Financial advisors who pay third parties to solicit or refer prospective clients to generate new business have historically been subject to the SEC’s Cash Solicitation Rule. However, that rule was drafted in an era where most paid referral relationships were between individuals, such as a financial advisor who paid a third-party accountant to refer clients their way. In recent years, though, the growing use of lead-generation services, advisor networks, and ‘advisor-matching’ tools, referred to as “operators” in the Marketing Rule’s Adopting Release, has given rise to third-party solicitation activity that often looks more like advertising directly to prospective clients. Which, in fact, often meets the definition of an ‘endorsement’, subjecting many third-party relationships to the Marketing Rule’s compliance regulations.

In response to this shifting landscape, the SEC has scrapped its old Cash Solicitation Rule and folded the regulations for third-party solicitation into its new Marketing Rule, which had a mandatory compliance deadline for SEC-registered advisers of November 4, 2022. In the new rule and subsequent Adopting Release, solicitors have been redesignated as “promoters”, referring to anyone who provides a testimonial or endorsement for an investment adviser, whether or not any compensation was paid. And when an advisor provides compensation for a testimonial or endorsement, the testimonial or endorsement is considered an advertisement under the SEC Marketing Rule. Which means that third-party solicitors providing such advertisements will require a greater investment into due diligence and oversight going forward than under the previous rule.

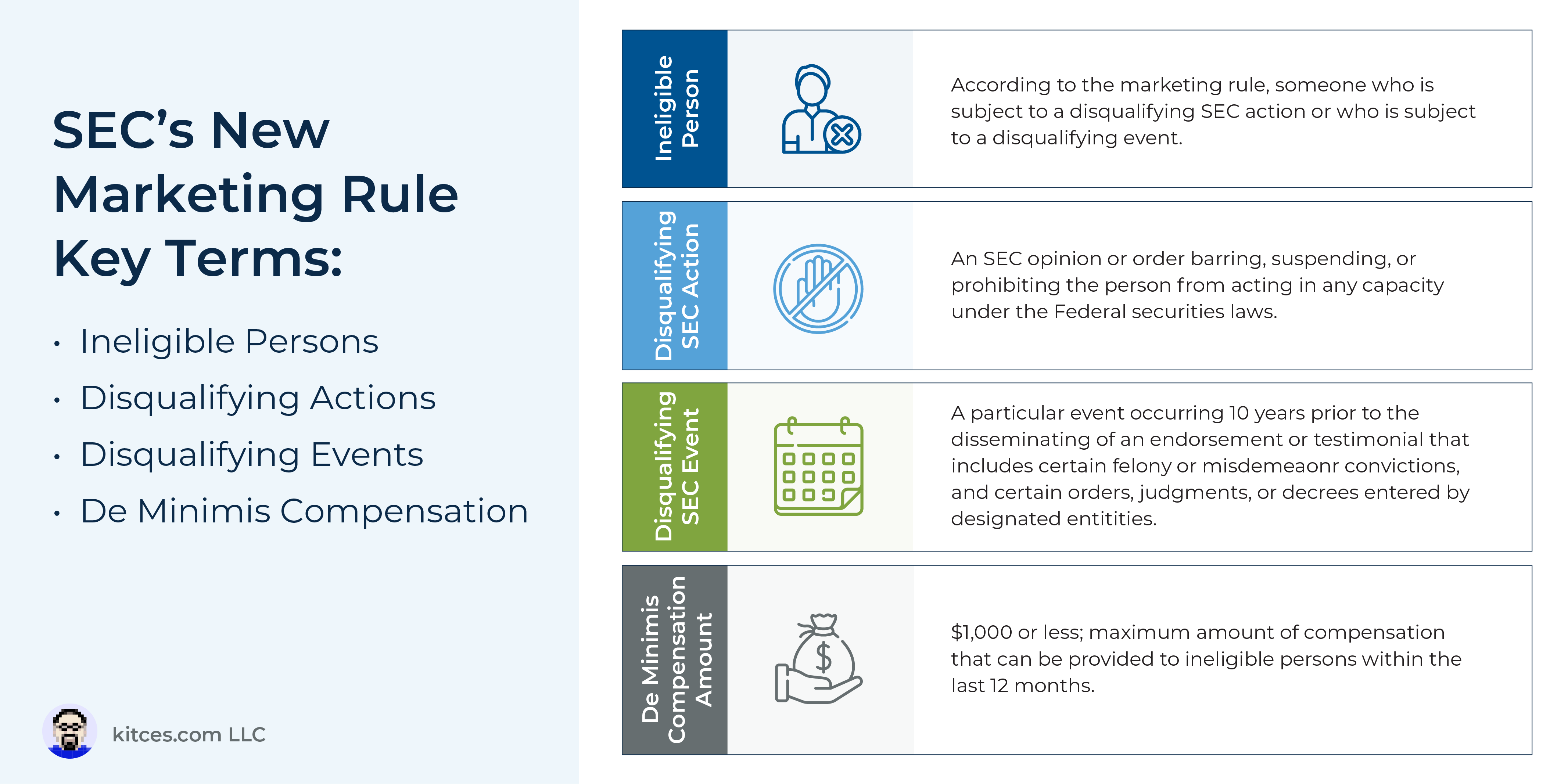

The upshot is that any paid solicitation agreements between advisers and third parties are now required to comply with the SEC Marketing Rule’s advertising regulations for testimonials and endorsements. These requirements include ensuring that promoters are eligible to receive compensation for testimonials or endorsements (i.e., they are not disqualified by the SEC from acting in any capacity under Federal securities law), entering a written agreement between the adviser and promoter (unless a de minimis compensation threshold, generally $1,000 during the preceding 12 months, is not met), making specific disclosures to prospective clients about the terms of the solicitation agreement and any material conflicts of interest, and, for the adviser, taking reasonable steps to ensure that promoters themselves are complying with the Marketing Rule’s requirements. Additionally, investment advisers should ensure they disclose the promoter relationship in their Form ADV Part 1 and Form ADV Part 2A.

The key point is that all paid solicitation agreements – including both existing and new relationships between advisers and promoters – are generally considered to involve advertisements and will be subject to the Marketing Rule, so for all SEC-registered advisers who are in (or are considering) such relationships, it’s crucial to review all aspects of the relationship in order to ensure compliance. And given the fact that advisers are ultimately responsible for ensuring the compliance of the promoters they utilize – including advisor networks and advisor-matching services that have gained popularity in recent years – using third-party solicitors might require a greater investment into due diligence and oversight going forward than under the previous rule, which could have long-term implications for the cost versus benefits of using such arrangements in the future!

{kind=link}