Birlasoft Ltd. – Bold. Agile. Ambitious

Incorporated in 1990 and headquartered in Pune, Birlasoft Ltd. is a global leader at the forefront of Cloud, AI and Digital Technologies. It is a part of CK Birla Group, a US$ 2.9 billion diversified conglomerate with global presence across five continents in three main industry clusters: Technology and Automotive, Home and Building solutions, and Healthcare & Education. Birlasoft derives most of its revenues from the export markets, where it serves customers chiefly in the Banking, Financial Services and Insurance (BFSI), Manufacturing, Lifesciences, and Energy & Utility (E&U) sectors. As of 31 March 2023, the company had a headcount of 12,193.

Products and Services

Birlasoft offers services in the lines of Digital & Cloud, DATS – Data Analytics Transformation Services (expertise in machine learning, artificial intelligence, data mining and predictive modelling), ERP (comprehensive enterprise services such as process execution, product management, marketing, and distribution/supply chain) and ICTS – Infrastructure and Cloud Technology services (Cloud migration, workplace transformation, network modernization, and system integration).

Subsidiaries: As of FY23, the company has 14 subsidiaries, including step-down subsidiaries and no associate or joint venture company.

Key Rationale

- Diverse range of projects – Birlasoft is implementing a strategy of executing increased number of short-term projects (duration of one year or less) and change requests, majority of such contracts coming from their existing client base. This has aided the company to partially offset the impact of furloughs during the quarter. Leveraging strength and retaining and mining existing accounts is visible in company’s deal flows and top account growth. The management has started to consider acquiring short term projects as a sustained strategy for the company.

- Leadership team transition – The company is undergoing employee and organisational transformation, including active hiring of new professionals, especially for key leadership positions such as New Chief Executive Officer for Rest of the World (ROW – comprising of all regions outside America – includes Europe, U.K., Asia Pacific, including India) region, new CEO & Managing Director hired last year. The management expects the experience in tech services industry and exceptional leadership that these professionals possess to superhead the company in its futuristic vision and execution capabilities.

- Q3FY24 – In constant currency, Birlasoft reported a revenue of Rs.1,343 crore marking an increase of 10% compared to the Rs.1,221 crore of Q3FY23. EBITDA stood at Rs.214 crore compared to the Rs.7.4 crore of Q3FY23, a surge by 2796% YoY. For the first time the company crossed the Rs.150 crore mark to report net profit of Rs.161 crore which is a robust growth of 1082% against a loss of Rs.16.4 crore of same period in the previous year. Amongst the verticals, Energy & Utilities delivered the highest growth of 7.9% due to new deal ramp-ups, followed by Manufacturing (1.7%) and Life sciences (1.3%) compared to Q2FY24. BFSI as a vertical tends to be relatively more affected by furloughs and hence it has registered a quarter-on-quarter decline of 0.7%. Operating cash flow during Q3 has been at about 141% of EBITDA.

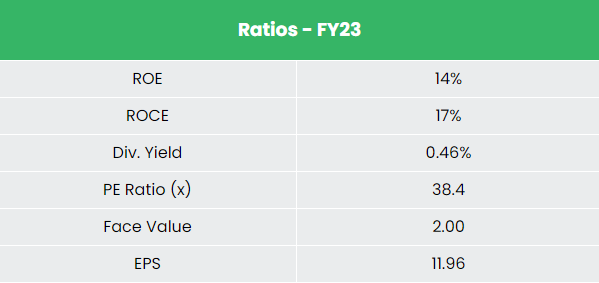

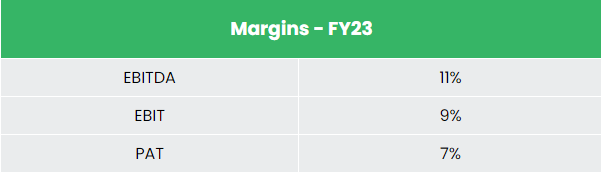

- Financial performance – The company has generated a revenue and PAT CAGR of 13% and 14% over the period of 3 years (FY20-23). Average 3-year ROE & ROCE is around 16% and 21% for FY20-23 period. The company has robust capital structure with a debt-to-equity ratio of 0.03.

Industry

The IT & BPM sector has become one of the most significant growth catalysts for the Indian economy, contributing significantly to the country’s GDP and public welfare. The sector is consistently strengthening its digital capabilities by adopting deep tech technologies and focusing on deploying emerging technology solutions such as AI, Cybersecurity, and IoT. India’s IT industry is likely to hit the US$ 350 billion mark by 2026 and contribute 10% towards the country’s gross domestic product (GDP), India’s IT and business services market is projected to reach US$ 19.93 billion by 2025. The Indian software product industry is expected to reach US$ 100 billion by 2025. Data annotation market is expected to reach US$ 7 billion by 2030 due to accelerated domestic demand for AI. India is also amongst the fastest growing Fintech markets in the world. Indian FinTech industry’s market size was $50 Bn in 2021 and is estimated at ~$150 Bn by 2025.

Growth Drivers

In the Union Budget 2023-24, the allocation for IT and telecom sector stood at Rs. 97,579.05 crore (US$ 11.8 billion). Cabinet approved PLI Scheme – 2.0 for IT Hardware with a budgetary outlay of Rs. 17,000 crore (US$ 2.06 billion). Up to 100% FDI is allowed in Data processing, Software development and Computer consultancy services; Software supply services; Business and management consultancy services, Market research services, technical testing and Analysis services, under automatic route.

Competitors: Coforge Ltd, Latent View Analytics Ltd etc.

Peer Analysis

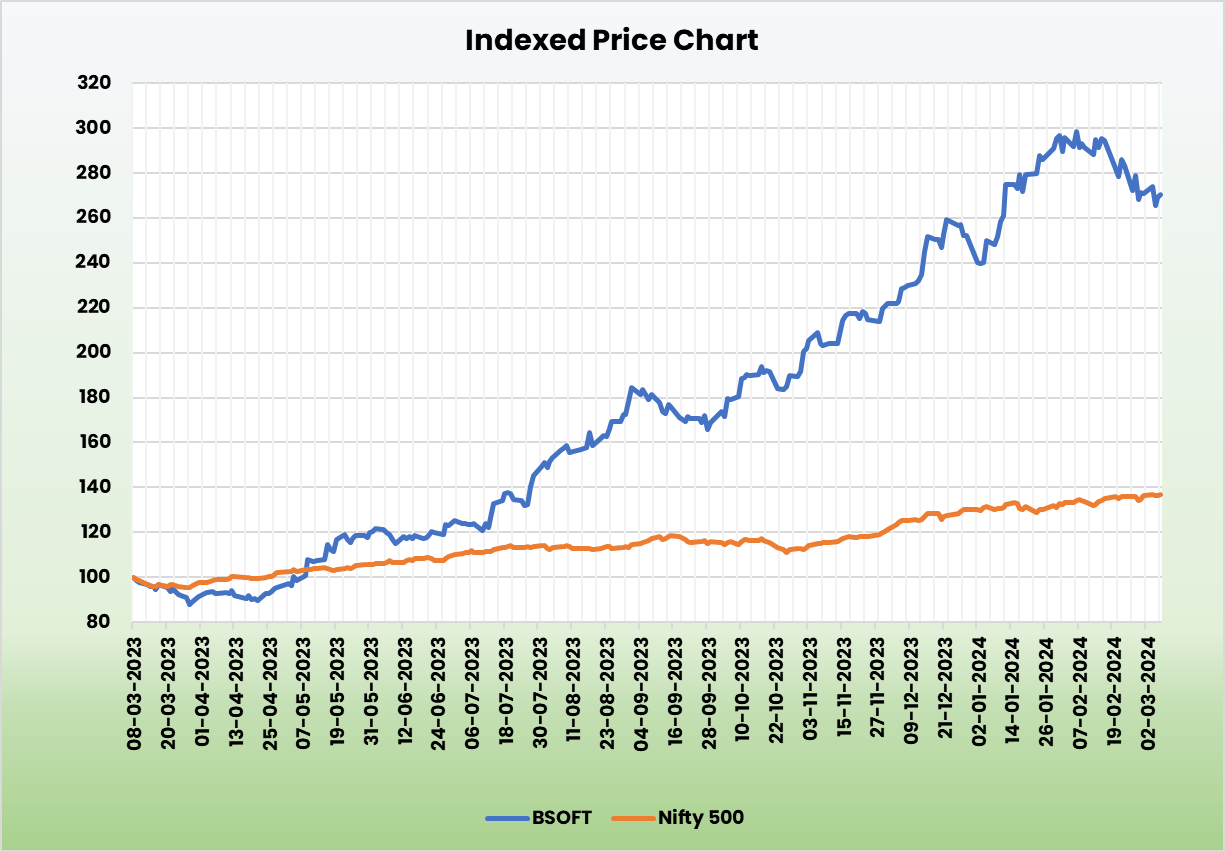

While comparing with the peers, Birlasoft is undervalued stock trading at a cheaper price to earnings ratio with an overall healthy performance metrics. In the trailing twelve months (TTM), net profit growth stood at 58% for Birlasoft whereas the same is at -7% and -6% for Coforge and Latent View respectively.

Outlook

Birlasoft had signings of a total contract value of $218 million during Q3FY24, in spite of the third quarter being a weak quarter for the industry. The fundamentals of the business is robust, evident in the quantum of the deal wins during the quarter as well as cash flow generated. Sustained strategy of taking short term projects is adding value to the revenue and margin. The company is focusing on account mining efforts, resulting in growth across key accounts with top accounts growing at 3.2% compared to the previous quarter. However, the macroeconomic conditions and the extent to which client’s decide to optimise their spending are key factors to lookout for. Strategy to develop inhouse talent and gradually reduce subcontracting is proving to be successful. It recorded an expansion in EBITDA margin to 16% during Q3FY24, even after absorbing a large part of the organization-wide compensation hike and promotions that became effective from the 1st of September 2023.

Valuation

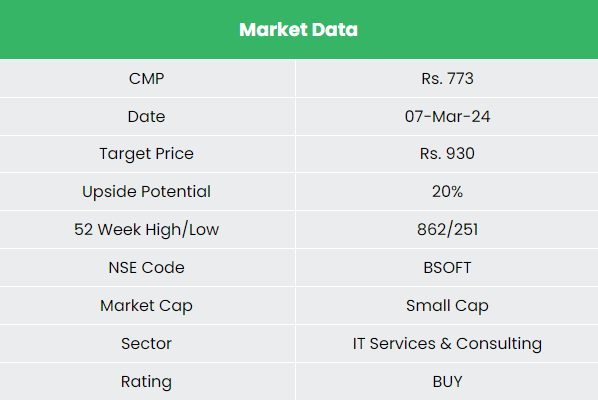

Birlasoft Ltd’s focus on deal execution, top account mining, building capability inhouse and parallel reduction of subcontracts is favourable for the company to achieve more deal wins in mid to long term. We recommend a BUY rating in the stock with the target price (TP) of Rs. 930, 27x FY25E EPS.

Risks

- Macroeconomic headwinds – Tighter monetary and fiscal policies and recessionary environment in major markets resulting from macroeconomic pressures might slowdown the rate at which the company is able to secure deals.

- Forex Risk – The company has significant operations in foreign markets and hence is exposed to forex risk. Any unforeseen movement in the forex market can adversely affect the company.

Recap of our previous recommendations (As on 07 Mar 2024)

Please click on the below links to read our previous reports:

Other articles you may like

Post Views:

63

{kind=link}