NTPC Ltd. – Leading India’s Power Sector

Established in 1975 and headquartered in New Delhi, NTPC Ltd. is an Indian Public Sector Undertaking (PSU) primarily involved in the generation and sale of bulk power. It is a vertically integrated company overseeing the entire process of power generation and distribution. As of FY24, NTPC boasts an installed capacity of 75,958 MW (including JVs) and aims to become a 130 GW company by 2032. The company’s energy portfolio includes 35 coal, 11 gas/naphtha, 29 solar, 11 hydro, and 3 wind-based power plants. Notably, four of its coal stations ranked among the top 10 performing stations in the country in terms of Plant Load Factor (PLF) in FY24.

NTPC’s Product Portfolio:

Business verticals of NTPC are power generation (thermal, renewable including solar & wind, hydro, and nuclear), green hydrogen and chemicals, mining, waste to energy, energy trading, consultancy services, EV ecosystem, and ash management.

How many Subsidiaries does NTPC have?

As of FY24, NTPC has 10 subsidiaries and 16 joint venture companies, enhancing its operational scope and market reach.

NTPC Growth Strategies

Capacity Expansion:

- Expanded commercial capacity by 3924 MW in FY24.

- Increased captive coal production by 48% from 23.20 MMT in FY23 to 34.39 MMT in FY24.

- Plans to award an additional 15.2 GW of thermal capacity and boost coal mining capacity to 50 million tonnes annually within three years.

Strategic Growth Plans:

- NTPC Green Energy Limited (NGEL) partnerships for Green Hydrogen initiatives in Gujarat.

- MoU with Gujarat Pipavav Port Ltd. for Green Ammonia production and offshore wind farm exploration.

- Power Purchase Agreement with Damodar Valley Corporation for 310 MW solar projects.

Renewable Energy:

- Aiming for 45-50% capacity from non-fossil fuels by 2030.

- Commissioned 3.6 GW of renewable energy projects with an additional 8.4 GW under construction and 11.2 GW in the tendering process.

- MoU with the Government of Maharashtra for green hydrogen, pump hydro, and renewable energy projects.

Financial Report of NTPC:

Q4FY24:

- Revenue: Rs.47,622 crore, an 8% increase from Q3FY23.

- EBITDA: Rs.13,984 crore, a 17% increase from Q3FY23.

- Net Profit: Rs.6,490 crore, a 33% YoY increase.

- EBITDA margin at 29% and net profit margin at 14%.

FY24:

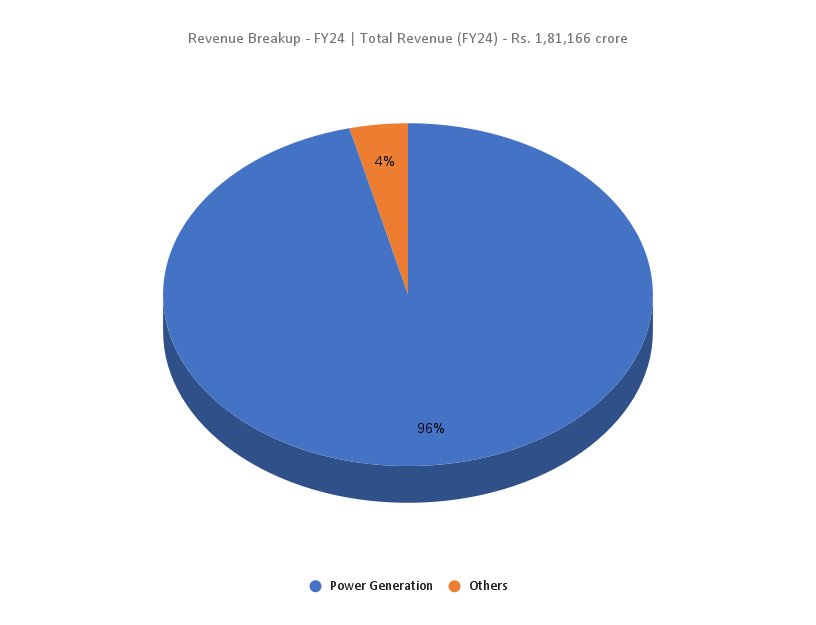

- Revenue: Rs.1,81,166 crore, a 2% YoY increase.

- Operating Profit: Rs.51,093 crore, a 7% YoY increase.

- Net Profit: Rs.21,332 crore, a 25% YoY increase.

- Generated 422 Billion Units, up 6% from FY23.

- Average PLF of NTPC coal stations at 77.25%, 8% above the national average.

Financial Performance:

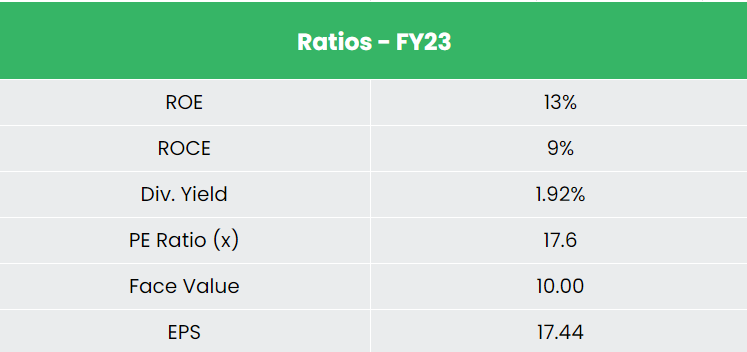

- Revenue and PAT CAGR of 17% and 9% over FY21-24.

- Average 3-year ROE & ROCE at around 13% and 10%, respectively.

Industry Outlook:

- Diverse Power Sector: India’s power sector includes coal, lignite, natural gas, oil, hydro, nuclear, wind, solar, agricultural, and domestic waste sources.

- Future Growth: Projected power requirement of 817 GW by 2030.

- Renewable Energy Expansion: CEA estimates an increase in renewable energy generation share from 18% to 44% by 2030.

- Thermal Energy Reduction: Expected decrease in thermal energy share from 78% to 52% by 2030.

- Government Initiatives: Plans to establish a renewable energy capacity of 500 GW by 2030.

Growth Drivers:

- Increasing Electrification: Growing population and per-capita usage.

- Government Support: Significant budget allocation for green hydrogen, solar power, and green-energy corridors.

- FDI: 100% Foreign Direct Investment in the power sector, attracting US$ 18.17 billion from April 2000 to December 2023.

Comparison with NTPC’s Competitors:

Among competitors like Tata Power and Power Grid Corporation, NTPC stands out as the most undervalued stock with stable returns on capital and healthy revenue growth.

Outlook:

- Thermal Capacity Expansion: Plans to award 15.2 GW thermal capacity by FY26.

- Renewable Energy Targets: 60 GW by 2032.

- Capex Plans: Rs.35,000 to Rs.50,000 crore over the next 2-3 years.

- Sustained Demand: Benefits from consistent electricity demand.

- Government Backing: Provides sustained revenue visibility for medium to long term.

- Futuristic Plans: Focus on renewable energy and strategic partnerships.

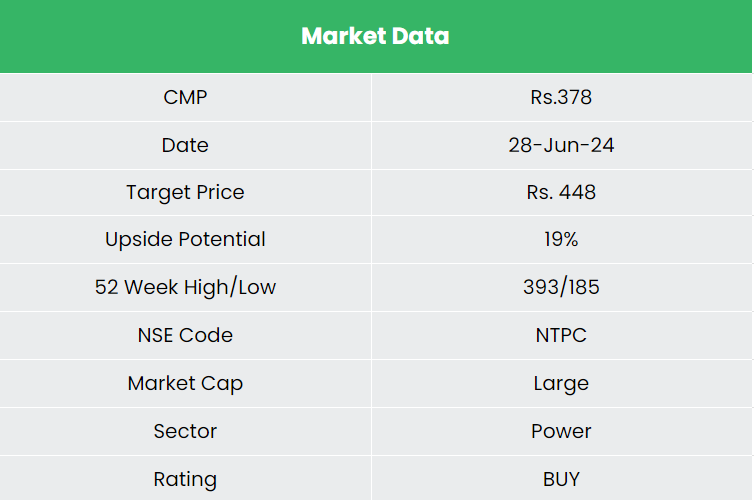

Valuation:

We recommend a BUY rating for NTPC Ltd., with a target price of Rs.448, based on 17x FY26E EPS, reflecting its growth potential and strategic initiatives.

Risks:

- Financial Risk: High dependence on debt for expansion projects.

- Execution Delay: Potential delays in thermal and renewable energy projects impacting turnover.

Note: Please note that this is not a recommendation and is intended only for educational purposes. So, kindly consult your financial advisor before investing.

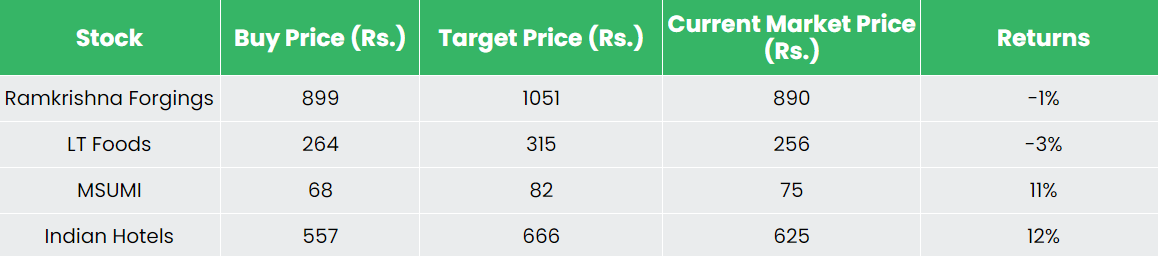

Recap of our previous recommendations (As on 28 June 2024)

Motherson Sumi Wiring India Ltd

Other articles you may like

Post Views:

84

{kind=link}