With a plethora of interdependent and ever-changing parts, gaining a clear (or even not-terribly-fuzzy) understanding of where the economy stands at any given moment is a daunting task, to say the least. Even more difficult is using data based on samples and surveys (and subject to constant revision!) to develop some idea about which of the myriad possible outcomes might be more likely to occur. Yet, by taking a measured look at factors driving economic activity and influencing behavior, advisors can help clients face risks they can’t control and (hopefully) position themselves to take advantage of opportunities as they develop.

In this guest post, Larry Swedroe, Head of Financial and Economic Research at Buckingham Wealth Partners, reviews key aspects of economic activity in the 1st quarter of 2024, examines what the behaviors in the various financial markets might be suggesting about investor expectations, and offers insight into how advisors might help clients prepare moving forward.

As has been the case for the past several quarters, the prevailing characteristic of the economy is one of bifurcation, with interest rate-sensitive sectors remaining in a recession (as evidenced by the manufacturing sector’s 16-month-long contraction), while the services sector (which accounts for nearly 80% of U.S. GDP) continues to expand. Importantly, headline inflation has continued to trend lower, but with persistent upward pressure on wages in the services sector, a rebound in housing prices, and no relief in sight for skyrocketing auto insurance, home insurance, and home repairs (as well as trade-route disruptions arising from turmoil in the Red Sea), the Fed may have little choice but to keep rates elevated as they pursue their elusive 2% inflation target.

Meanwhile, a smorgasbord of potential risks threatens economic growth’s “soft landing” narrative. Notably, the work-from-home movement has resulted in a dramatic drop in office valuations that could lead to a whole host of issues, including lending constraints in the banking sector, which is already sitting on a mountain of unrealized losses on Treasuries and mortgages. Lower office valuations may also squeeze tax receipts in municipalities, particularly large cities that are already experiencing financial strains due to the surge in illegal immigration and the flight of high-income individuals and companies to states with lower taxes.

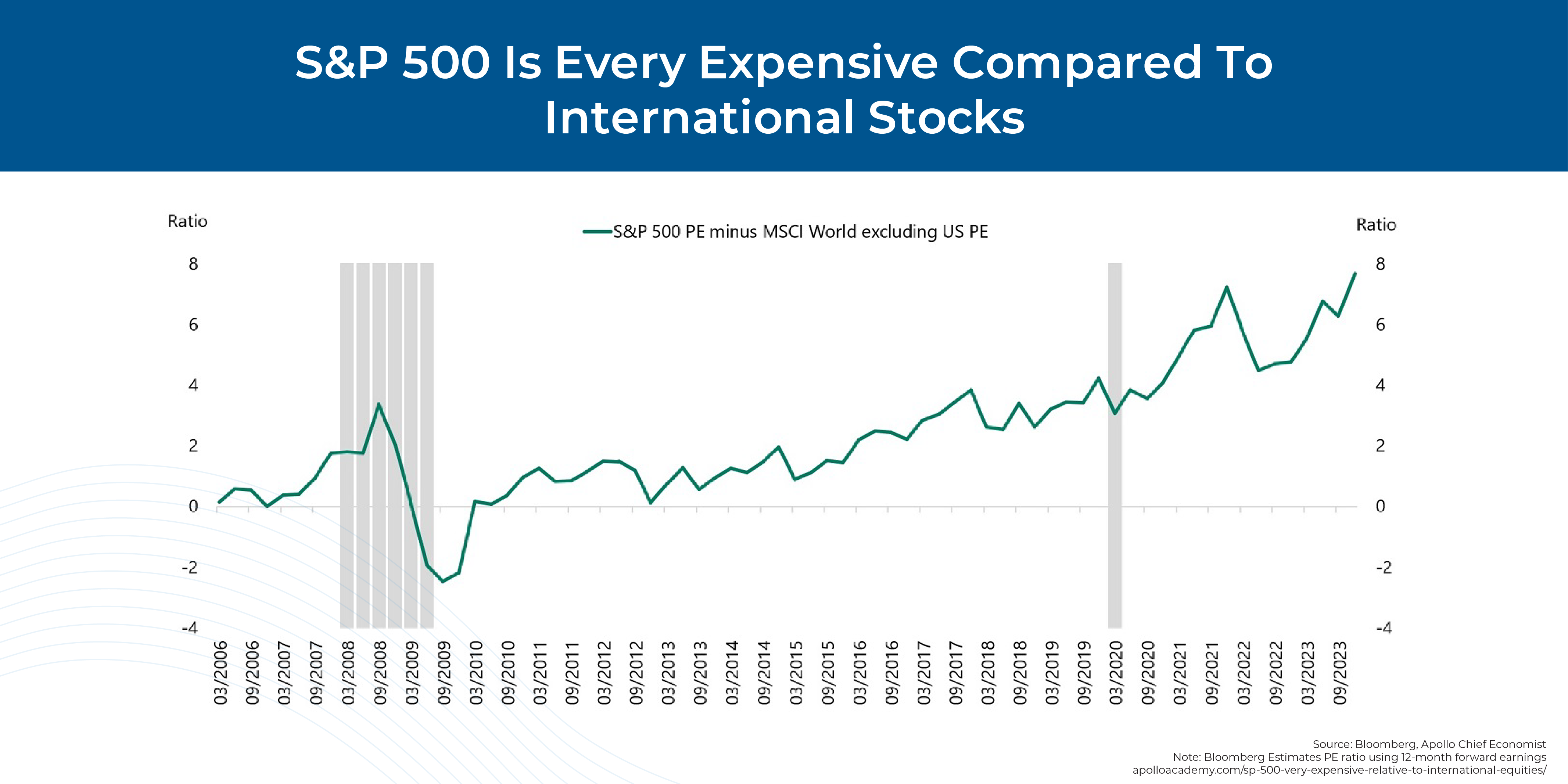

The equity market is experiencing its own bifurcation, with a wide dispersion in (extremely elevated) valuations across the “Magnificent 7” and the rest of the market, which is much closer to historical averages. At the same time, value and international stocks continue to lag, trading as if the economy is already in the depths of a serious recession. Looking forward, equity analysts predict earnings growth in 2024 of 11.5%, which stands in stark contrast to the Philly Fed’s Survey of Professional Forecasters expectations of total GDP growth of ‘just’ 3.8%. Given that corporate profits have historically tracked GDP growth, this inconsistency creates an interesting enigma.

Ultimately, the key point is that advisors can prepare clients for the possibility of increased volatility as the year develops, along with lower equity returns due to lower potential economic growth, high valuations in leading stocks, persistent inflation, higher-for-longer interest rates, and rising fiscal debt. Some strategies can include adjusting assumptions for future equity returns and increasing allocations to fixed-income assets that are less sensitive to inflation shocks (particularly shorter-term bonds with low credit risk, including TIPS and floating rate debt). Additionally, advisors may look to increase diversification with assets that have historically low correlation with economic cycles, including reinsurance, private lending, consumer credit, commodities, and long-short factor funds. The bottom line is that by assessing the broader economic landscape, advisors can help clients weather the potential risks on the horizon, position themselves to take advantage of possible opportunities, and (most importantly) remain focused on their long-term goals!

{kind=link}