Executive Summary

As an individual begins planning for retirement, one of the factors often considered is whether (and where) they might relocate to enjoy their retirement. When evaluating their potential options across the U.S., a state’s income tax rules can have a significant impact on where they might choose to live. The perception of a state as having high or low taxes could make it more or less attractive for someone choosing where to relocate, and those perceptions are often skewed by the state’s ‘headline’ tax rate (that is, the top tax rate imposed on the highest income tax bracket), meaning that states that don’t tax any income at all are often given extra consideration, while those that tax income at the highest rates tend to get crossed off the list fairly early.

In reality, however, the top marginal rates don’t usually tell the whole story – at least not for retirees. That’s because many states (including those typically labeled as “high-tax”) feature a slew of different tax breaks that can significantly reduce the tax burden for retirees in those states. As a result, the list of states where a typical (or even higher-income) retiree would pay very little or even zero tax might be much larger than what might be assumed based on the top marginal rates alone.

State tax breaks for retirees usually come in 4 flavors: no income tax at all; exclusion of Social Security income from taxable income; exclusion of pension or retirement plan withdrawals; and additional exemptions, deductions, or credits for all taxpayers above certain age thresholds. Every state in the U.S., plus the District of Columbia, features at least one of these types of tax breaks benefiting retirees, and many have more than one, meaning that retirees with a combination of Social Security, pension, and even other types of income (like dividends and interest or income from working a job) will almost always pay a lower overall tax rate on their income than those who are still working full-time.

The tricky part, however, is navigating the many nuances and exceptions included in the different tax codes of the 50 states. Many states either have income-based limitations on the tax benefits that higher-income retirees can realize, while others cap the total amount of retirement tax benefits that an individual can use (for example, by setting a maximum amount of combined Social Security and/or pension income that can be deducted from a taxpayer’s income). As part of the final decision, therefore, it’s often advantageous to do more in-depth tax planning to recognize some of the planning opportunities or pitfalls that could come with retiring to a certain state.

The key point is that even though it might not be necessary to attain a thorough grasp of all 50 states’ tax policies, knowing some of the key elements to look for when considering a given state – like whether or not (and how much) Social Security or retirement plan income is taxed; the treatment of interest, dividends, and capital gains; and what other potential deductions or exemptions might be available for taxpayers after a certain age – can create a deeper understanding of the true impact of income tax from living in a certain state. And for some future retirees, it might even expand the potential list of states beyond what they previously considered affordable!

Authors:

One of the most significant decisions that many individuals will make about retirement is where to live after they stop working. There are countless potential factors that can be considered when making this decision – like proximity to family, weather, and cultural options, just to name a few – but financial factors can also weigh heavily. The cost of living can vary widely from one area to another, which means that the location that one chooses might make the difference between a sustainable retirement scenario and one that will need some adjustments in order to succeed.

Many factors contribute to the cost of living in any given area. For example, housing, medical care, transportation, and energy costs might be among the most significant when looking at an individual city or region. But among all the location-specific factors, state income taxes might be the least understood. Retirees often seek to minimize the impact of taxes on their retirement, but the complexity of navigating income tax laws and regulations (that are unique to each individual state) makes it difficult to judge the true impact that state taxes will have on an individual’s retirement.

Though it isn’t realistic for most individuals to have a thorough grasp of all 50 states’ income tax policies, it is possible to create a reasonable estimate of the tax impact of a given retiree in various states, and namely, to understand which state(s) might be the most (or the least) tax-friendly to that retiree. By understanding broadly how states tax different types of common retirement income and knowing where to look further for specifics, individuals can gain some clarity into their state tax situation and (hopefully) turn their focus to the other factors that matter most to them.

Examining State Taxes When Choosing Where To Retire Means Focusing On More Than Just The Top Marginal Tax Rate

The state where an individual retires can have a big impact on their net retirement income and, therefore, their standard of living in retirement. Higher taxes can equate to larger withdrawals from retirement savings, presenting a higher risk that the individual will run out of savings before they retire (or, conversely, could require that they reduce spending in other ways to preserve a sustainable withdrawal rate). Thus, many individuals seek to relocate where they can expect lower state tax rates in retirement, allowing them to spend their savings in more enjoyable ways.

States are commonly classified as high- or low-tax based on their overall marginal income tax rates and (for higher-income earners) on their top marginal tax brackets in particular. By this measure, states such as California (13.3% top marginal rate), Hawaii (11%), New York (10.9%), and New Jersey (10.75%) have garnered reputations as ‘high-tax’ states.

But understanding the impact of state income taxes in retirement goes far beyond looking at the top marginal tax brackets. This is because many states have special provisions specifically designed to lower the tax burden on retirees, including tax breaks on Social Security and pension income, qualified plan withdrawals, and investment income, along with other targeted exemptions and deductions based on age and income level. As a result, while some states may indeed impose a heavy tax burden on high-income working-age individuals, those effects may be greatly reduced for retirees – such that, even in states considered ‘high-tax’ based solely on their top marginal tax rates, individuals might pay little or no tax on their income in retirement!

For financial advisors who use financial planning software applications that model state taxes in retirement projections, the challenge can be that many programs might not be able to factor in the nuances of all 50 different state tax codes, let alone keep up with every change and detail.

But advisors can still help clients navigate the tax implications of where to live in retirement, even without being experts on every single state’s tax policy. By understanding a few general rules – and knowing where to find the right information when it’s necessary to go deeper – advisors can help correct potential misperceptions that their clients may have and even expand the list of possible states where they would consider retiring (potentially opening the door to some locations that the client might not have otherwise considered possible!).

The information in this article is accurate as of September 2022. Unless 2022 tax policy is officially set in a state, the information here is based on 2021 policies.

Many Tax-Friendly Retirement States Offer Benefits For Different Types Of Retirement Income

States With No Income Tax

Just as it is easy to focus on the top marginal tax rate for ‘high-tax’ states, it is also easy to assume the list of ‘low-tax’ states begins and ends with the 8 states that have zero income tax at the state level (plus New Hampshire, which taxes only interest and dividends, but not other income like wages and retirement income), as listed below:

- No state income tax: Alaska, Florida, Nevada, South Dakota, Tennessee, Texas, Washington, Wyoming

- Only interest and dividend income is taxed: New Hampshire

Clearly, all else being equal, these 9 states are the most income-tax-friendly to all taxpayers, retirees included. But, for retirees, in particular, the list of states that offer the chance of 0% (or near-0%) state-income-tax rates may be much longer. Depending on a household’s complete retirement income picture, individuals might owe little or no state income tax even if they don’t live in one of the 9 income-tax-free states listed above.

States With Tax Exemptions For Social Security Income

Social Security is a core source of income for many retirees. And luckily (for those who receive it), Social Security income receives favorable tax treatment from the Federal government as well as from many states. At the Federal level, a maximum of 85% of Social Security benefits are included in taxable income (with that percentage dropping to 50% and 0% when income falls below certain thresholds). Furthermore, even the amounts that are Federally taxable are themselves often completely or partially exempt from state income tax.

There are 32 states and the District of Columbia that completely exclude Social Security income from their normal income taxation. Which means that, including the 9 states with no state income tax noted earlier, Social Security income is not taxed in 42 U.S. jurisdictions!

Notably, the list includes some of the states with the highest top marginal rates (like California, Hawaii, New Jersey, New York, and Oregon), meaning that despite their high-state-tax reputation, retirees in these states would pay 0% state income tax on their Social Security benefits (which, in many cases, could make up a significant portion of their overall income). And the benefits go beyond just paying zero tax on Social Security income: Because Social Security is subtracted from the taxpayer’s taxable income, that means – in states with progressively higher tax brackets as income increases – that more of the taxpayer’s other, non-Social Security income will be taxed at lower rates, further reducing the overall tax burden!

Though not included on the list above, Nebraska has passed a law that will phase out state taxation of Social Security benefits entirely by 2025.

Additionally, 8 other states – Connecticut, Kansas, Minnesota, Missouri, Nebraska, New Mexico, Rhode Island, and Vermont – allow the exclusion of at least some Social Security income in many cases. For some households, these exclusions can be total.

The states that partially exclude Social Security benefits from taxation have different methods of calculating the portion that is excluded, so the total value to retirees can vary significantly by state. For example, Connecticut excludes Social Security income in full if the filer’s Federal Adjusted Gross Income is below $75,000 for single filers ($100,000 for joint filers), while Minnesota has a lower threshold ($64,670 for single filers, $82,770 for joint). New Mexico’s newly passed exemption, which is slated to start for the 2022 tax year, will also have income-based phaseouts of $100,000 for single filers and $150,000 for joint filers.

Adding the states above with full or partial exemptions of Social Security to the 9 that have no tax at all, a total of 48 states (plus the District of Columbia) fully or partially exclude Social Security income from taxation. Only Montana and Utah fail to offer any targeted relief to taxation of Social Security benefits!

States That Exclude Income From Pensions And Retirement Plans

Many retirees – particularly those who are clients of financial advisors – rely not just on Social Security for retirement income but also on coordinated withdrawals from their retirement savings (or, in increasingly rare circumstances, on guaranteed benefits from defined-benefit pension plans). And while this income is almost always taxable at the Federal level (save for Roth account withdrawals and after-tax portions of traditional accounts), many states exclude some – or even all – pension and retirement plan income if certain conditions are met.

There are 3 states – Mississippi, Illinois, and Pennsylvania – that exclude all pension and qualified retirement plan income from taxation (at least in most cases – Mississippi’s exclusion applies only to income for taxpayers over age 59 ½, which is the same age when most taxpayers can take retirement plan distributions without a Federal tax penalty on early withdrawals). Notably, these 3 states are also on the above list of states that do not tax Social Security. Which means that, for retirees whose income consists solely of Social Security benefits and withdrawals from retirement accounts, these 3 states, plus the 9 states with 0% income tax, would not tax their income at all!

But for retirees who don’t plan on retiring in any one of these 12 states, there are many other states offering additional exclusions of retirement income from pensions and other qualified plans, which could significantly reduce (or eliminate entirely) their taxable income. Specifically, 21 states offer limited exclusions of certain types of retirement income, some of which are subject to limitations such as income-based phaseouts, age-based restrictions, or reductions based on the amount of Social Security that is also excluded from income. The particulars of these rules can be complex and are specific to each state, but they are summarized at a high level in the map and table below.

In some cases, these retirement income exclusions are quite broad and can apply to sources of income beyond ‘regular’ retirement accounts, such as rental income and investment income from non-retirement accounts (Delaware and Georgia), and even earned income (Georgia, up to $4,000/person).

In other cases, exclusions could be narrower. For example, in Rhode Island and Maryland, the pension exclusion applies to withdrawals from 401(k), 403(b), and 457(b) plans, but not to distributions from IRAs. This limitation makes SIMPLE and SEP IRAs, as well as IRA rollovers, less attractive for those who plan to retire in those states (and incentivizes those with both IRA and 401(k) plan assets to roll their IRA funds into their 401(k) plan when possible in order for their withdrawals to fully qualify for the exclusion).

Example 1a: Martha is a retiree in Rhode Island. After retirement, Martha had $500,000 in her former employer’s pretax 401(k) plan, which she subsequently rolled over into a traditional IRA.

She begins making withdrawals of $15,000 per year, but because those withdrawals are from her IRA, they are treated as taxable income for state tax purposes.

Example 1b: George is a retiree in Rhode Island. After retirement, George has $250,000 in his former employer’s pretax 401(k) plan and $250,000 in a traditional IRA. After confirming that his 401(k) plan will accept a rollover from his IRA, George rolls the IRA’s assets into his 401(k) plan.

Like Martha in Example 1a, George also begins making withdrawals of $15,000 per year. But because those withdrawals are from a 401(k) plan and not from an IRA, they qualify for the $15,000 per year exclusion.

Because George is below the income phaseouts for the Rhode Island pension income exclusion, 100% of his pension income will be tax-free for state tax purposes.

Some states, including Colorado, Maine, and Maryland, reduce their pension and retirement plan exclusions by the amount of Social Security benefits that are also excluded from income, meaning that retirees who are already receiving Social Security may receive a reduced exclusion (or possibly no exclusion at all!) for their pension income.

This creates tax-planning opportunities for retirees in these states; as while pension income received before the retiree starts receiving Social Security benefits is more likely to fully qualify for the exemption than after they receive benefits, these states might be particularly attractive for retirees who plan to receive Social Security benefits only after they begin receiving retirement income (that would be subject to income exclusion).

During the window of time between when retirement/pension distributions and Social Security benefits begin, the retiree may be able to receive (at least up to the maximum excludable amount) pension/retirement distributions free from state income taxes, without the exclusion being reduced by Social Security benefits. This factor also makes delaying Social Security benefits potentially more attractive in these states.

Example 2: John and Abigail are 65-year-old retirees considering where to live in retirement. They currently live in Southern California, but because they both love to ski, they want to find a place to retire where they can enjoy the slopes.

Each has an IRA worth $750,000. John and Abigail are planning to delay filing for Social Security benefits until age 70 and make withdrawals from their retirement accounts to fund their living expenses in the meantime.

The couple’s financial advisor points out that Colorado not only has some of the best ski resorts but also allows for an exclusion of up to $24,000 per person in pension income each year for individuals age 65 and older, for a combined total of $48,000 per year free from state tax every year for 5 years (until they both reach age 70 when their Social Security benefits would begin).

Which means that relocating to Colorado would permit them to receive up to a grand total of $48,000 × 5 years = $240,000 in state-tax-free income before they begin receiving Social Security benefits (and even before considering any other state tax exemptions, deductions, or credits)!

Once John and Abigail file for Social Security benefits, however, the exemption for pension income will be reduced by the amount of benefits received (and eliminated entirely if their Social Security benefits exceed the $24,000 per person exclusion maximum). So the window of opportunity to maximize their income exclusion ends once they decide to start receiving Social Security benefits.

Some states also exclude from taxation all or some income from certain types of public pensions (such as military, police, firefighter, teacher, or other Federal, state, or local government pensions). For example, 24 states have personal income tax but do not tax military pension income at all. Other states allow for partial exclusions (such as Oklahoma, which allows for an exclusion of 75% of military pension income).

In some cases, military pension exclusions can reduce other pension exclusions. For example, in South Carolina, excluded military pension income reduces the $10,000 retirement income exclusion dollar for dollar, making the retirement income exclusion less valuable for retirees who rely on both military pensions and other types of retirement income.

If public pensions make up a large part of a household’s retirement income, state taxes can be greatly affected by a taxpayer’s state of residence (e.g., some states may only exclude state employee pension income if the retiree was an employee of that state) and taking a careful look at a state’s tax policies may be worth the effort to fully understand the tax implications.

The Most Retiree-Friendly States

Putting all of these considerations together, each of the U.S. states can be categorized into one of 4 groups based on their tax-friendliness with respect to income tax, Social Security benefits, and pension/retirement plan income, as shown in the graphic below:

- Zero income tax (8 states plus New Hampshire, which only taxes certain investment income);

- All Social Security and pension/retirement plan income exempted from taxation (3 states);

- Social Security exempted, but pension/retirement plan income at least partially taxed (29 states plus the District of Columbia); and

- At least some tax on both Social Security and pension/retirement plan income for most retirees, though exactly how much tax they will pay on each may vary greatly from state to state (8 states).

Age-Based Exemptions, Deductions, And Credits

Beyond tax breaks specifically tied to Social Security, pensions, and qualified retirement plans, some states offer additional tax benefits for people age 65 or older. There are 29 states (plus the District of Columbia) that offer age-based benefits intended to create tax relief for retirees, but unlike the Social Security and pension/qualified-plan exclusions discussed earlier, these age-based exclusions apply to any type of income, including wages and investment income.

In many cases, states offer a higher standard deduction to residents over a certain age. But depending on the state, these relief measures may also be structured as separate exemptions or deductions (which reduce the amount of income subject to taxation) or as credits (which reduce the amount of tax owed dollar for dollar).

States who use separate deductions and credits rather than an increased standard deduction may offer greater benefits to taxpayers who itemize their deductions, and for whom a higher standard deduction wouldn’t provide any benefit.

Note that, in many cases, these exemptions, deductions, and credits are in addition to other tax benefits (e.g., standard deductions and personal exemptions) that apply to all taxpayers. In effect, this can create a 0% state tax bracket that potentially gives retirees the ability to receive a certain amount of income from sources such as dividends, interest on investments, or income from a part-time job (and often in addition to Social Security and retirement withdrawals), without paying state income tax.

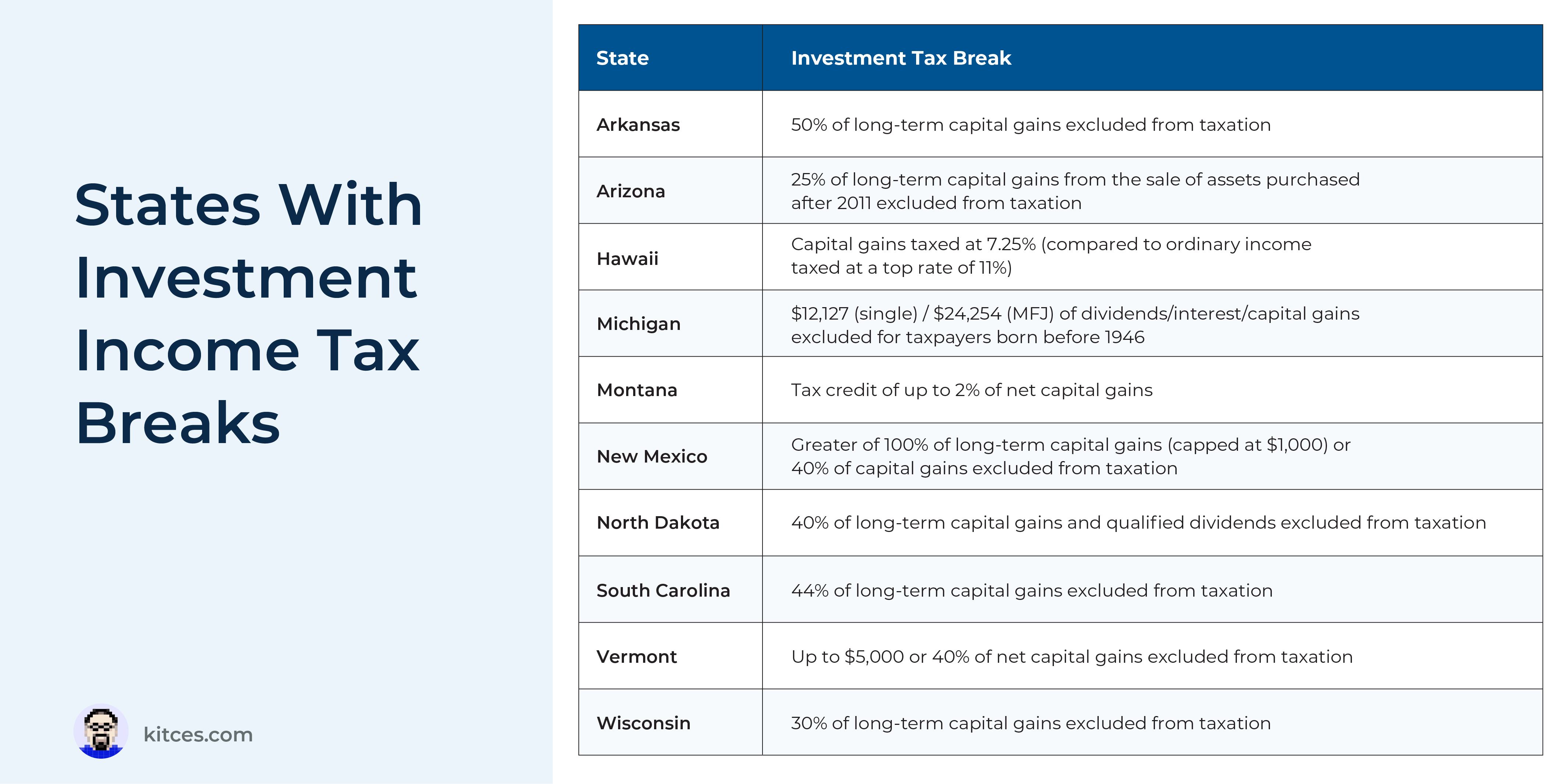

States With Special Treatment Of Investment Income

Investments in taxable accounts can be another important component of many retirees’ income. While the benefits for investment income tend to be less generous than for other types of retirement income, 10 states do offer lower taxation of certain types of investment income, which, while not specifically targeted at retirees, can help reduce taxes for those who rely on interest, dividends, and capital gains in taxable investment accounts.

Conversely, as noted above, New Hampshire is unique among states in that it taxes only investment income (though only from dividends and interest, not from capital gains), making it currently among the less tax-friendly states for retirees who rely largely on income from taxable investments. However, recently-enacted legislation will phase out their current 5% tax on dividends and interest, eliminating it entirely (thus making New Hampshire fully income tax-free) starting in 2027.

Retirement Income Exclusions Based On Per-Person Spousal Income

The 16 states in the table below offer retirement income exemptions on a per-spouse basis, not as a combined exemption for the household. Which means that, in order to access up to double the per-person exclusion, each spouse needs to have their own retirement income.

Example 3a: Jimmy and Rosalynn are married and are both 95 years old. They live in Georgia, where taxpayers age 62 and older can each exclude up to $65,000 of their own retirement income for a combined maximum of $130,000.

Jimmy and Rosalynn have a combined income of $145,000, which is roughly split between them. Since they each receive income in excess of the per-person maximum exclusion permitted in Georgia, they are entitled to take the full combined exclusion of $130,000, with a taxable state income of $15,000.

Example 3b: Amy, Jimmy and Rosalynn’s daughter, is married to James. Amy and James are both 65 years old and also live in Georgia, so they, too, can also exclude up to $65,000 of their own retirement income.

Amy and James also have a combined income of $145,000, but since Amy earns the lion’s share of the family’s income and James earns only $5,000, which is less than the maximum retirement income exclusion amount allowed by their state, they cannot take the full combined exclusion. They are only entitled to exclude $70,000 of their income, with a taxable state income of $80,000.

In states where retirement income exemptions are applied to each spouse individually, couples who qualify for the exemption and whose retirement incomes are more evenly distributed between spouses will generally end up with a lower state income tax bill than couples whose retirement incomes are mostly attributable to one spouse. This means that, all else being equal, retired couples in these states can benefit from planning their withdrawals so that each spouse fills up their ‘exclusion bucket’ before taking additional retirement withdrawals.

This income splitting is easiest to do if both spouses have assets in retirement plans. Unfortunately, by the time a couple reaches retirement, it may be too late to set the family up for a better state tax situation. So, planning to optimize for state taxes often needs to begin early, with total annual contributions split between spouses rather than concentrated with one spouse.

Tax-Friendly States Can Vary For Different Retirees Depending On Retirement Income Sources

Because of all the different ways that states impose taxes on different types of income, some retirees could have many more options for paying zero (or close to zero) tax than others, depending on the type of income mix they receive during retirement.

For example, given that nearly all states exempt some (or all) Social Security income from taxation, and that many states also exempt at least a portion of the income from pensions and qualified account withdrawals, retirees who rely primarily on those 2 sources of income will have a large number of states to choose from where their tax burden will be minimal. By using financial planning software with the capability to model state taxes, financial advisors can get an idea of which options these retirees would have to choose from.

Example 4: James and Dolly Madison anticipate that they will each receive $18,000 of Social Security income and $19,500 of qualified-plan income during retirement, for a combined total income of $75,000 each year.

With their retirement income mix, the Madisons would have an estimated $0 state tax bill in 24 states! Notably, this list includes Illinois, New Jersey, and New York, states commonly thought of as high-tax states.

Furthermore, if the Madisons were willing to pay slightly more than $0 in state tax – but a less than 1% effective state tax rate overall – the list would expand by 11. Their effective state tax rates would be over 2% in only 3 states: Oregon (2.2%), Massachusetts (2.2%), and Utah (3.6%)!

As illustrated above, taxpayers with moderate income levels sourced primarily from Social Security and qualified retirement plans will generally have very favorable state tax conditions across the country. But because many states have limitations on the amount of retirement income that they will exempt from tax – or have phaseouts that reduce the tax-preferenced treatment of retirement income above certain income levels – the number of low-tax states starts to dwindle as income increases. And yet, a retiree with substantial income could still pay zero or near-zero tax in a number of states – even those that aren’t known as ‘zero-tax’ states.

Example 6: Ulysses and Julia Grant are soon-to-retire attorneys. They anticipate that they will each receive $48,000 of Social Security income, close to the maximum possible amount. They also have large retirement plan balances, and each anticipates receiving $77,000 of qualified plan income each year to fund the rest of their spending during retirement. Thus, they expect their combined total annual income to be $250,000.

While the Grants’ high income led them to expect substantial tax bills in most states, they still found that there were 12 states – the 9 zero-tax states plus Illinois, Mississippi, and Pennsylvania – where they would owe no state income tax on account of their mix of Social Security and qualified retirement plan income. A 13th state, Georgia, almost squeaked into this group as well, with a 0.1% effective rate, and 6 additional states would have an effective rate of under 2%.

Tax-Friendly States For Earned Income And Investment Income In Retirement

While some retirees may plan to rely solely on Social Security and qualified plan withdrawals in retirement, other retirees may need to rely on additional sources of income. Earned income (e.g., income received from working in a job or business) and investment income (e.g., interest, dividends, and capital gains from a taxable investment portfolio) are important parts of many retirees’ income mix. Because these types of income don’t have the same favorable tax treatment in most states, retirees who rely on them are likely to see higher taxes in many states than those whose income solely comes from Social Security and retirement plan withdrawals.

In the case of individuals with earned income in retirement, recall that only Georgia specifically allows a deduction for earned income (up to $4,000) after age 62. And although other states offer age-based deductions and credits that can offset all types of income – allowing at least some relief to individuals who make income from working a job or running a business in retirement – those offsets tend to be smaller than those for Social Security and retirement income.

Still, when earned income is part of a mix that also includes more favorably-taxed income like Social Security and qualified plan withdrawals, the overall effect the earned income has on the individual’s tax burden can be fairly modest in many states. Since most states have progressively tiered tax brackets (similar to Federal tax brackets), retirees with a low or moderate amount of earned income – along with Social Security and retirement plan withdrawals, which may only be partially taxed, if at all – will have most of that income taxed at relatively low rates.

Example 7: The Tafts are a couple, both age 70, with $90,000 in annual income as outlined below:

Despite their earned income, which makes up more than a quarter of their total income, the Tafts can still take advantage of the exclusion of their Social Security and pension/qualified plan income in many states, plus additional age-based deductions, exemptions, and credits, that would make their taxable income substantially less than their gross income of $90,000.

As a result, they would still have 21 states to choose from with 0% income tax, and 35 states with estimated effective tax rates below 1%.

Many households may also have a substantial amount of taxable investment income to fund their retirement and, for some – e.g., business owners who sold their businesses at retirement – income from interest, dividends, and capital gains can make up a large part of their total income.

Unlike the Federal tax system, few states have separate tax rates for capital gains income. This is part of the reason that tax rates are generally higher when investment income makes up a substantial portion of a taxpayer’s total income. Since investment income is not treated as favorably as Social Security, pension distributions, or qualified retirement plan income in many states, it is more often taxed in the same way that earned income would be, potentially bumping taxpayers into progressively higher tax brackets.

Example 8: The Trumans are a recently retired couple deciding where to live in retirement using their $48,000 combined annual Social Security income, $24,000 in withdrawals from retirement accounts, and funds from a $2.3 million taxable account from which they draw $78,000 of investment income (LTCG) each year.

Because of the Trumans’ investment income and higher total income, the number of states with no tax is much smaller than for the Tafts from Example 7. There are only 10 states with 0% tax and 21 states with effective state income tax rates of 3% or more.

Putting State Income Tax Planning Into Practice For Financial Planning Clients

The tax burden in any given state will depend on a family’s total tax picture. But the examples above show that some states known for their high top-marginal rates can, in spite of their reputation, actually be quite tax-friendly to retirees. Some states, like Georgia, Illinois, Mississippi, New Jersey, and Pennsylvania, are often effectively zero-tax states for some retirees. In many other states, state taxes might amount to only 1% or less of the total income earned.

Typically, the more a household depends on Social Security and qualified retirement plans and pensions, the higher the likelihood that they will pay little or no state income tax. Yet the list of states that partially or fully exclude these types of income is much larger than many clients might imagine – and by helping clients put this in perspective, advisors can potentially broaden their range of possible retirement locations.

If a retiree is looking to minimize their state tax burden in retirement, then they might have more options than just the 9 states with no income tax. This is because, depending on their mix of income from Social Security, retirement plans and pension distributions, taxable investment income, and earned income, the list of potential states with little or no tax that would apply could include numerous other states, including ones with a high-tax reputation.

A Process For Financial Advisors To Compare State Income Tax Options For Retiring Clients

When discussing with clients how their choice of where to live in retirement will impact their tax situation, advisors can look beyond just the headline marginal tax rate. To get a deeper understanding of the tax implications, advisors can consider the specific types of income that the client will rely on in retirement and how it will be taxed in the state(s) that the client is contemplating. By doing so, it becomes clear that certain states might be better from a tax perspective than others for some clients (while other states might be preferable for other clients with different income sources).

The process can start by making a list of each of the different types of income the client will rely on in retirement, broken down by the individual recipient (as some states offer benefits that are broken down by each income earner). In addition to the traditional mix of income sources that include Social Security, qualified retirement plans, pension income, and taxable investment accounts, some clients might have plans to work part-time in retirement or even start a side business in their post-employee lives. All of these types of income may be taxed in different ways at the state level, depending on the state, so fully understanding the client’s potential tax situation requires first knowing what role each type of income will play in the client’s retirement plan.

After determining the client’s sources of retirement income, the next step is comparing how those sources of income will be taxed in the state(s) the client is considering. Some financial planning software platforms include state taxes in their projections, so it may be tempting to rely on the software’s outputs when comparing different states. However, software programs may not fully account for how different states tax different types of income – nor will they always be updated immediately to account for changes in state tax policy. Which means that it would be best to check the software’s output against the state’s actual tax policy for accuracy.

Of course, the total cost of living in a certain location, including expenses for property taxes, housing, healthcare, entertainment, food, and transportation, could reduce or even fully negate the tax savings from moving to a state with lower income tax rates.

Financial advisors can help their clients consider these factors in aggregate to make the decision on which state or area can maximize the client’s chances of a financially successful retirement.

State Tax Summary

Below is a summary table of each state’s tax treatment of Social Security, pension and retirement plan income, investment income, and age-based deductions and exemptions.

Click to download the editable Excel spreadsheet

Ultimately, deciding where to live in retirement is about deciding where an individual will be happiest once they begin that phase of life. Financial considerations like taxes may not (and perhaps should not) always be the deciding factor, but knowing that one’s savings will be spent on more of what they want to spend it on (and not on taxes) can make it easier to choose a place to live based on what really matters, with fewer financial constraints to limit a person’s available options.

For advisors, then, a deeper knowledge of state tax rules, including which states do or do not tax major sources of retirement income like Social Security and pension and qualified plan withdrawals, can help open up more possibilities for clients to make the decision that will make them happiest in the long run.

{kind=link}