The Reserve Bank of Australia has fired off the 11th rate hike in this cycle, raising the cash rate by 0.25 percentage points to 3.85%, the highest level since April 2012 – with further rate hikes flagged in a bid to rein in inflation.

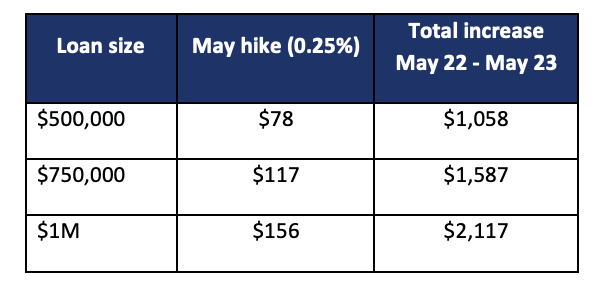

If lenders pass on the 0.25-percentage-point hike, as expected, the average owner-occupier with a $500,000 loan and 25 years remaining will see their repayments increase by $78. But as this was now the 11th rate hike since last May, that same borrower will see their repayments rise by a total $1,058.

“As a result of [RBA’s latest] decision, the average owner-occupier who hasn’t negotiated their loan since the first hike will soon be paying 6.61%,” said Sally Tindall (pictured above), RateCity.com.au research director.

See the table below for the expected increase in mortgage repayments:

Note: Based on an owner-occupier paying principal and interest with 25 years remaining. Starting rate is the RBA av. existing owner-occupier variable rate of 2.86% in April and assumes banks pass the hikes on in full.

RateCity.com.au estimated that after the latest RBA hike, a competitive variable rate will be under 5.5% for owner-occupiers paying principal and interest, with a handful of lenders likely to still offer rates under 5.25%.

“After a month’s reprieve borrowers were still catching up to the rate hikes rather than catching their breath. To have another one piled on top will feel like another kick in the guts,” Tindall said.

“Someone with a $500,000 debt at the start of the hikes, will now need to find more than $1,000 in spare change to stop their repayments from falling into the red. Some families may find this is the rate hike where they come up short.”

Borrowers need not take these rate hikes lying down, though, she said.

“Homeowners on an uncompetitive rate could potentially wind back the clock by four or five rate hikes, just by switching lenders,” Tindall said.

For instance, someone with a $500,000 debt and 25 years remaining on their loan could save up to $12,382 in the next two years by simply refinancing from the average variable rate to one of the lowest in the market.

Someone with a $1 million loan, meanwhile, could save an estimated $25,914 in the next two years by refinancing from the average rate to one of the lowest.

The estimates by RateCity.com.au were based on an owner-occupier switching from the average rate of 6.61% to a rate under 5.25% and includes the costs of refinancing and assumes the cash rate moves in line with CBA’s forecast.

Here’s some refinancing tips brokers can share with their clients:

- Check your new rate and compare it to what other lenders are offering

- Check your equity. If you own more than 30% of your home at today’s values, you might be eligible for rate discounts

- Don’t extend your loan term. Extending your loan back out to 30 years might lower your repayments, but you’ll pay for it in the long run

- Make higher repayments to save on interest and build a buffer for down the road

- Beware of cashbacks, as these might be offered at the expense of a higher rate

- Ask the new lender to waive upfront fees

Use the comment section below to tell us how you felt about this.

{kind=link}