Over the past few decades, advicers have used Monte Carlo analysis tools to communicate to clients if their assets and planned level of spending were sufficient for them to realize their goals while (critically) not running out of money in retirement. More recently, however, the Monte Carlo “probability of success/failure” framing has attracted some criticism, as it can potentially alter the way that a client perceives risk, leading them to make less-than-ideal decisions. In reality, retirees rarely experience true failure, and instead find that they may need to adjust their spending (in both directions!) in order to meet all of their goals. And while some have suggested pivoting to a more accurate “probability of adjustment” framing, there is a simpler way to talk about “retirement income risk” that relies on the concepts of overspending and underspending, which can help both advicer and client better understand the trade-offs inherent in the ongoing decisions around spending in retirement.

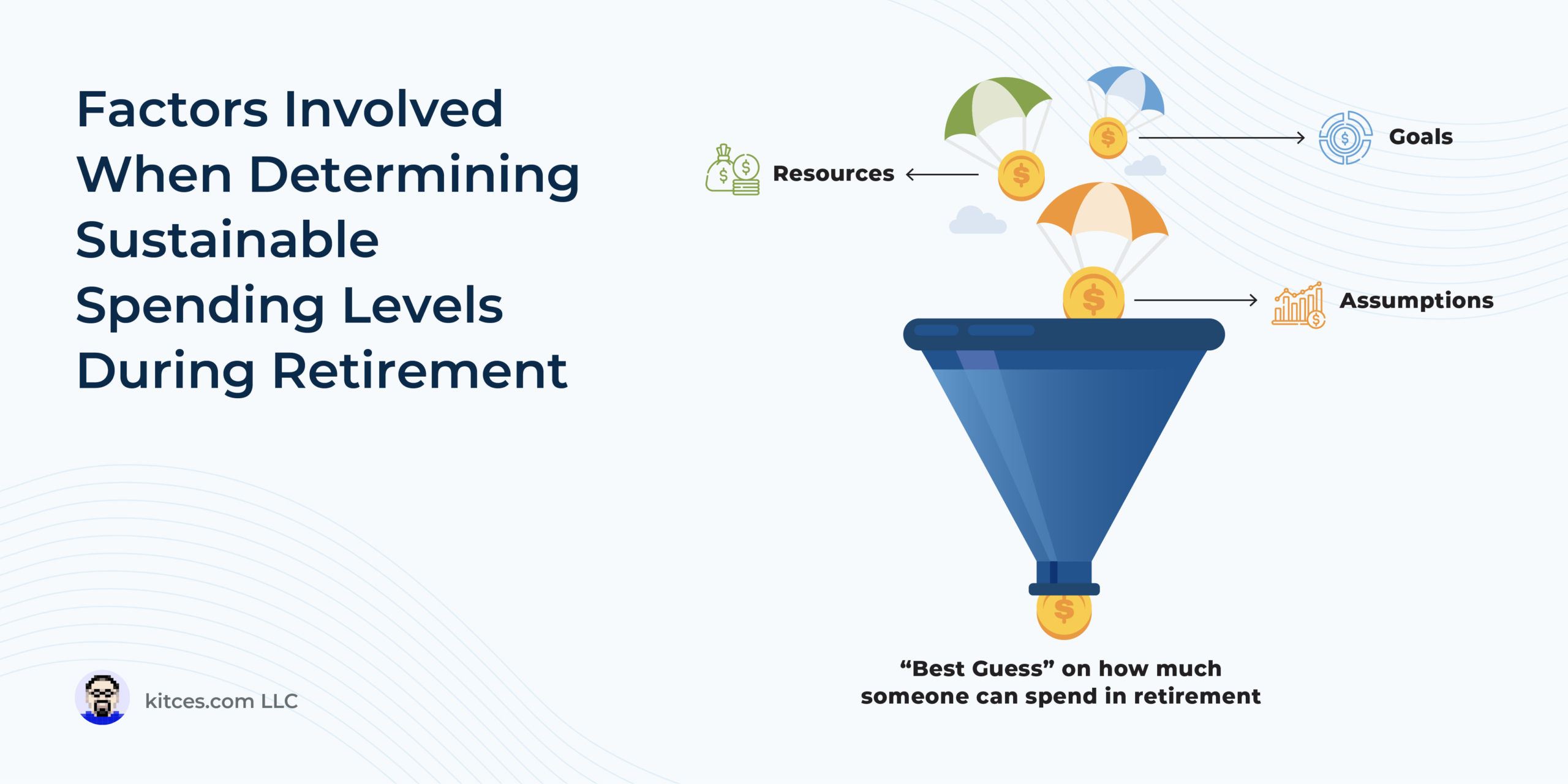

Determining whether clients are overspending or underspending during their working years is relatively straightforward and is simply a matter of observing if they are spending more or spending less than they make. However, once the client retires, the “how much they make” part of the equation becomes much less clear. But by accounting for all of a client’s income sources and balancing them against their various spending goals with a set of future assumptions around such factors as life expectancy and market performance, the advicer can arrive at a “best guess” answer to the question of how much the client should be spending. From a mathematical standpoint, that best guess is the level at which a client is equally likely to overspend as they are to underspend. Yet, in the Monte Carlo success/failure framework, that balance point exactly represents a 50% probability of success, which seems intuitively ‘wrong’ given that the analysis targeted the precise spending level that would preclude both overspending and underspending!

The Monte Carlo success/failure framing, in essence, focuses only on minimizing the risk of overspending, hiding a bias towards underspending by calling it a “success”. Or, put another way, a 100% probability of success is exactly a 100% probability of underspending. Which means that solving for higher probabilities of success generally necessitates underspending to the point where clients, while comfortable knowing that they almost certainly won’t run out of money, may have to significantly revise their desired expectations for their standard of living. By contrast, the overspending/underspending framework allows advicers to mitigate the Monte Carlo bias toward underspending while using concepts that clients are already familiar with. For instance, an advicer might communicate that their job is to help the client find a spending level that balances their goals of living the life they want while not depleting their resources.

Helping a client determine a balanced spending level in retirement is only the beginning of the journey. As time goes on, odds are that various factors (including circumstances, expectations, market returns, and inflation, to name just a few) will require spending levels to be adjusted. And by relying on the overspending/underspending framework, advicers can communicate how clients will be able to make those adjustments over time and, in the process, minimize the biases that incentivize lower spending that ultimately prevent them from living their lives to the fullest!

{kind=link}