Nowadays many Liquid Funds giving us decent around 7% safe and less volatile returns. Should we invest in Liquid Funds for Long Term Goals?

What are Liquid Funds?

Liquid Funds are debt mutual funds where the fund manager has a mandate to invest in debt and money market securities with a maturity of up to 91 days. This is the definition of SEBI.

However, this looks to me like the wide open place for fund managers to invest in any debt and money market security (even low-rated security). With 91 days period, one can reduce the interest rate risk volatility. However, if the fund manager took the risk and invested in low-rated papers, then there is always a risk of default or downgrade.

Many may be surprised by my notion. However, if you check the history (Is Liquid Fund Safe And Alternative To Savings Account?), there are instances where one Liquid Fund crashed by almost 7% in a single day!!

This incident is a classic example and caution to those who BLINDLY believe that Liquid Funds are safe and less volatile. If the fund manager took a BLIND risk, then you have to face the risk.

Why are Liquid Funds now giving 7% fantastic returns?

It is all because of the inflation trajectory in which we are currently in. Higher inflation led to higher interest rates. This impacted a fall in bond prices. The impact of this is more on long-term bonds than the short-term bonds. Just because of this, the one-year returns show around 7%.

Just because of this reverse cycle, we can’t assume that going forward in the future Liquid Funds will generate 7% returns safely.

Should we invest in Liquid Funds for Long Term Goals?

As I mentioned the reason for such a fantastic performance of liquid funds for a year, assuming the same for the future is not worth it. Instead, let us try to understand the probability of past returns by considering the various rolling returns of a liquid fund. I am considering a liquid fund which is the oldest and also of the highest AUM. I found that SBI Liquid Fund (Direct) is the oldest with the highest AUM (Rs. 58,177 Cr).

I have taken the last 10 years of NAV history. Hence, we have around 3,741 daily data points.

Let us try to understand the volatility for 1-year, 3-year, and 5-year rolling returns.

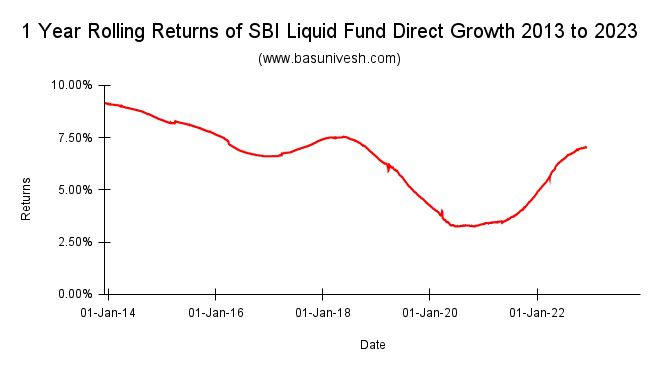

1-Year Rolling Returns of SBI Liquid Fund Direct-Growth 2013 to 2023

Notice the volatility. The maximum return is 9.16%, the minimum is 3.25% and the average is 6.29%.

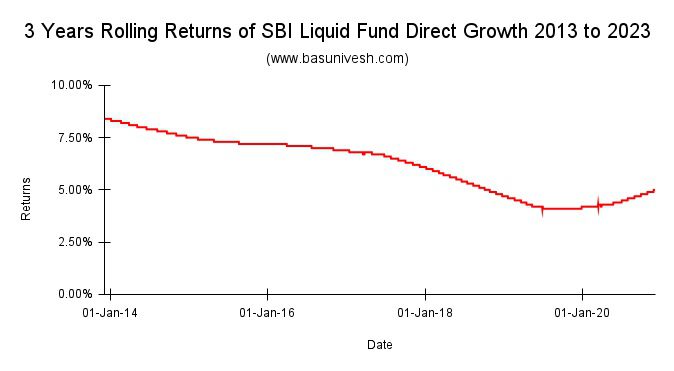

3-Year Rolling Returns of SBI Liquid Fund Direct-Growth 2013 to 2023

The maximum return is 8.4%, the minimum is 4.1% and the average is 6.12%. The average returns of 1-year rolling returns and 3-year rolling returns look almost the same!!

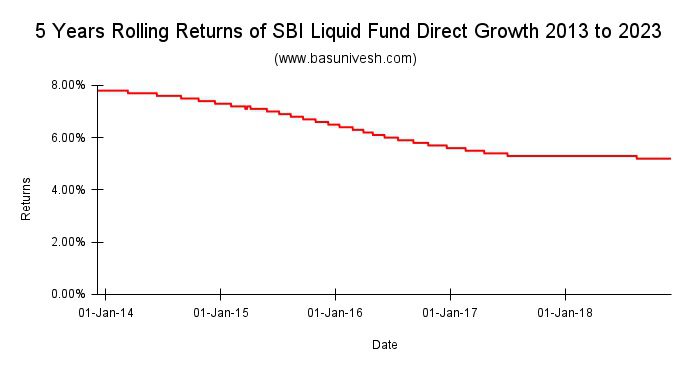

5-Year Rolling Returns of SBI Liquid Fund Direct-Growth 2013 to 2023

The maximum return is 7.8%, the minimum is 5.2% and the average is 6.28%. The average returns of 1-year rolling returns, 3-year rolling returns, and 5-year rolling returns look almost the same(6.29%, 6.12%, and 6.28%)!!

If the Liquid Funds are SAFE (avoiding default and credit risk) and less volatile, then why such a wide range of return possibilities even after holding for 5 years?

The answer is even though Liquid Funds may to a certain extent completely avoid the default or downgrade risk by investing in government securities or money market instruments, they can’t run away from interest rate risk.

Hence, just because of the higher inflation and higher interest rate cycle, if these funds are generating around 7% returns in a year does not mean they provide the same decent returns in the future. If you look back at the history, you notice from the above charts that there were certain periods where the same Liquid Funds generated fantastic returns of over 7.5% for 5 5-year holding period. But at the same time, we must understand the reasons behind this and also in which interest cycle we are in.

Why one must invest in Liquid Funds?

Due to the recent tax changes in Debt Funds (Debt Mutual Funds Taxation From 1st April 2023), there is no great advantage of PARKING (I am not using the words investing) your money in Liquid Funds.

Then who can and when one can consider Liquid Funds? One can use the Liquid Funds for their short-term goals like less than 2-3 years and unsure of exactly when they need the money. Otherwise, a simple Bank FD or RD is enough to cater to your requirements.

One more thing to think is even though name of these funds is LIQUID, they are not as liquid as your Bank FDs (if you booked through internet banking). Usually, it takes a day or two to redeem your money from liquid funds. Instant redemption in Liquid Funds has certain limitations like either Rs.50,000 or 90% of the fund value (whichever is earlier).

Considering all these aspects, don’t invest randomly just because of the current returns. Rather than that, you must have a clear purpose in choosing the Liquid Funds. As I have given one classic incident of past credit risk history, don’t be in the wrong belief that Liquid Funds are safe. Instead, have a look at the portfolio and then take a call.

{kind=link}