With inflation marking a 40 year high in June, everyone seems to have one question on their mind: When will inflation return to normal? July’s Consumer Price Index (CPI) print offers a glimmer of hope. Core CPI, which excludes volatile food and energy prices, grew just 0.3 percent in the month of July, down from 0.6 and 0.7 percent in the prior two months. Declining energy prices left headline CPI unchanged over the month.

Alas, the Federal Open Market Committee’s (FOMC) latest Summary of Economic Projections suggests inflation will remain high for some time. The median FOMC member is currently projecting 5.2 percent inflation in the personal consumption expenditures price index (PCEPI) for 2022; 2.6 percent inflation for 2023; 2.2 percent inflation for 2024; and 2.0 percent thereafter.

The Federal Reserve is ostensibly committed to a 2 percent average inflation target, which permits a temporarily high rate of inflation. But just because the Fed can let inflation run higher than 2 percent for a period of time doesn’t mean it should. FOMC members are asked to submit their projections under the assumption that the Fed conducts monetary policy appropriately, as they see it. Hence, their projections for inflation tell us how FOMC members think the price level should evolve.

When should inflation be higher than the Fed’s 2-percent average inflation target? In general, prices should rise above the level consistent with the Fed’s average inflation target when real output falls below its long run growth path. When supply constraints reduce our ability to produce, higher prices provide a useful signal that goods and services are relatively scarce and an incentive to scale back purchases until production recovers.

We must be careful not to confuse above-average prices with above-average inflation, however. When the economy is recovering from an adverse supply shock, for example, prices return to trend. In the process of returning to trend, prices are (1) above trend and (2) growing at a rate below the average inflation target. Hence, justifications for higher prices do not necessarily justify higher inflation. We must think carefully about where the economy is and where it is going.

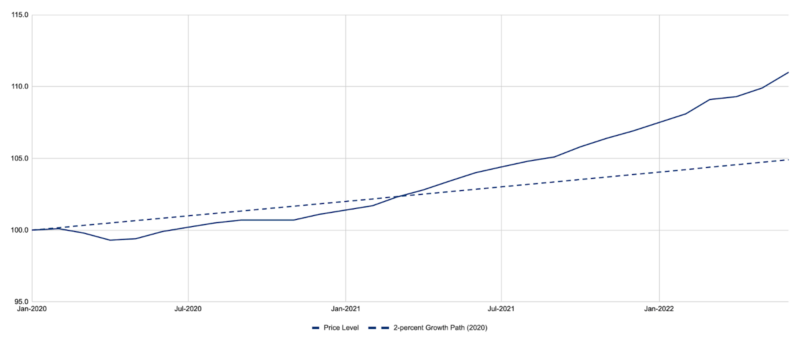

Consider how prices have evolved over the last 18 months. In April 2021, prices started to rise above trend. Then, in October 2021, they began to rise more rapidly. The continuously-compounding annual inflation rate since January 2020, which had stood at 3.0 percent in August and September 2021, climbed to 3.2, 3.4, 3.5, 3.6, and 3.7 percent in the months that followed. In March 2022, it climbed to 4.0 percent, where it remained until June 2022 when it hit 4.3 percent. Hence, the question today is whether inflation should be above 2 percent given that prices are already well-above the level consistent with the Fed’s average inflation target.

What justification might Fed officials have for wanting inflation to remain above 2 percent through 2024? Perhaps they would point to lingering supply disturbances associated with the pandemic or, more recently, Russia’s invasion of Ukraine. Alas, that would not quite cut it. To the extent that these disturbances persist, they justify above-trend prices. They do not necessarily justify above-average inflation. Above-average inflation would require a general worsening of supply conditions. And, despite the modest decline in real output observed in the first two quarters of 2022, potential output has likely continued to recover. Since prices are above trend, the process of returning to trend as real output recovers would require less than 2 percent inflation—not more than 2 percent inflation, as Fed officials project.

Perhaps Fed officials think that, although the economy will largely recover from these temporary supply disturbances, these disturbances will also bring about a longer-lasting reduction in total factor productivity growth. Below-average total factor productivity growth would result in below-average real output growth and, as such, could serve as a justification for above-average inflation.

The below-average total factor productivity growth story is sensible, but strikes me as unlikely. We do not typically assume a temporary reduction in our ability to produce has a long-lasting effect on total factor productivity growth. What is different in this situation? And why would it warrant inflation to be 20 to 60 basis points above the average inflation target given that prices are already elevated well above the level consistent with the average inflation target?

I cannot think of a good reason for inflation to remain high through 2024; but many bad reasons come to mind. The most likely explanation, in my opinion, is that Fed officials do not take their average inflation target very seriously. They permitted nominal spending to surge, which pushed prices up far higher than was required given the supply disturbances realized. They will eventually get inflation back down to 2 percent—but not anytime soon. And, even then, the price level will remain permanently elevated.

William J. Luther

William J. Luther is the Director of AIER’s Sound Money Project and an Associate Professor of Economics at Florida Atlantic University. His research focuses primarily on questions of currency acceptance. He has published articles in leading scholarly journals, including Journal of Economic Behavior & Organization, Economic Inquiry, Journal of Institutional Economics, Public Choice, and Quarterly Review of Economics and Finance. His popular writings have appeared in The Economist, Forbes, and U.S. News & World Report. His work has been featured by major media outlets, including NPR, Wall Street Journal, The Guardian, TIME Magazine, National Review, Fox Nation, and VICE News.

Luther earned his M.A. and Ph.D. in Economics at George Mason University and his B.A. in Economics at Capital University. He was an AIER Summer Fellowship Program participant in 2010 and 2011.

Selected Publications

“Cash, Crime, and Cryptocurrencies.” Co-authored with Joshua R. Hendrickson. The Quarterly Review of Economics and Finance (Forthcoming).

“Central Bank Independence and the Federal Reserve’s New Operating Regime.” Co-authored with Jerry L. Jordan. Quarterly Review of Economics and Finance (May 2022).

“The Federal Reserve’s Response to the COVID-19 Contraction: An Initial Appraisal.” Co-authored with Nicolas Cachanosky, Bryan Cutsinger, Thomas L. Hogan, and Alexander W. Salter. Southern Economic Journal (March 2021).

“Is Bitcoin Money? And What That Means.”Co-authored with Peter K. Hazlett. Quarterly Review of Economics and Finance (August 2020).

“Is Bitcoin a Decentralized Payment Mechanism?” Co-authored with Sean Stein Smith. Journal of Institutional Economics (March 2020).

“Endogenous Matching and Money with Random Consumption Preferences.” Co-authored with Thomas L. Hogan. B.E. Journal of Theoretical Economics (June 2019).

“Adaptation and Central Banking.” Co-authored with Alexander W. Salter. Public Choice (January 2019).

“Getting Off the Ground: The Case of Bitcoin.” Journal of Institutional Economics (2019).

“Banning Bitcoin.” Co-authored with Joshua R. Hendrickson. Journal of Economic Behavior & Organization (2017).

“Bitcoin and the Bailout.” Co-authored with Alexander W. Salter. Quarterly Review of Economics and Finance (2017).

“The Political Economy of Bitcoin.” Co-authored with Joshua R. Hendrickson and Thomas L. Hogan. Economic Inquiry (2016).

“Cryptocurrencies, Network Effects, and Switching Costs.” Contemporary Economic Policy (2016).

“Positively Valued Fiat Money after the Sovereign Disappears: The Case of Somalia.” Co-authored with Lawrence H. White. Review of Behavioral Economics (2016).

“The Monetary Mechanism of Stateless Somalia.” Public Choice (2015).

Books by William J. Luther

{kind=link}