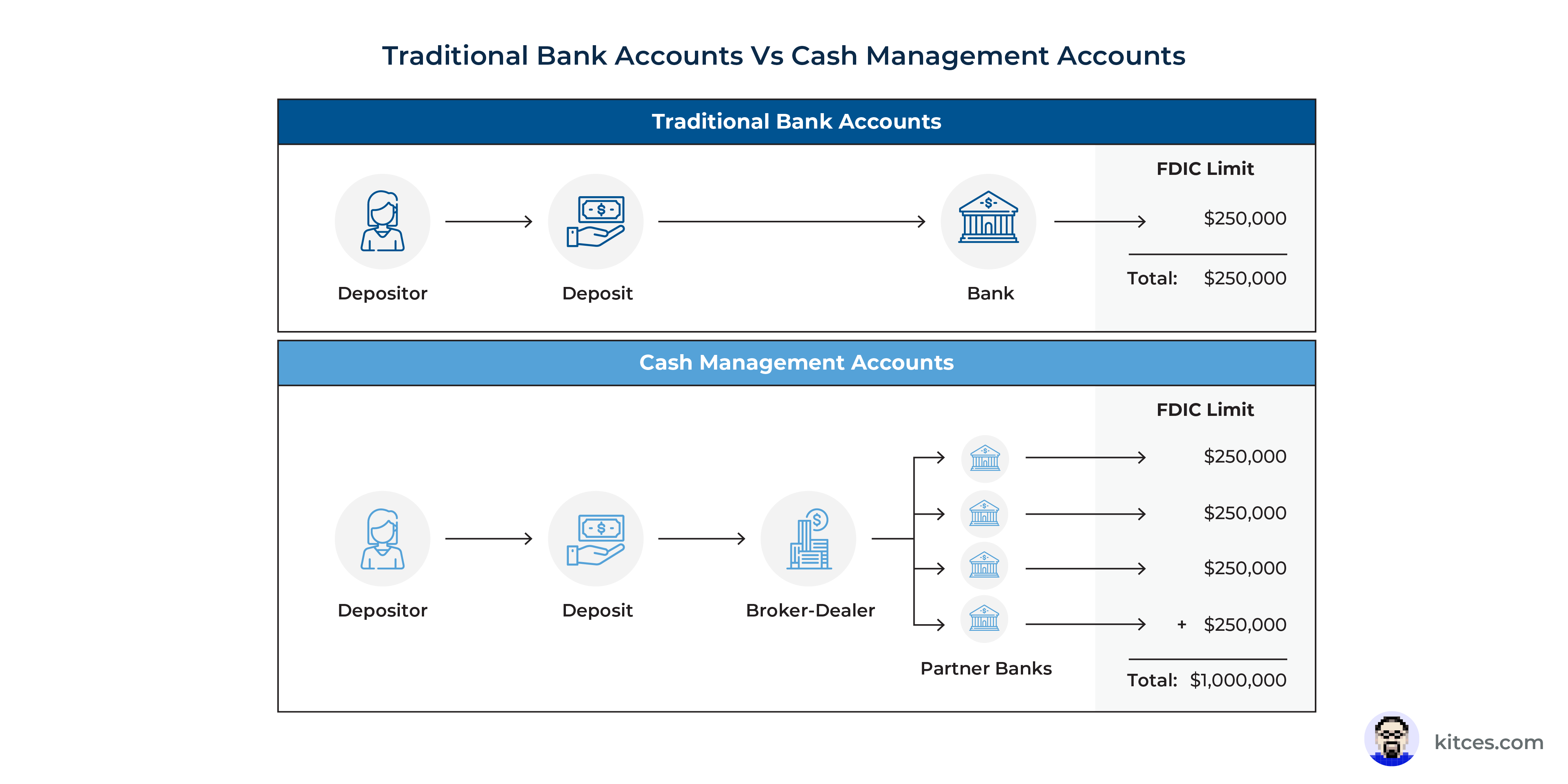

Additionally, as a client’s cash balance rises, more complications can potentially arise for them in managing their cash. FDIC insurance is limited to $250,000 per account owner at each bank, so those who want to hold more than that amount in cash (or CDs) would need to open accounts at multiple banks for their deposits to remain fully covered. If someone wanted to keep $1 million in cash, they would need accounts at four different banks; if they wanted to keep $2 million, they would need to use eight banks, and so on – and with each banking relationship comes a separate set of statements, tax forms, online login credentials, etc. The value of the client’s time saved by streamlining all of these factors could be substantial, even before accounting for the possibility of earning a higher yield on their cash.

Cash Management Accounts: The Next Wave Of Cash Management FinTech

It is likely not a coincidence that the last rising rate cycle – during which the Fed gradually rose the Federal Funds rate from 0% to 2.5% between December 2015 and December 2018 – corresponded with a rise in popularity of high-yield online savings accounts, which took advantage of the low overhead of an online-only presence to offer yields significantly higher than that of traditional brick-and-mortar banks. At the peak of the last rate cycle, these accounts yielded close to 2.5%, far outpacing most traditional savings accounts and competing with other cash-like vehicles like money market accounts and CDs.

By offering higher yields than the competition and a user-friendly, digital-first experience, high-yield savings accounts quickly became popular as a place to park short-term savings. For financial advisors, high-yield savings accounts also made the process of advising on cash much easier: rather than spending time calling brick-and-mortar banks to search for the best rate, an advisor could simply pull up a site like Bankrate and find the highest-yielding account (and they could streamline it even further by using software like MaxMyInterest to automatically find the top-yielding accounts and to propose an allocation that maximized the client’s interest rate and the FDIC coverage on their cash).

Following the rise of high-yield savings accounts and technological tools to optimize how cash is allocated between accounts, the next wave of cash management technology began to appear around the last time interest rates peaked in 2019. In this case, it wasn’t banks but investment and broker-dealer firms that led the way, offering high-yielding ‘cash management accounts’ connected to their already-popular trading apps. In 2019, robo-advisors Betterment and Wealthfront, along with the online brokerage app Robinhood, all launched their own high-yield cash management accounts, each offering interest rates competitive with the bank-owned high-yield savings accounts.

While being similar to a savings account from the customer’s perspective – often including features like debit cards, direct deposit, and bill pay features – cash management accounts really aren’t bank accounts at all; rather, they are more like the cash sweep accounts commonly used to hold cash in investment portfolios. In a nutshell, cash management accounts act as an intermediary: when the depositor moves funds into their cash management account, those funds are then sent to one or more “partner” banks. The depositor may be able to opt in or out of specific banks, but the cash management account handles allocating and moving the funds automatically. All this happens on the back end, however, so from the depositor’s perspective there is just one account to log into and move cash in and out of.

There are three additional key features that set these cash management accounts apart from both traditional sweep accounts and high-yield savings accounts:

- First, by using their existing technology infrastructure and low overhead, online brokerages are able to offer far higher yields than the cash sweep programs of traditional brokerages like Charles Schwab, TD Ameritrade, and Vanguard (similar to the way that online-only high-yield savings accounts were able to offer higher yields than traditional brick-and-mortar banks).

- Second, by partnering with multiple banks, brokerage cash management accounts are able to offer higher FDIC protection limits than traditional bank accounts. For example, Betterment and Wealthfront both provide $1 million of protection, while Robinhood offers $1.25 million (versus the $250,000 per person per account provided on traditional bank accounts).

- Finally, for existing customers on those investment and broker-dealer platforms, having a built-in cash management account offers a ‘one-stop’ experience for both banking and investing, giving customers a product from a firm they already know and trust, along with the ability to view and manage their cash and investments with a single app.

While less tangible of a benefit than higher yields and FDIC coverage, offering both banking and investing functionality in one account might be the cash management accounts’ biggest draw from a user’s perspective. In a world where apps and logins proliferate and clutter our minds (and phone screens), having a self-contained financial ‘ecosystem’ represented by a single app might become more and more attractive to users simply for the convenience of being able to find everything in one place.

Cash management accounts proved initially popular with retail customers – Wealthfront, for example, nearly doubled its total assets under management in the year it launched its cash management account – but a broader uptake may have been interrupted by unlucky timing. By the time the offerings were rolled out in 2019, the Fed had already begun cutting interest rates amid signs of weakness in the economy, and in early 2020, the COVID pandemic brought on a brief but severe recession, and interest rates crashed back down to zero. With less enthusiasm for (or value to be found in) cash management in the ensuing two years, the brokerage-affiliated cash accounts have not (yet) been accepted as enthusiastically by savers and advisors as the high-yield savings accounts that preceded them.

As rates begin to rise again, however, these accounts could begin to meaningfully compete with high-yield savings, since they are similar in terms of yield with the additional benefits of higher FDIC insurance and greater interconnectedness with customers’ existing financial ecosystem.

How Advisors (And Their Clients) Can Benefit From Cash Management Technology

High-yielding brokerage-affiliated cash management apps might be an attractive prospect for retail customers, but they pose a particular challenge for financial advisors: the highest-yielding cash management accounts are, for the most part, affiliated with retail-only investment firms that don’t have an advisor platform. Of the three outlined above, only Betterment has both a high-yielding cash account and a custodial platform for advisors. And while the broker-dealers that many advisors do use for custody – like TD Ameritrade, Charles Schwab, and Fidelity – also offer cash management accounts, those custodians pay far lower interest rates than the retail-focused firms, as seen below:

Of course, the reality is that most advisors are unlikely to recommend that a client open a cash management account at a brokerage different from where the client’s investments are being managed by the advisor, even if that account has a substantially higher yield than what is offered on the advisor’s custodial platform. And it isn’t likely that the major custodians will meaningfully increase their yields on cash any time soon, given the importance of the ‘spread’ on custodial clients’ cash as a profit center.

Until the major custodial platforms start to offer cash accounts that can compete with the retail brokers, independent advisors may not be able to offer the same kind of interconnected experience between cash and investments as a retail broker-dealer like Robinhood or robo-advisors like Wealthfront and Betterment.

Flourish Cash And StoneCastle Bring Cash Management Accounts To Advisors

Fortunately, advisors are able to use some of the same technology that brokers use to power their affiliated cash management accounts regardless of where their clients’ investments are held. Over the past few years, several third-party AdvisorTech companies have introduced cash management solutions specifically designed for financial advisors and their clients. By using some of the same back-end processes as the brokerage-affiliated cash management accounts – such as partnering with multiple banks to send depositors’ funds – these third-party companies are able to offer yields that are competitive with the retail brokers, as well as similar levels of FDIC coverage.

And with the visibility that these companies give advisors into a client’s cash, advisors can incorporate that cash more fully into their financial planning, bringing more of the client’s financial picture into their orbit. Two particular leaders in this space worth highlighting are Flourish Cash and advisor.cash by StoneCastle, which both have the potential to streamline cash management for advisors.

Both platforms offered by Flourish and StoneCastle have similar core features: Access to multiple partner banks, a single online client dashboard (which, in both cases, can be labeled with the advisor’s branding), and advisor access to clients’ account balances, transactions, and account statements (including 1099s). They also feature integrations with financial planning and portfolio reporting software (like eMoney, Orion, and Tamarac).

These features can potentially streamline the process of advising on cash quite significantly. As advisors would no longer have to search for the highest-yielding bank account to recommend to the client (and then ensure that the client actually follows up on the recommendation), they would simply send the client a link to their branded login page, where the client would be able to fill out a streamlined account application and connect their existing accounts to transfer cash in. The technology then does the work on the back end to send the client’s funds to one or more of their partner banks.

Furthermore, since Flourish and StoneCastle both partner with multiple banks– which allow the client’s funds to be shifted from one bank to another at any time – the client is ensured a competitive interest rate on their cash. As of August 2022, both Flourish and StoneCastle pay an Annual Percentage Yield (APY) of 1.75%. Both firms make money by earning a spread between the interest paid directly by the partner bank and the interest that is paid out to the client, so the client’s yield may not ultimately be quite as high as other high-yield cash management or savings accounts; however, in the mind of many clients, the ability to seamlessly integrate their cash into their advisor’s orbit might be worth the small difference in yield.

Where Flourish and StoneCastle differ is in some of the additional features they offer. One of Flourish’s key features, SmartBalance, allows clients to set a target balance for their linked checking account, which then automatically transfers money to or from their Flourish account when the checking account’s balance falls above or below that target, virtually eliminating the work of implementing an advisor’s recommendation to maintain a target checking account balance (and helping ensure that cash doesn’t build up in the client’s checking account while earning little or no interest). Flourish also has a client referral feature allowing existing clients to refer friends and family to the advisor directly through their account; advisors can also invite prospective clients to Flourish to preview the experience.

StoneCastle’s distinguishing feature is its large network of partner banks, totaling over 900 banks around the country. This allows for more stability in interest rates, as yields may not fluctuate as quickly when there are more banks to choose from, and enables them to offer a whopping $25 million in FDIC coverage per person – 10 times its closest competitor and 100 times what a single savings account would provide. For ultra-high-net-worth clients with large amounts of cash on hand, the convenience of managing that cash from a single account with full FDIC protection could be worth it on its own.

StoneCastle also features a program called Impact, which allows clients to direct their deposits specifically towards community banks and credit unions that primarily serve minorities and other underserved populations, making it a potential choice for advisors with clients for whom social impact is a strong driver of their financial decisions.

Can Advisors Bill On Cash Management?

If advising on cash adds value for clients, one inevitable question that follows is whether advisors can bill for it in some way. Because whatever method the advisor uses to advise on cash – no matter how streamlined – will inevitably require some amount of extra time, expertise, and resources to provide, it is reasonable to expect some additional compensation in return for the extra value the advisor is delivering. The question, then, is how much will it take to make it worthwhile for the advisor (without also eating too much into the value realized by the client)?

Given that most rates on cash are still between 1% and 2%, it seems unlikely that the traditional AUM structure of the 1%-ish fee used for invested assets would be practical for cash, since that would eat up at least half the yield earned on the client’s cash. Even if rates do climb further and the advisor is able to deliver that value to the client, there is no guarantee that rates would stay that high and that a 1% fee would remain practical as rates rise and fall with economic conditions. Looking at recent history, interest rates on high-yield savings accounts fell to as low as around 0.4% before 2022’s rate hikes, so it is difficult to imagine charging more than that and still being able to create positive value in all economic environments.

Whether it is worth creating a different fee structure for advising on cash may depend on the revenue opportunity that it creates. If an advisor with 100 clients, each of whom holds an average of $100,000 of cash, charges 0.4% per year to advise on that cash, they would realize 100 × $100,000 × 0.4% = $40,000 of additional revenue. Larger firms, and those whose clients have large cash holdings, could realize even more, and those with the size and technology to scale cash management could potentially charge a lower fee (which might be more palatable for clients) and still earn enough to be worth their while.

In this way of charging a small, flat cash-management fee, billing directly would be similar to an ‘Assets Under Advisement’ (AUA) model, where the advisor charges different rates for a client’s directly-managed investments and the ‘held-away’ assets that they may not manage directly, but still advise on (which traditionally comprises employer retirement plans, like 401(k) plans, but could conceivably include cash as well).

Advisors can compare the potential revenue opportunity from billing on these assets against the additional operational complexity involved. For example, advisors would need a way to aggregate asset values for quarterly billing calculations (and to separately calculate both AUA and AUM for regulatory purposes) and determine which account(s) to actually bill from. Additionally, advisors should be able to explain how additional fees for managing cash would be worth it for the client. For instance, advisors who may have previously claimed that their investment management fee covered ‘holistic’ planning, clients may have questions about why advice on cash management hadn’t fallen under that ‘holistic’ label before, and why it can’t simply be covered by the advisor’s existing AUM fee.

There is also a case to be made that offering cash advice as a ‘free’ add-on for clients will ultimately recoup its own cost to the advisor even if they don’t bill on it directly. Offering a convenient, user-friendly cash management system like Flourish or Stonecastle that is fully in the advisor’s orbit can be a differentiator from other advisors who don’t advise on cash, potentially offering an additional layer of relationship ‘stickiness’ that can keep clients around longer, and creating more opportunities for planning that help the advisor reinforce their ongoing value to the client.

It remains to be seen how far interest rates will continue to climb during the current rising rate cycle, but what seems certain is that they will fluctuate up and down as the American economy lurches out of the COVID era. The higher rates do go, the more potential yield that advisors can help their clients achieve on their cash; however, it’s important not to undersell the less-tangible (but nonetheless valuable) benefits that cash management advice can provide for both the client and the advisor.

From the client’s perspective, cash management is a potentially complex task that an advisor can help to simplify and to ensure that they receive a sufficient amount of FDIC protection. For the advisor, being more involved in the client’s cash management can help streamline and improve their recommendations in other financial planning areas (since being aware of that part of their financial picture can better inform their observations and recommendations elsewhere).

And ultimately, since most clients interact with their cash on a nearly daily basis, advising on that cash is a way for advisors to have a positive impact on their clients’ everyday life – while giving them the opportunity to remind clients of their value on an everyday basis as well!

{kind=link}