The announcement of the merger between Charles Schwab and TD Ameritrade in November 2019 kicked off a marathon of preparation for advisory firms to transition their clients on the TD Ameritrade custodial platform to Schwab. And with the final conversion of clients scheduled to take place over the upcoming Labor Day weekend of 2023, the marathon is approaching its final sprint toward the finish line. While many RIAs have already tackled some of the bigger issues around the conversion such as informing clients of the changes and updating regulatory documents, there are still some operational intricacies in the TD Ameritrade to Schwab transition process for advisors to address that could cause headaches if they’re missed.

In this Guest Post, Grier Rubeling, a transition consultant for RIAs and founder of Advisor Transition Services, offers a series of actionable tips to help advisors (and their clients) get through the ‘Schwabitrade’ transition smoothly.

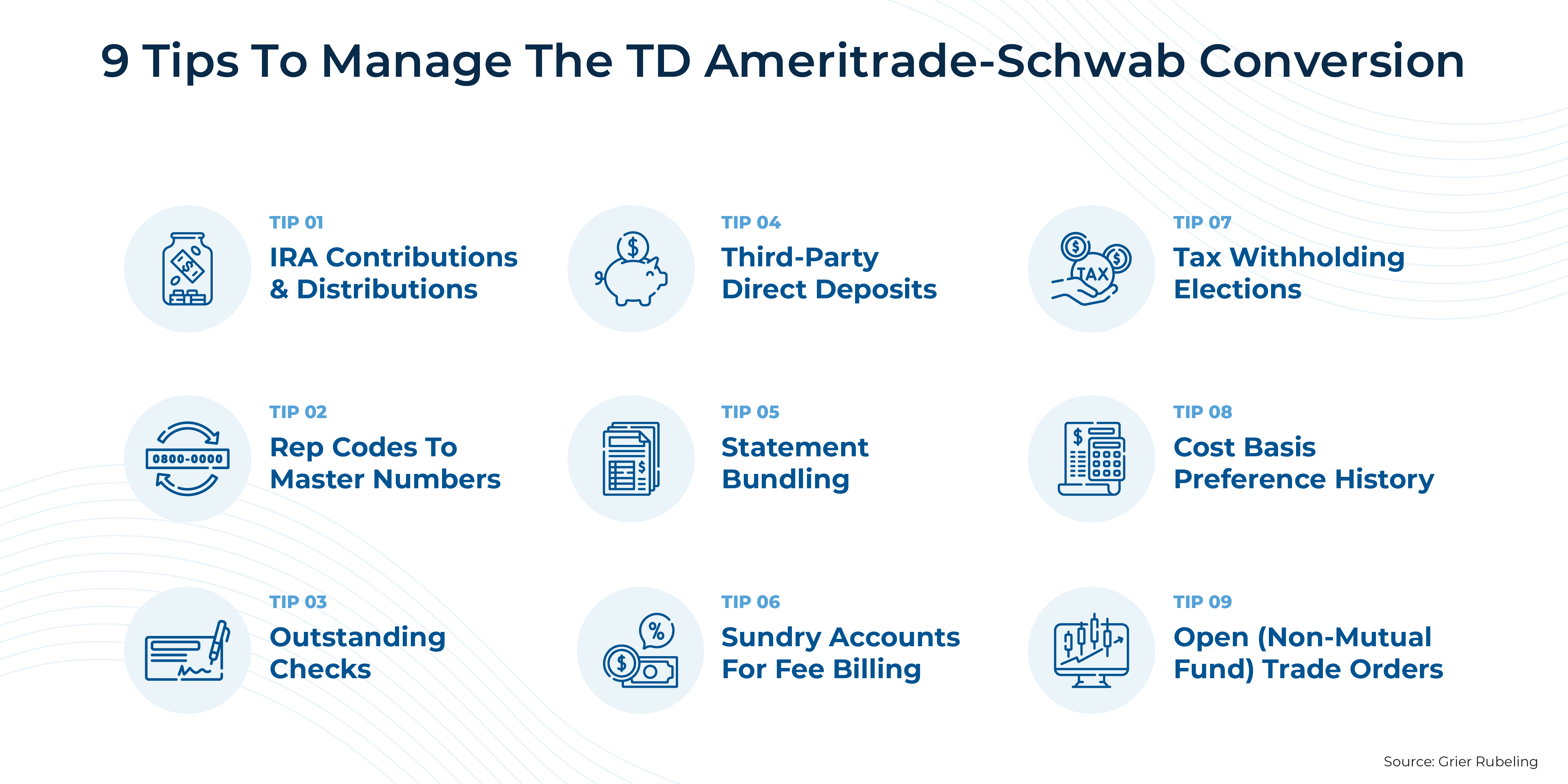

At a high level, some of the operational challenges of the transition amount to adjusting to Schwab’s way of doing things for advisors who are used to TD Ameritrade. For instance, TD Ameritrade rep codes that are used to organize client accounts will be converted to an 8-digit Schwab “master number”, which is used for account grouping, billing, account service, and more. Advisors will also need to familiarize themselves with Schwab’s treatment of sundry accounts for fee billing and tax withholding elections for distribution, both of which differ in some key ways from TD Ameritrade.

Additionally, although Schwab states that most advisors’ tax-lot settings for cost basis purposes will carry over after the conversion, some advisors with specific personalized settings (such as having multiple default lot-selection methods for different security classes) will likely need to research Schwab’s Transition Planning Guide for information on whether and how those settings may change post-conversion. And any changes made between now and the conversion date of Labor Day weekend likely won’t carry over, meaning they would need to be re-implemented once the transition is complete.

Finally, there is a category of tasks that involves tying up some loose ends that may remain after the conversion. For example, any checks or third-party direct deposits addressed to TD Ameritrade will be accepted for around 90 days after the conversion, but may encounter delays, so it’s important to ensure that clients’ deposit instructions are updated quickly. Additionally, any open trade orders (e.g., Good-Til-Canceled or Good-Til-Date orders) for non-mutual-fund securities will be canceled and will need to be re-ordered after the conversion. And for clients with IRAs, all contribution and distribution reported by Schwab will reflect only post-conversion transactions – meaning that advisors will need to keep careful records for any clients who contributed or withdrew prior to the conversion.

Ultimately, while this is by no means a fully comprehensive list of potential issues for advisors to consider about the TD-to-Schwab conversion, they may be some of the most common and important to address to ensure a smooth transition. Because with Schwab’s customer service resources likely to be stretched thin in the days and weeks following the conversion, the more potential issues that advisors can identify and address before they become a problem, the less of the advisor’s own resources need to be tied up in operational headaches (allowing them to keep the focus on their client-facing work)!

{kind=link}