Petronet LNG Ltd. – First LNG terminal in India

Incorporated in 1998 as a joint venture among GAIL, IOCL, BPCL & ONGC, Petronet LNG Ltd. (PLL) is currently one of the fastest growing world-class companies in the Indian energy sector. The company was formed to develop, design, construct, own and operate Liquefied Natural Gas (LNG) import and regasification terminals in India. PLL commenced its operations by setting up country’s first LNG receiving and regasification terminal at Dahej, Gujarat and another terminal later at Kochi, Kerala. As of 31 March 2023, the company with a combined capacity of 17.5 million metric tonnes per annum (MMTPA) of LNG account for around 33% gas supplies in the country and handle around 75% LNG imports in India.

Products and Services

PLL is an energy company that operates in the LNG sector of the natural gas industry. PLL’s main business activities includes Import of Liquefied Natural Gas (LNG) and sale of Regasified – LNG (RLNG) & Regasification/ Handling of LNG and ancillary services.

Subsidiaries: As of FY23, the company has 3 subsidiaries and 2 joint ventures.

Key Rationale

- Renewal of Qatar deal – The company recently renewed its long-standing deal with Qatar for additional 20 years from 2028 till 2048. The deals ensures steady supply of 7.5 MMTPA LNG from Qatar to India, bolstering the countries energy security. The 20-year deal is an extension of an existing contract for LNG supplies signed in 1999 which runs until 2028. The deal is considered to be of national significance ensuring a steady supply of regasified LNG to key sectors such as fertilisers, city gas distribution, refineries, petrochemicals, power and other industries.

- Expansion plans: To enhance the present LNG storage capacity of around 1 million CuM at Dahej terminal, construction of two additional LNG storage tanks of gross capacity of 1,85,000 CuM each has been taken up at a cost of approx. Rs.1,250 crore with a construction schedule of 36 months (September, 2024). The company is also undertaking a highly cost-effective brownfield expansion of regassification capacity of Dahej Terminal from 17.5 MMTPA to 22.5 MMTPA at an estimated cost of Rs. 600 crore.

- New business initiative – Diversifying its business lines, the company is undertaking a new petrochemical PDH/PP (propane dehydrogenation and polypropylene) plant including an ethane handling facility in Dahej terminal at an outlay of Rs.20,658 crore, expected to be commissioned in FY27-28. 250 KTA from the proposed 750 KTA capacity of the PDH plant has already been tied up with a customer for 15 years, extendable for another 5 years. Remaining 500 KTA propylene will be converted to PP. The management expects to deliver an IRR of 20% and equity IRR of 30%.

- Q3FY24 – During the quarters, the company revenue declined by 7% to Rs.14,747 crore as compared to the Rs.15,776 crore of Q3FY23. Profits improved marginally with operating profit increasing by 2% to Rs.1,705 crore and net profit increasing by 1% to Rs.1,191 crore. However, compared to the previous quarter (Q2FY24), revenue increased by 18%, operating profit improved by 40% and net profit surged by 46%. The quarter also reported highest ever PBT and PAT recorded in the 9-month period.

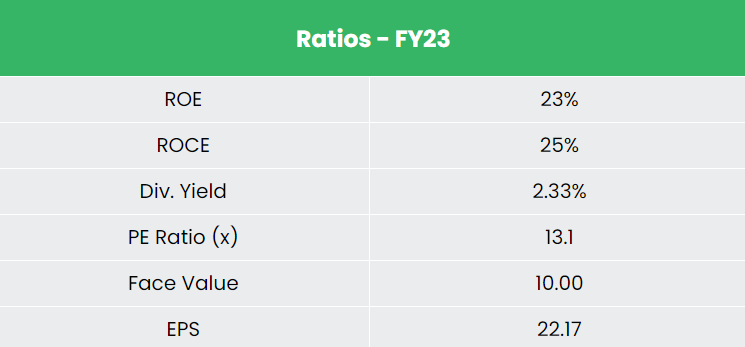

- Financial performance – The company has generated revenue and PAT CAGR of 19% and 6% over the period of 3 years (FY20-23). Average 3-year ROE & ROCE is around 25% and 28% for FY20-23 period. The company has robust capital structure with a debt-to-equity ratio of 0.20.

Industry

The oil and gas sector is among the eight core industries in India and plays a major role in influencing the decision-making for all the other important sections of the economy. Being the third largest consumer of energy and oil in the world India’s economic growth is closely related to its energy demand, therefore, the need for oil and gas is projected to increase, thereby making the sector quite conducive for investment. Natural Gas consumption is forecast to increase at a CAGR of 12.2% to 550 MCMPD by 2030 from 174 MCMPD in 2021. Notably, India is also the 4th largest importer of liquefied natural gas (LNG).

Growth Drivers

- Government of India has allowed 100% foreign direct investment (FDI) in many segments of the sector, including natural gas, petroleum products and refineries, among others.

- India has set a target to raise the share of natural gas in the energy mix to 15% by 2030 from about 6.7% now.

- A total of 88% of the nation’s geographical area covering 98% of the population has been authorized for the development of City Gas Distribution network.

Competitors: GAIL (India) Ltd, Gujarat Gas Ltd etc.

Peer Analysis

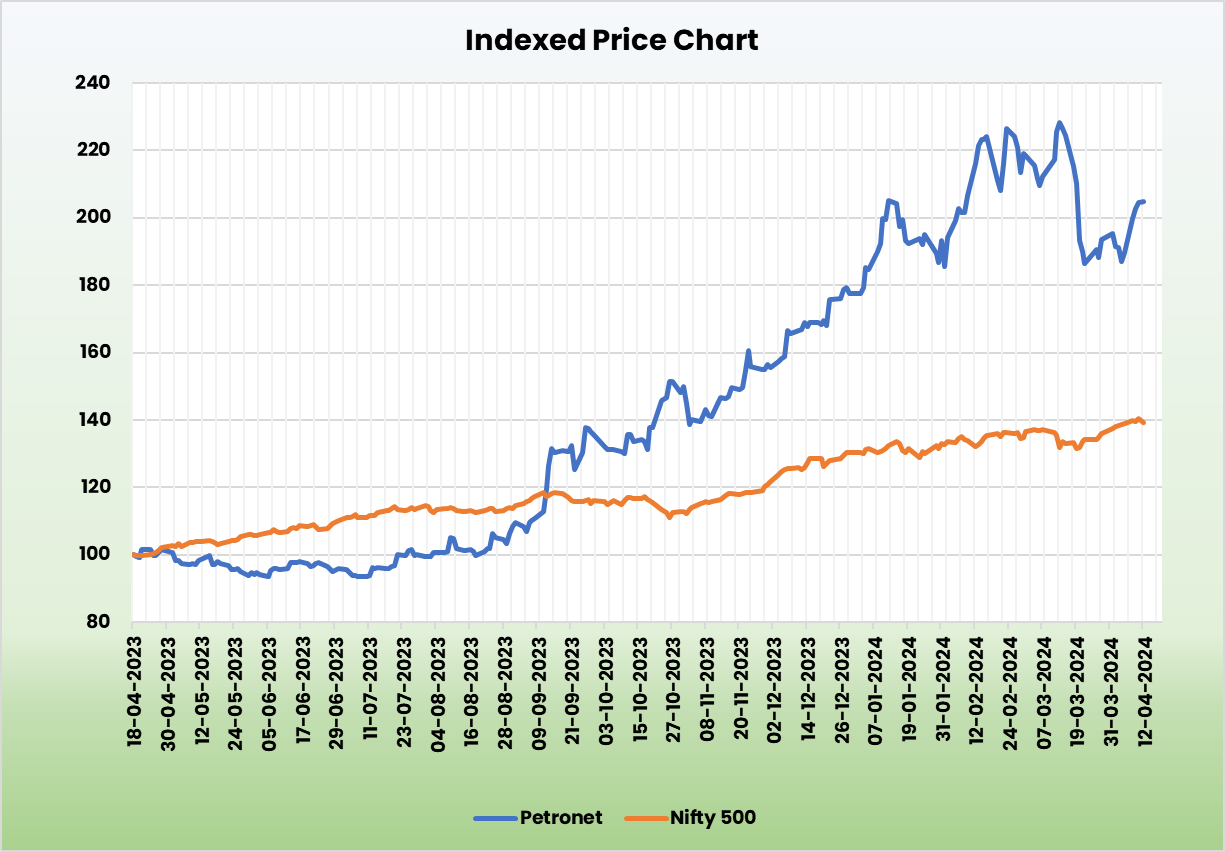

In comparison to the above competitors, PLL is the most undervalued stock with healthy returns on the capital employed and stable growth in sales.

Outlook

The company is well placed to gain from the government’s push for energy efficiency from natural gas. Currently Dahej terminal is utilised at 96% capacity and the plans to extend capacity to 22.5 MMTPA by March 2025 is expected to give further turnover for the company. The company also has other value added services in pipeline such as pipeline connectivity from Coimbatore to Krishnagiri pending completion by year-end, terminal in Gopalpur, etc. However, the entry into non-core petchem business where existing petchem companies are already struggling to make reasonable returns could be margin dilutive to the company.

Valuation

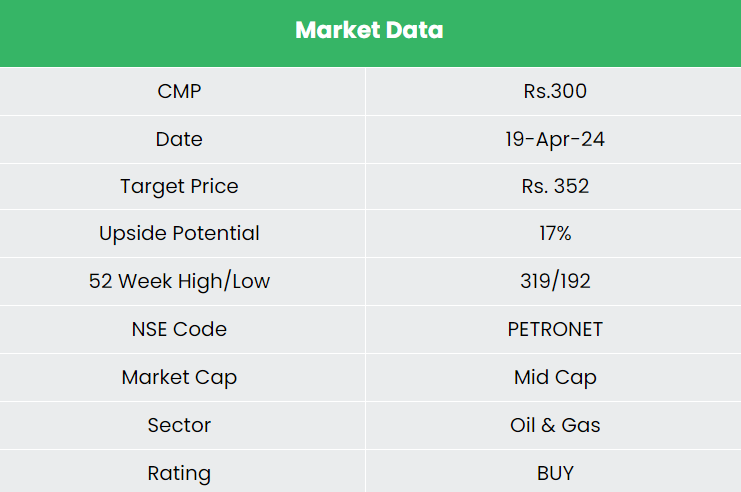

We believe Petronet LNG Ltd. is well positioned to benefit from the tremendous potential that India has to offer for the exponential growth in energy consumption. We recommend a BUY rating in the stock with the target price (TP) of Rs.352 14x FY25E EPS.

Risks

- Geopolitical disturbances – Geopolitical risks such as war outbreaks, government instability or any other social unrest of the like may result in acute supply chain disruption thereby impacting the company’s operations.

- Capital misallocation risk – Capex plans into non-core petchem business could stress the company’s capital allocation and balance sheet. The company expects to fund the project through a debt: equity mix of 70:30 to optimise its capital structure and continue with the existing level of dividend payout. Petchem investment needs very high margins to meet management targets of profitability.

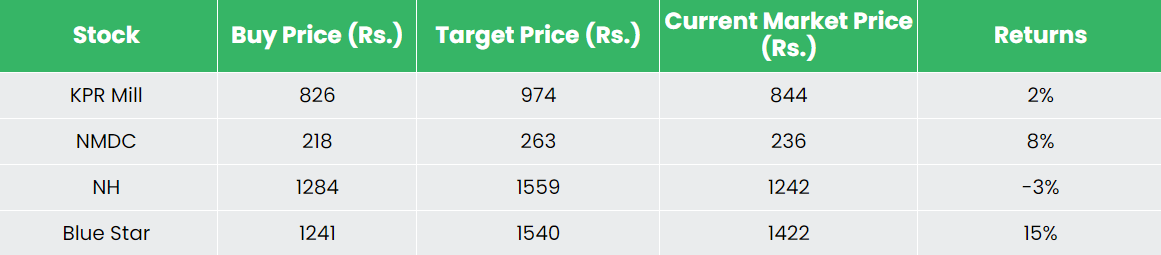

Recap of our previous recommendations (As on 19 Apr 2024)

Other articles you may like

Post Views:

70

{kind=link}