The original SECURE Act, signed into law in December 2019, changed many of the long-standing rules governing IRAs and other retirement accounts, and no single measure in the legislation had a more seismic impact on planning than the changes to the post-death distribution rules for retirement accounts. Specifically, the law stipulated that “Non-Eligible Designated Beneficiaries” (i.e., designated beneficiaries who are neither surviving spouses nor fall into a limited number of other categories) would need to empty the inherited retirement account by the end of the 10th year after the decedent’s death (and would no longer be able to ‘stretch’ the distributions over their own life expectancy).

While many observers expected that Non-Eligible Designated Beneficiaries would not be required to take annual distributions during this 10-year period (as long as the account was fully distributed by the end of the 10th year), the IRS in February 2022 issued Proposed Regulations that would make a subset of these beneficiaries (those who inherit accounts from decedents who died on or after their Required Beginning Date) subject to both the 10-Year Rule and annual Required Minimum Distributions (RMDs). The caveat, however was that these were merely proposed regulations, and as the year went on both beneficiaries and their advisors remained in limbo regarding whether they would need to take distributions in 2022 (or should have taken them in 2021) in order to avoid potential penalties. Until finally, the IRS issued a notice in October 2022 waiving any potential penalties for Non-Eligible Designated Beneficiaries for 2021 and 2022 for missing RMDs from their inherited retirement accounts, effectively eliminating the RMD requirements for those years… but notably not addressing the requirements for 2023 and onward.

Amid this backdrop, the IRS in July 2023 released Notice 2023-54, which provides relief for Non-Eligible Designated Beneficiaries who inherited retirement accounts from an owner who died on or after their Required Beginning Date by eliminating any penalties for failing to take (potential) RMDs for 2023, essentially ‘punting’ RMDs yet again until (at least) 2024 – though still lacking any detail as to when Final Regulations might be expected that could clarify RMD requirements for future years. Notably, however, while this group of Non-Eligible Designated Beneficiaries doesn’t have required distributions from their inherited accounts for 2023, they can still make voluntarily distributions – and may actually be better off in doing so, if it can prevent future spikes in taxable income when the beneficiary is eventually forced to make (bigger) distributions to empty the account.

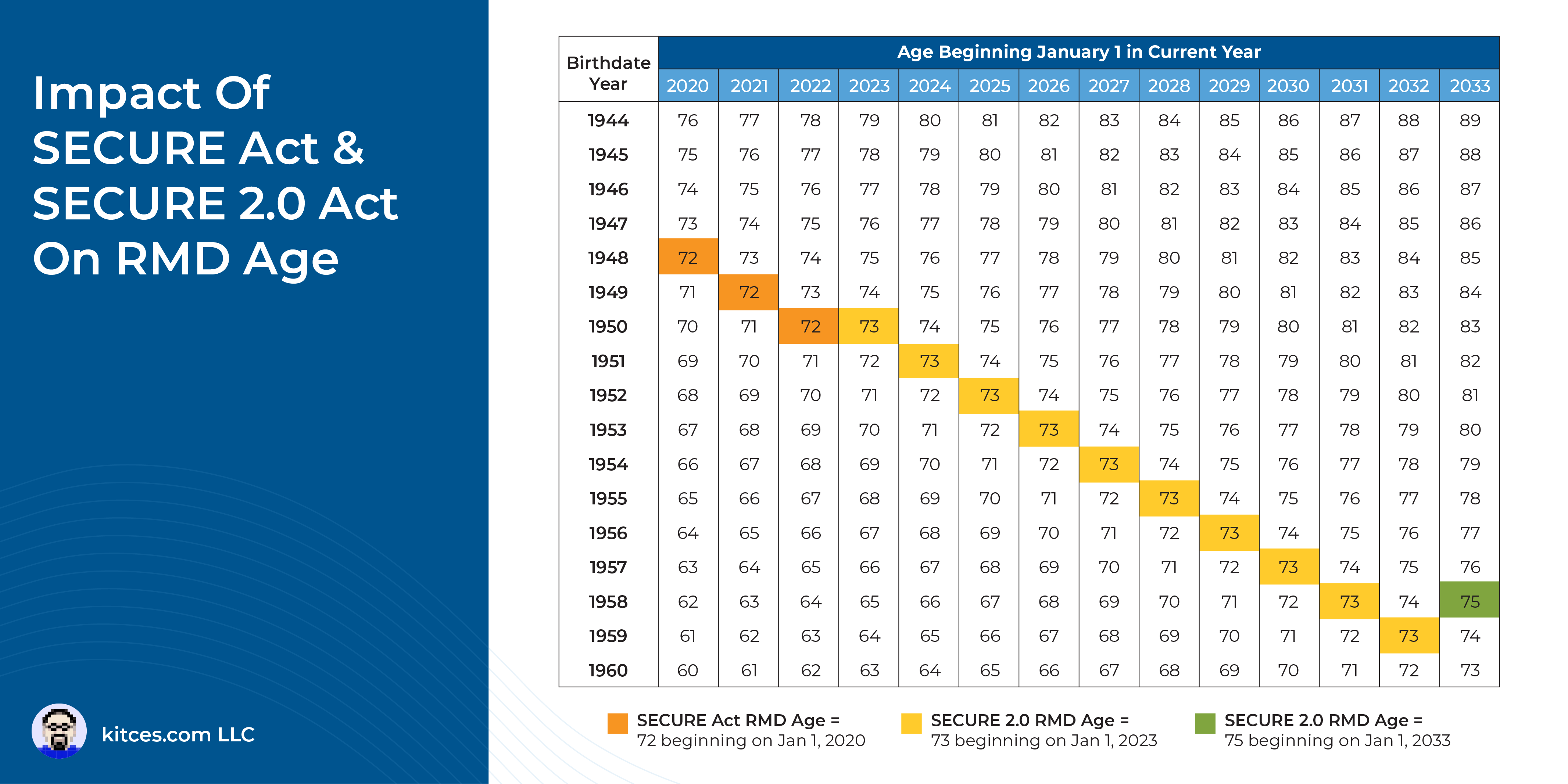

In addition to the guidance regarding inherited accounts, Notice 2023-54 also offers a temporary RMD reprieve to retirement account owners born in 1951, who, as a result of the “SECURE 2.0” law passed in December, are now no longer required to take RMDs until they turn 73 (i.e., in 2024) – but who may not have learned about the delay before taking what would have been their 2023 RMD (or who may not have been able to cancel a scheduled RMD in time) due to SECURE 2.0 being passed so late in the year. Those individuals are now permitted to treat these distributions as a rollover, and unlike traditional rollovers, they may complete the rollover outside of the usual 60-day window (provided such rollovers are completed by the end of September 2023). Further, Notice 2023-54 allows such rollovers to be completed even if they would otherwise be in violation of the once-per-year rollover rule.

Ultimately, the key point is that IRS Notice 2023-54 provides important answers to some of the most pressing questions taxpayers and their advisors have had regarding RMD requirements for 2023. Nonetheless, we’re still in the early innings of figuring out how to handle the changes made first by the original SECURE Act and later on by SECURE 2.0, meaning there will be plenty of opportunities for advisors to keep clients up-to-date on the latest changes as further guidance rolls in!

{kind=link}