Alex Kontoghiorghes

Do lower taxes lead to higher stock prices? Do companies consider tax rates when deciding on their dividend pay-outs and whether to issue new capital? If you’re thinking ‘yes’, you might be surprised to know that there was little real-world evidence (let alone UK-based evidence) which finds a strong link between personal investment tax rates on the one hand, and stock prices and the financial decisions of companies on the other. In this post, I summarise the findings from a recent study which shows that capital gains and dividend taxes do indeed have big effects on risk-adjusted equity returns, as well as the dividend, capital structure, and real investment decisions of companies.

Background

What drives stock returns? This is one of the oldest and most important questions in financial economics. While a lot of attention has been paid to the analysis of predictors such as company valuation ratios, market betas, momentum effects, and so on, in this blog post I advocate that taxes are an important and often overlooked predictor of stock returns.

I advocate this due to the findings of a unique natural experiment in the UK, which involved a lesser-known segment of fast-growing UK publicly listed companies, and which provided an ideal setting to study the effects of a very large tax cut. In summary, once Alternative Investment Market (AIM) companies were permitted to be held in tax-efficient Individual Savings Accounts (ISAs) for the first time in 2013, their prices became permanently higher than they would have been, their risk adjusted excess stock returns fell commensurately with the fall in their effective tax rates, dividend payments increased by a quarter, companies issued more equity and debt in response to their new lower cost of capital, and finally, companies used their newly issued capital to invest in their tangible assets and increase pay to their employees. Want to find out more? Keep reading.

Background and methodology

Around 10 years ago (July 2013 to be exact) the then Chancellor of the Exchequer George Osborne announced that stocks listed on the Alternative Investment Market (AIM), a sub-market of the London Stock Exchange, could from August 2013 onwards be held in a capital gains and dividend tax-exempt individual savings account (ISA) for the first time. This was a very important change for AIM-listed companies, and they had been calling for this equalisation of tax treatment for many years as stocks and shares ISAs hold billions of pounds of retail investors’ savings.

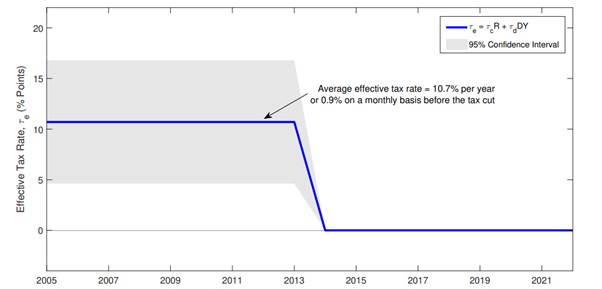

Since main market London Stock Exchange Stocks (such as the FTSE All-Share companies) were always eligible to be held in ISAs, this provided a unique natural experiment to study what happens to various company outcomes when their owners’ effective personal tax rate suddenly becomes zero. To see how big this tax cut was, Figure 1 shows that pretty much overnight, the effective AIM tax rate for retail investors (the amount of return percentage points paid out in tax, calculated as the sum of the stock’s capital gain and dividend yield components) went from around 10% per year to 0% after AIM stocks could be held in ISAs, a huge decrease in the world of personal taxation.

Figure 1: Average effective tax rate of AIM stocks before and after legislation change

The equivalent effective tax rate for main market stocks when held in ISAs during this period was always 0%, which is why they are used as the control group in this study.

Using a difference-in-differences approach with a matched London Stock Exchange control group, I investigate the effect of the tax cut on the equity cost of capital and company financial decisions. The matched control group is created using the following important characteristics: firm size, age, sector, book-to-market ratio, and market beta, to ensure that the results are less likely to be driven by unobservable AIM company-specific factors.

What I find

Relative to the control group, I find that AIM stock prices initially jumped as retail investors and retail-focused institutions increased their relative ownership after the legislation change. I also find that long-run pre-tax stock returns decreased by 0.9 percentage points per month to reflect their lower required rate of return (investors no longer required compensation for their tax liability). This amount is statistically equivalent to the monthly effective tax rate AIM companies faced before the change in legislation (0.9% x 12 ≈ 10%).

On the company side, I find that dividend payments increased by around a quarter to reflect the lower tax liability faced by their investors. Furthermore, in response to their lower cost of capital, AIM companies issued both more equity and debt. Finally, in-line with the ‘traditional view’ of corporate investment theory, AIM companies substantially increased their tangible assets (for example factories, warehouses, and machinery), and increased total pay to their employees. Regarding the external validity of these results, it is important to mention that AIM companies are generally smaller and faster growing than the average UK publicly listed company, and their relatively more concentrated ownership structure will also be a factor in their pay-out and investment decisions.

Implications for policymakers

These findings have important policy implications on a number of levels. My study revealed that changing the level of investment taxes is an effective tool to incentivise capital flows into certain assets. When similar assets have differing rates of investment taxes, this can cause substantial distortions to company valuations, as reflected by the large change in the annual returns of AIM listed companies. A lower cost of capital means companies have higher stock prices and can raise capital on more favourable terms.

My findings showed that equalising investment taxes between AIM and main market London Stock Exchange companies enabled a more efficient flow of capital to small, growing, and often financially constrained UK companies, and potentially allowed a more efficient flow of dividend capital to shareholders which was previously impeded due to higher rates of taxation.

Finally, my findings show that a permanently lower cost of capital incentivised AIM companies to issue more equity and debt post tax-cut, and companies used this new capital to invest in their tangible capital stock, and increase the total pay to their employees, which was a stated intended consequence of the legislation change.

Alex Kontoghiorghes works in the Bank’s Monetary and Financial Conditions Division.

If you want to get in touch, please email us at bankunderground@bankofengland.co.uk or leave a comment below.

Comments will only appear once approved by a moderator, and are only published where a full name is supplied. Bank Underground is a blog for Bank of England staff to share views that challenge – or support – prevailing policy orthodoxies. The views expressed here are those of the authors, and are not necessarily those of the Bank of England, or its policy committees.

Share the post “Another reason to care about investment taxes”

{kind=link}