Executive Summary

Communicating ongoing value to clients and prospects can be a challenge for financial advisors. Although there are many ways to articulate how an advisor can create value for a client, there is no guarantee that any one particular method will resonate with every potential client. An expression of value that works for one prospect might fall completely flat with another – and for advisors, it might feel like guesswork to find out what message will be the most effective for a particular client.

In this guest post, Michael Lecours, financial advisor and co-founder of fpPathfinder, introduces an approach for advisors to define their value for clients based on the “Jobs To Be Done” framework – that is, the specific outcome that the prospect wants from engaging with an advisor.

The concept behind the Jobs To Be Done framework lies in the insight that prospective clients often want something specifically unique beyond just the service provided by the advisor. For example, one client hiring an advisor to manage their investments might actually be seeking more free time from not having to manage their own portfolio, whereas another client might seek the advisor’s help because they want to reduce their stress level and fear making the wrong investment decisions. While the actual service performed by the advisor might be the same for both clients, the different ‘jobs’ of getting more free time and reducing stress levels reflect unique aspects of the advisor’s value that are most important to each client. While there are countless potential reasons that a client would seek an advisor, the Jobs To Be Done that clients generally need can be grouped into four categories: Functional (relating to the advisor’s knowledge and technical skills); Emotional (relating to the peace of mind created by professional advice); Social (relating to the ability to keep up or fit in with friends and peers); and Aspirational (related to achieving a certain future goal or status).

For advisors to convey their value in terms of a client’s Jobs To Be Done, they must first identify what those jobs are. One way to do this is to use a job-mapping approach to help identify where in the financial planning process the client or prospect became stuck, and what triggered their search for help. For instance, do they need help defining their big-picture goals? Are they too disorganized to put together the necessary documents for creating a plan? Or do they know what they need to do but want help executing their plan? Assessing the client’s challenges in each job-mapping stage – from Pre-Execution, Execution, and Post-Execution – can help the advisor determine the actual job that will help the client overcome the obstacle blocking them from finishing the process.

Ultimately, the key point is that advisors can convey their value to clients in terms of what clients really want from the relationship. And by assessing the different reasons that clients may be unable or unwilling to do their own financial planning and finding out where in the process the client may be stuck, advisors may find valuable insights into the actual job a client needs to be done. And when advisors understand the real Jobs To Be Done that clients are seeking, they can create a compelling value proposition based on what will help them complete those jobs!

The Challenge Of Communicating Value Faced By Financial Advisors

For many financial advisors building financial planning firms, success can be described by the ‘Iceberg Illusion’, which depicts a giant iceberg with only about 20% of the entire iceberg visible above the water. This visible portion represents the aspect of being a financial advisor that other people can externally actually see – the client service aspects and marketing/communication efforts – but the remaining 80% is unseen below the waterline, representing the bulk of time advisors spend working on goals and projects that the client may never see, such as their efforts to prepare for client meetings, keep the business running, and research the planning industry to stay on top of current trends.

In other words, while the client may see the streamlined report that clearly communicates their unique situation along with the advisor’s recommendation, they never see all the work that the advisor put into reviewing the client’s history, researching options, and formulating the recommendation. Consequently, clients are often accustomed to seeing only the ‘end-product’ without recognizing the hard work, time, and expertise of advisors who truly provide great service.

Importantly, for many advisors, articulating the value that they can provide to a prospective client can be a tough challenge. In fact, the challenge of communicating value is common for any service-based business that provides intangible services. Clients don’t see or touch the financial planning process involved in producing the plan they may be presented with, and therefore it’s hard for them to evaluate the value they would receive if they engaged with the advisor. However, there are various strategies that advisors can use to communicate the value of their service to prospective clients.

Communicating Advisor Value As Return On Investment

One way that advisors can articulate the value of financial planning is to approximate the additional return on investment that comes from engaging in financial planning. In essence, the advisor attempts to boil all the value provided to the client down to a simple “excess” rate of return. Vanguard’s Advisor Alpha, Morningstar’s Gamma, and Envestnet’s Capital Sigma are some of the more commonly referenced reports that aim to calculate the value financial planners provide to their clients as a function of their return on investment.

For instance, Vanguard’s February 2019 report, Putting Value On Your Value: Quantifying Vanguard Advisor Alpha, suggests that by incorporating certain best-practice advisor strategies (e.g., using particular spending/distribution strategies, behavioral coaching, and regular rebalancing), advisors can potentially add about 3% in net returns per year.

This framework provides an easy and relatable way for an advisor to communicate their value that can resonate with the client. It naturally adds a layer to the investment performance conversation that shifts the focus to the benefits of financial planning while still looking through the lens of Return on Investment.

For some clients who appreciate detailed conversations about their investment strategy, this communication method may resonate with them. For others, though, the purpose of financial planning isn’t necessarily about wealth creation or enhancing returns in the first place… so they may not care at all.

Communicating Advisor Value As It Relates To What Is (Specifically) Important To Clients

Some advisors structure their conversations by leaning into attributes that clients find important to them. The Financial Planning Association’s study “Identifying What Investors Value in a Financial Adviser: Uncovering Opportunities and Pitfalls” by Ryan O. Murphy, Samantha Lamas, and Ray Sin, found that clients ranked the following attributes most valuable (from highest to lowest) in what they get from the advisor-client relationship. Interestingly, this study also identified that many of the factors that advisors believe clients value most did not align with what clients actually value:

According to this study, advisors can use several different angles to communicate their value based on what clients value most, or alternatively, to focus on clients who particularly appreciate a certain type of advisor value. For example, some advisors may choose to connect with clients who value the advisor’s ability to help them reach their goals along with their skills and knowledge. These advisors might frame their value proposition by emphasizing their expertise (e.g., “I bring 25 years of experience in helping clients attain their financial planning goals”). Other advisors may focus on targeting clients who value their ability to communicate clearly and then attract them by writing newsletters and blog posts that explain complex financial concepts well.

While this study revealed a notable mismatch between advisor and client perspectives on what clients value most, another research study by the same authors, “Goals-Based Financial Planning: How Simple Lists Can Overcome Cognitive Blind Spots”, suggested that advisors can overcome this disconnect by helping clients identify their most important goals (which tend to change often over time) with simple tools like checklists. And by doing so, advisors can focus on communicating what clients really do value most – reaching the specific goals they want to achieve. Which is important, because shifting their focus on communicating what really matters most to clients can help advisors appeal more broadly to investors.

And specificity is important, too, because when messages that are meant to resonate with clients and prospects are too generic (e.g., “We can help you reach your financial goals”), they tend to lack substance and nuance that show how the advisor will actually help them address the concerns that keep them up at night. This can be compounded by the fact that each client is unique, with different goals and different needs. Because, in some cases, prospective clients may not even be thinking in terms of goals; instead, many come to an advisor with a specific pain point in their financial life where their goal is to address the pain. And a prospective client evaluating the websites of two advisors will be more likely to gravitate toward the one that specifically addresses their particular pain point rather than toward the one that only talks broadly about “reaching your financial goals”.

One strategy for advisors who want to frame their value proposition around helping clients achieve their goals without losing the specificity of what that will mean for the client is to focus on helping clients who have similar goals. For example, an advisor could communicate, “We help clients looking to retire before age 60”, or “We help clients looking to retire within five years”, both of which will speak more to a prospective client than simply “We can help you reach your financial goals.”

Communicating Advisor Value As A Process

In addition to communicating value as a return on investment and how the advisor will address their clients’ priorities, some advisors also communicate their value based on their process. These advisors try to give insight into what occurs behind the scenes (or ‘below the waterline’, building on the hard work hidden in the iceberg illusion noted earlier). There are a few different ways that some advisors use this strategy today.

Strategic Coach’s Dan Sullivan developed a framework called a Unique Process for entrepreneurs to help them lay out general tenets of thinking through their own processes to deliver what they’re most talented and passionate about to clients in a systematic way. His book, Unique Process Advisors, showcases several examples of financial advisors who have used this approach to outline specific steps that occur when delivering their services to clients. It makes what to expect during the planning engagement very clear to the client.

In one example from the book, Mary Anne Ehlert, President & Founder of Protected Tomorrows, described how she and her team developed a unique process for parents of children with special needs. This 8-stage process, which she refers to as the Online Future Care Planning System, gives a new client a good sense of what it would be like to work with Mary Anne and her team. They know what they can expect throughout the planning engagement because the documented process succinctly captures and showcases the different areas that will be covered.

Asset Map has elaborated on Dan Sullivan’s Unique Process with their own framework to inspire advisors looking to articulate the process they use in their client journeys. Their Financial Advice Journey outlines 10 steps, summarized into 5 phases (illustrated below), that an advisor can use to help prospective clients understand what to expect at each stage of the financial planning process.

Another way for advisors to communicate the value of their services as a process is to create an annual client service calendar. In a 2014 ThinkAdvisor article, Angie Herbers lays out how advisors can set up a monthly service calendar, including a comprehensive menu of tasks. Some of the tasks are client-facing, like “Quarterly Newsletter”, while others are behind the scenes, like “Internal Investment Committee Meeting”.

Sharing such a calendar with clients helps them understand what their advisor actually does for them every month of the year, even when there is no direct contact between the client and the advisor.

With all of the various communication methods available to advisors, it can be hard to pick just one strategy to use. Each one is distinct and compelling; some of these strategies may resonate with certain clients and prospects but completely miss the point with others. A busy, single parent with young children may not care much about the process but may be very interested in how little time will be needed on their part and how much the advisor will do to help them achieve their goals. On the other hand, an engineering professional may gravitate more toward understanding the processes involved and the value communicated in terms of return on investment.

While advisors can combine elements from several different strategies in an effort to maximize the number of chords they strike when communicating with clients, it can be helpful for them to first understand the underlying theme that makes these different communication strategies work so well. This theme is described by the Jobs To Be Done framework.

Introducing The Jobs To Be Done Framework

“People don’t want to buy a quarter-inch drill. They want a quarter-inch hole!”

—Theodore Levitt, Harvard Business School professor of Marketing

The Jobs To Be Done framework, developed by Harvard Business School professor Clay Christensen, proposes that consumers hire businesses or make purchases based on specific jobs they want help getting done.

In originating his framework, Christensen described an interesting example where he and his colleagues assessed the particular job that consumers wanted a McDonald’s milkshake to complete. After lots of interviews, they determined that consumers didn’t buy the milkshake for its taste or sweetness or because of their desire for a morning snack; they were ‘hiring’ the milkshake to distract them from their long, boring morning commute to work. Consumers needed their milkshakes to keep them engaged with life in some manner while they were stuck in traffic on their way to work, which made the thick McDonald’s milkshakes – which take a long time to slowly drink down – an especially good fit for the Job.

Similarly, for a prospect using the Jobs To Be Done framework to hire an accountant to do their taxes, the specific job they really want to be done might be either:

- To provide confidence that the taxes are done correctly; or

- To save time by having someone else do their taxes for them.

In both cases, the work actually provided by the accountant might be the same, but the job – as the client sees it – can be framed very differently. In one case, the prospect wants to buy confidence that taxes are prepared correctly based on the accountant’s experience and expertise, and in the other, the prospect wants to buy time saved from preparing their taxes by delegating to someone else that does it for them. In both cases, they are looking for help with a job that goes beyond just tax preparation services. And understanding the actual job that a client wants to have done for them can help the professional market their services to their target clients much more effectively.

Generally, Jobs To Be Done can fall into four categories:

- Functional: Represents a goal or task the client is trying to achieve, such as having their investments managed or their income taxes filed.

- Emotional: Represents the emotions or feelings the client wants to experience, such as reduced stress from watching investments, greater confidence in knowing what to do, etc.

- Social: Represents how clients want to be viewed or relate to others, such as organizing retirement goals or travel plans to spend more time with friends and family members.

- Aspirational: Represents how clients can fulfill certain ambitions, such as having the means to live their lives to the fullest or being financially secure and successful.

As another example, consider a person who suffers from dental anxiety so severe that the distress of their anxiety outweighs the benefits they receive from regular dentist visits. In this case, a dentist who communicates by focusing on the cost or quality of the dentistry services will not connect with such prospects. However, some dentists have developed their businesses specifically to cater to these patients, such as Dentists for Cowards, who employ special techniques to ease patient anxiety. And fearful patients hire these dentists not so much to clean their teeth (a functional job), or to help them feel more confident about their smile (a social job), or to make them healthier (an aspirational job); rather, the patient hires the dentist primarily to reduce their anxiety (an emotional job)!

The important consideration here is that a financial planning engagement could take the form of many different jobs depending on the client’s perspective. A client could hire an advisor to create a financial plan for any of the job types:

- Functional: the client doesn’t have the time or technical expertise to do it themselves;

- Emotional: the client wants the peace of mind that their plan will be done correctly (by an experienced professional);

- Social: the client might want to retire because they want to spend more time traveling with their friends who have also just retired; or

- Aspirational: the client wants to achieve better financial outcomes to be more financially secure in retirement or achieve a certain lifestyle.

In all of these cases, the service of creating a financial plan is the same, and the time and expertise it takes may be the same, but the job that the client needs help with is actually motivated by very different reasons.

There are lots of different jobs that a prospective client could hire an advisor to perform. A Harvard Business Review study conducted by researchers from the management consulting firm Bain & Company identified thirty different elements of value ranging from functional (saves time, simplifies, informs) to life-changing (addresses motivations, heirlooms, hope). An advisor could think about these elements as the jobs they are being hired to perform. At the very least, these elements can be used as inspiration when thinking about the specific jobs that a client may hire an advisor to perform.

It’s important to note that while some prospects may approach an advisor to perform a seemingly functional job, such as “reduce the risk in the portfolio” or “make money”, what the prospect is actually seeking may not be considered functional at all. For example, the client may frame their request in terms of a functional job (e.g., finding a way to reduce the risk in their portfolio), but what they are really looking for is help with an emotional job (e.g., reducing their anxiety). As another example, a client may ask if their portfolio could sustain an early retirement (analysis for a functional job), but what they really want to know is more of a life-changing analysis to see if they have what it takes to thrive as a financially independent person.

The key point is that prospects are not necessarily hiring advisors because of the holistic financial plan they create; instead, they are really hiring the advisor to help with a particular functional, emotional, social, or aspirational job that will be unique to the prospect’s needs. And by considering the particular job that clients need help with, advisors can choose the right messages that will most likely resonate with prospects looking to hire them to do a job.

Using the Job-Mapping Method To Identify Jobs To Be Done For Clients

While identifying a prospect’s or client’s desired Jobs To Be Done can be time-consuming, mapping out the steps that a client would take if they were to complete the job on their own (without the support or assistance of an advisor) can be one way to efficiently tackle the process.

In their 2008 Harvard Business Review article, The Customer-Centered Innovation Map, authors Lance Bettencourt and Anthony Ulwick outlined such a process, using an 8-step job-mapping methodology for businesses to assess the value of their services. Advisors can use this approach to determine where clients are getting stuck as they try to address their own financial plan, which ultimately leads to the client contacting the advisor to perform a job. An advisor may realize that there is a common theme among their clients when performing this exercise.

According to Bettencourt and Ulwick, the following 8 steps are common to all jobs and can be used to assess where services may fall short in meeting what their clients actually need. Which is very similar to the financial planning process that advisors follow when working with clients.

Thus, when an individual needs to address a financial planning issue or plan for a financial goal on their own, they would follow the eight steps listed in the framework above to complete the job or until they became stuck and needed help from an advisor.

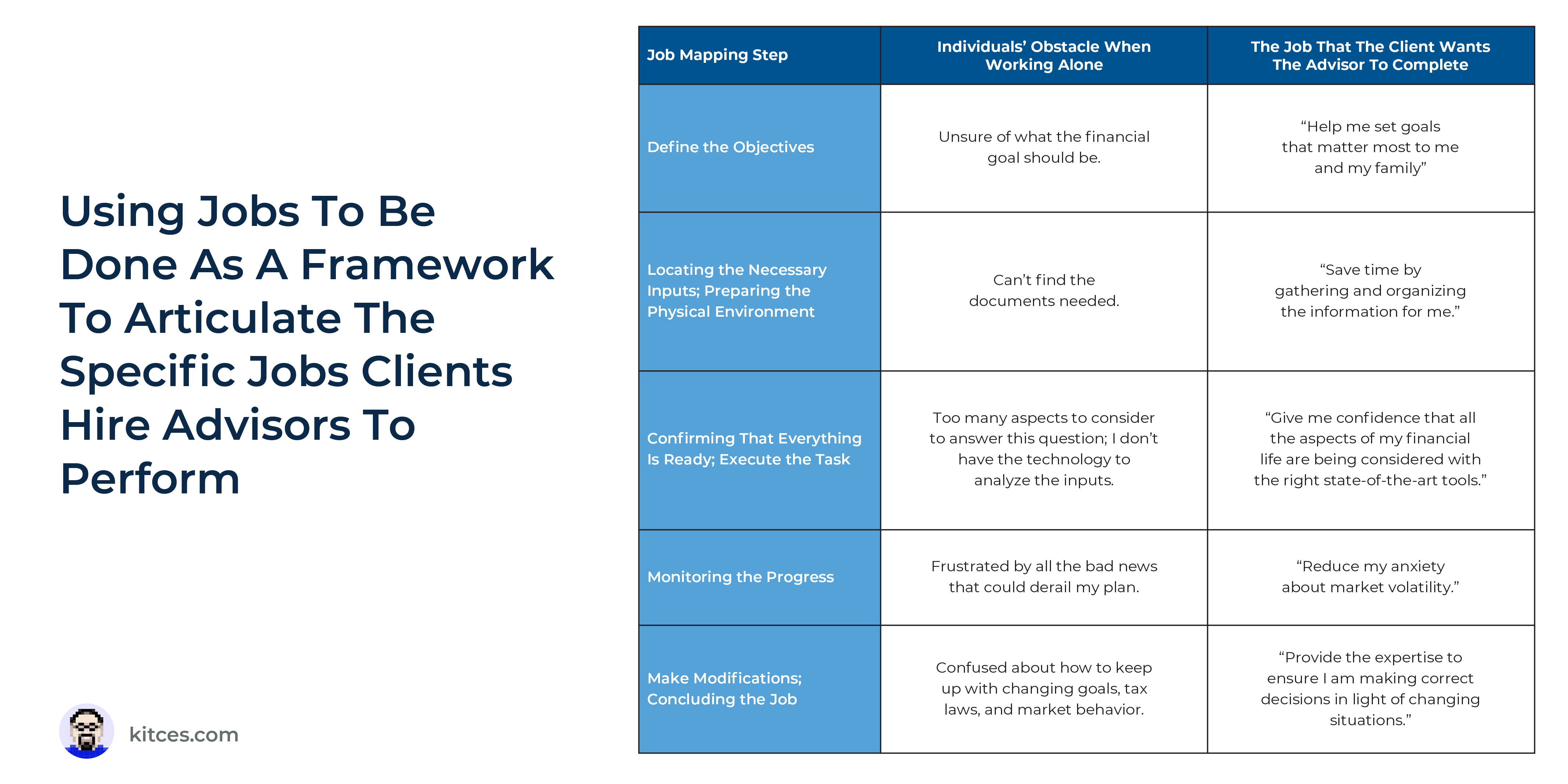

The first four Pre-Execution steps all revolve around preparing to actually develop the plan. Initially, the individual would define what they wanted to accomplish (e.g., the goals they were planning for). Then, they would gather the documents and information they needed. The next step would be to make sure they had the tools (or physical environment) to do the job – in this case, it would be to find the right software to assist in developing the financial plan.

After gathering the necessary tools and information, the individual could move on to the Execution phase of the job: creating the plan. This step would involve conducting the research, analyzing the information, developing a list of action items, and implementing the action items.

Finally, once the plan has been created and implemented, the final Post-Execution phase would involve monitoring the plan to make sure that it stays on track by adjusting for changing economic conditions and tax law updates. The job would ultimately be completed when the person’s goal of retiring is finally reached.

While many people endeavor to start this process on their own, they often run into roadblocks that keep them from continuing. At just about any stage in the process, an individual could run into a problem. Perhaps they get stuck early in the process because they don’t know how to define their goals, or they become overwhelmed by the amount of knowledge or research they need to do. As a result, they might decide to hire an advisor to help them complete the job they originally set out to do on their own.

However, from the perspective of the Jobs To Be Done framework, the primary reason the person decided to hire an advisor in the first place was not that they wanted an answer to their initial retirement question; it was because they needed help to overcome a particular obstacle that impeded them from finding the answer on their own.

For example, a person may decide that they want to retire early and use the 8-step process above to tackle their goal. But very quickly, they run into an obstacle because their spouse enjoys working and doesn’t want to retire early. Which brings them to the realization that they are not yet able to properly define their goal. In this case, they may seek an advisor to help perform a specific job such as, “Help me set goals that matter most to me and my family.”

Now imagine an individual (and their spouse) who both want to retire early. They are able to complete the first step of the 8-step process of defining their agreed-upon objectives. But when they move on to Step 2, “Locating the Necessary Inputs”, they run into a new problem – they are too busy juggling their work and family responsibilities that they aren’t able to find the time to find and organize the documents they need. In this case, they may hire an advisor to help them with the job to “Save time by gathering and organizing the information for me.”

By examining each of the Job Mapping steps, the advisor can gain insight into what would make a prospect turn to an advisor for help, identifying the particular pain points that such a do-it-yourself prospect might face. Trends may emerge among the advisor’s target audience (or even among their existing clients), which can help the advisor leverage various roadblocks by clearly describing how their service or process would help overcome those obstacles.

For example, an advisor might discover that a lot of existing clients struggle with finding time to work on their financial planning needs for a variety of different reasons. An advisor could incorporate this insight into their marketing messages by saying, “We spend the time to help you plan for your financial future, so you can spend your time doing what matters most to you.” Further messaging can support this statement by elaborating on how the advisor’s process actually saves their clients’ time, reinforcing the message that they really do focus on the jobs that matter most to their clients!

While communicating the value financial advisors can provide to their clients will always be difficult, there are many different strategies advisors can consider to help them structure the most effective messaging. But because all prospects are unique – each with their own values, goals, and preferences – there is no single communication strategy that will resonate with all prospects.

However, by honing in on a particular type of client with some common problem to be solved, advisors can use a new way of framing their value through a Jobs To Be Done Framework. This approach can appeal to the target client by framing the advisor’s services as a way to fulfill the specific job the client needs to have done. At the same time, it helps advisors to communicate their value in a manner that will resonate with clients and help them determine how the advisor will meet their specific and unique needs!

{kind=link}