Monte Carlo simulations have become a central method of conducting financial planning analyses for clients and are a feature of most comprehensive financial planning software programs. By distilling hundreds of pieces of information into a single number that purports to show the percentage chance that a portfolio will not be depleted over the course of a client’s life, advisors often place special emphasis on this data point when they present a financial plan. However, the results of these simulations generally don’t account for potential adjustments that could be made along the way (e.g., decreasing withdrawals if market returns are weak and the probability of success falls, or vice versa), making them somewhat less useful for ongoing planning engagements where an advisor could recommend spending changes if they become necessary.

With this in mind, retirement income guardrails, which provide strategies that pre-determine when spending retirement adjustments would be made and the spending adjustments themselves – have become increasingly popular. Nonetheless, while these thresholds and the dollar amount of potential spending changes might be clear in the advisor’s mind, they often go unspoken to the client. Which can lead to tremendous stress for clients, as they might see their Monte Carlo probability of success gradually decline but not know what level of downward spending adjustment would be necessary to bring the probability of success back to an acceptable level.

But by communicating the guardrails withdrawal strategy (and not necessarily the underlying Monte Carlo probability of success changes) to clients, advisors offer them both the portfolio value that would trigger spending changes and the magnitude that would be prescribed for such changes. Notably, while advisors have the power to determine these guardrails using traditional Monte Carlo software, doing so can be cumbersome and can involve calculating initial spending levels that are reasonable for a client’s portfolio size, solving for the portfolio values that would hit the guardrail thresholds, and determining the spending changes corresponding to the desired adjustment once a guardrail is hit (though there are specialized retirement income software programs available that can make these calculations easier).

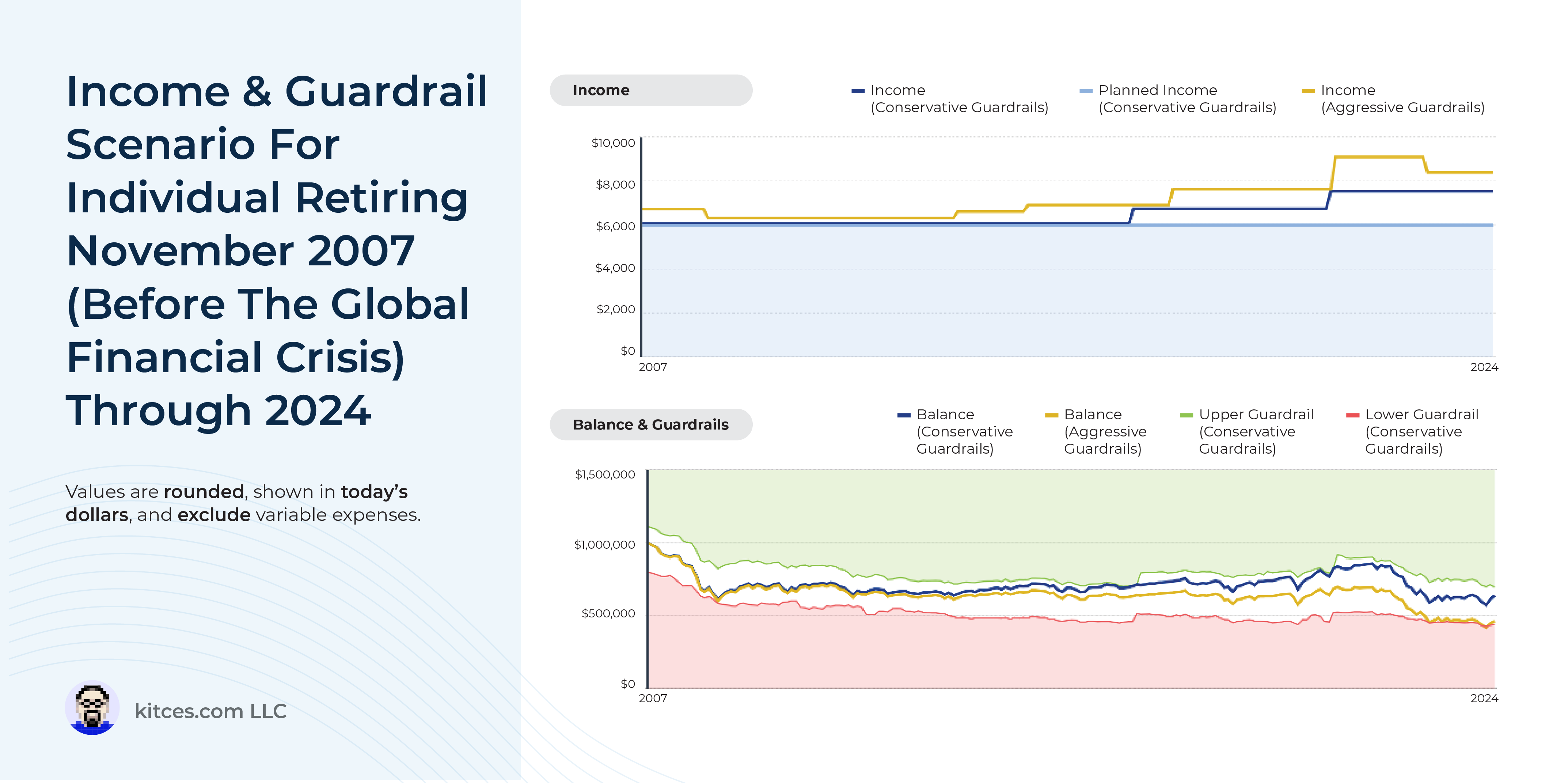

Even with the knowledge of potential short-run changes that a guardrails strategy might call for, a client may be concerned about additional income adjustments amidst an extended market downturn. One way advisors can give clients more confidence regarding this long-term outlook is to ‘stress test’ the plan with hypothetical scenario tests modeling some of the worst historical sequences of returns (e.g., the Great Depression or the Global Financial Crisis), showing clients when and to what degree spending cuts would have been necessary. This exercise can also give advisors and clients the opportunity to adjust the guardrail parameters depending on the client’s risk tolerance (e.g., a client who really wanted to guard against downward-spending-adjustment-risk might forgo income increases entirely).

Ultimately, the key point is that the probability-of-success results of Monte Carlo simulations can be highly stressful for clients, worrying them about the impact on their spending from a future market downturn. But by calculating guardrails and communicating the requisite spending adjustments that would protect the client’s overall outlook, and how the approach would have fared in some of the worst historical market environments, advisors can help clients mentally prepare for potential adjustments while bolstering their confidence in their financial plan!

{kind=link}