Tim Willems and Rick van der Ploeg

Since the post-Covid rise in inflation has been accompanied by strong wage growth, interactions between wage and price-setters, each wishing to attain a certain markup, have regained prominence. In our recently published Staff Working Paper, we ask how monetary policy should be conducted amid, what has been referred to as, a ‘battle of the markups’. We find that countercyclicality in aspired price markups (‘sellers’ inflation’) calls for more dovish monetary policy. Empirically, we however find markups to be procyclical for most countries, in which case tighter monetary policy is the appropriate response to above-target inflation.

In a simplified setup where wages are firms’ only input cost, while consumers only buy domestically produced goods, the ‘battle of the markups’ takes an intuitive form (Rowthorn (1977)):

By itself, there is nothing guaranteeing that real-wage aspirations held by workers and firms are mutually consistent in this framework – ie, there is nothing to ensure that

Unemployment as an equilibrating device

Layard and Nickell (1986) argued that the moderating effect from the presence of unemployment acts like a clearing mechanism. They posed that aspired markups

Here, the structural component ‘

Similarly, price markups aspired by firms also consist of a structural component alongside a cyclically sensitive one:

When it comes to the cyclicality of price markups, it is debated whether they are pro or countercyclical. On the one hand, a slowdown makes firms afraid of having to carry large inventories or suffer from capacity underutilisation. This would imply that aspired price markups are procyclical (

In general, and irrespective of the sign of

It can be shown that the equilibrium level of unemployment increases in structural aspirations held by workers and firms (

The role of the central bank

The story so far assumes that, somehow, the unemployment rate ‘agrees’ to clear any conflict between firms and workers. In reality, it won’t automatically. There are many reasons for unemployment to exist, eg search frictions (Pissarides (2000)) or providing incentives to limit shirking (Shapiro and Stiglitz (1984)). This implies that the level of unemployment is not ‘free’ to clear any conflict and further action is required.

This is where the central bank comes in. Through its mandate, the central bank is tasked with setting policy to keep inflation at target. In our framework, this implies that the central bank will attempt to set its policy to ensure that cyclical conditions are such that markup aspirations are consistent with the size of national income. And if aspired markups are cyclically sensitive, there is an ‘aspirational channel’ of monetary policy transmission.

If aspired markups of both firms and workers are procyclical (

There is however debate over the sign of

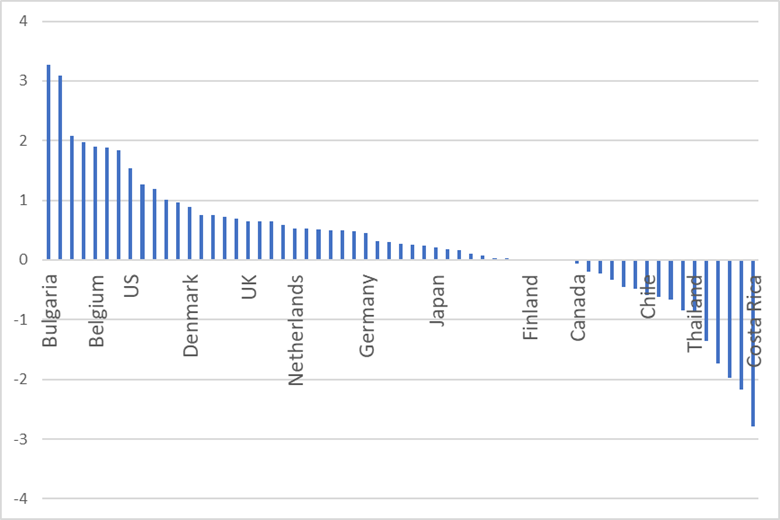

Consequently, it is important for central banks to know whether firms’ aspired markups are pro or countercyclical. We have estimated the cyclicality of the price markup (

Chart 1: Estimated degree of cyclicality in price markups (

Paying for imports

Recent UK experiences have been more involved than the stylised situation described thus far. Next to domestic workers and firms, foreign exporters also lay a claim on UK output – as output is partly produced with imports, like energy. As energy prices rose around Russia’s 2022 invasion of Ukraine, the UK’s terms-of-trade worsened and the share of national income flowing abroad suddenly went up – leaving less pie to be distributed domestically.

Absent any reduction in the structural components of markups aspired by firms and workers (

Indeed, central bankers appear to have an ‘aspirational’ transmission mechanism in mind as can be seen from Christine Lagarde (2023):

We need to ensure that firms absorb rising labour costs in margins (…) The economy can achieve disinflation overall while real wages recover some of their losses. But this hinges on our policy dampening demand for some time so that firms cannot continue to display the pricing behaviour we have recently seen (emphasis added).

Conclusions and policy implications

A monetary tightening is not the only way via which markup aspirations could be moderated. Faced with an adverse terms-of-trade shock, it is also possible that workers and/or firms internalise the implications (that there is less income to be divided domestically), inducing them to lower the structural components of their aspired markups (

Absent such a co-ordinated response, bringing inflation back to target following an adverse terms-of-trade shock may require a cyclical slowdown to moderate markups aspired by workers and firms. An important caveat is that this strategy might not work if firms’ aspired price markups are countercyclical, but we find no evidence for this in the UK. As a result, the monetary tightening implemented in recent years is likely to aid the disinflation process via our ‘aspirational channel’ (not present in most standard models, featuring acyclical desired markups), which facilitates inflation returning to target.

Tim Willems works in the Bank’s Structural Economics Division and Rick van der Ploeg is a Professor at the University of Oxford.

If you want to get in touch, please email us at bankunderground@bankofengland.co.uk or leave a comment below.

Comments will only appear once approved by a moderator, and are only published where a full name is supplied. Bank Underground is a blog for Bank of England staff to share views that challenge – or support – prevailing policy orthodoxies. The views expressed here are those of the authors, and are not necessarily those of the Bank of England, or its policy committees.

Share the post “Markup matters: monetary policy works through aspirations”

{kind=link}