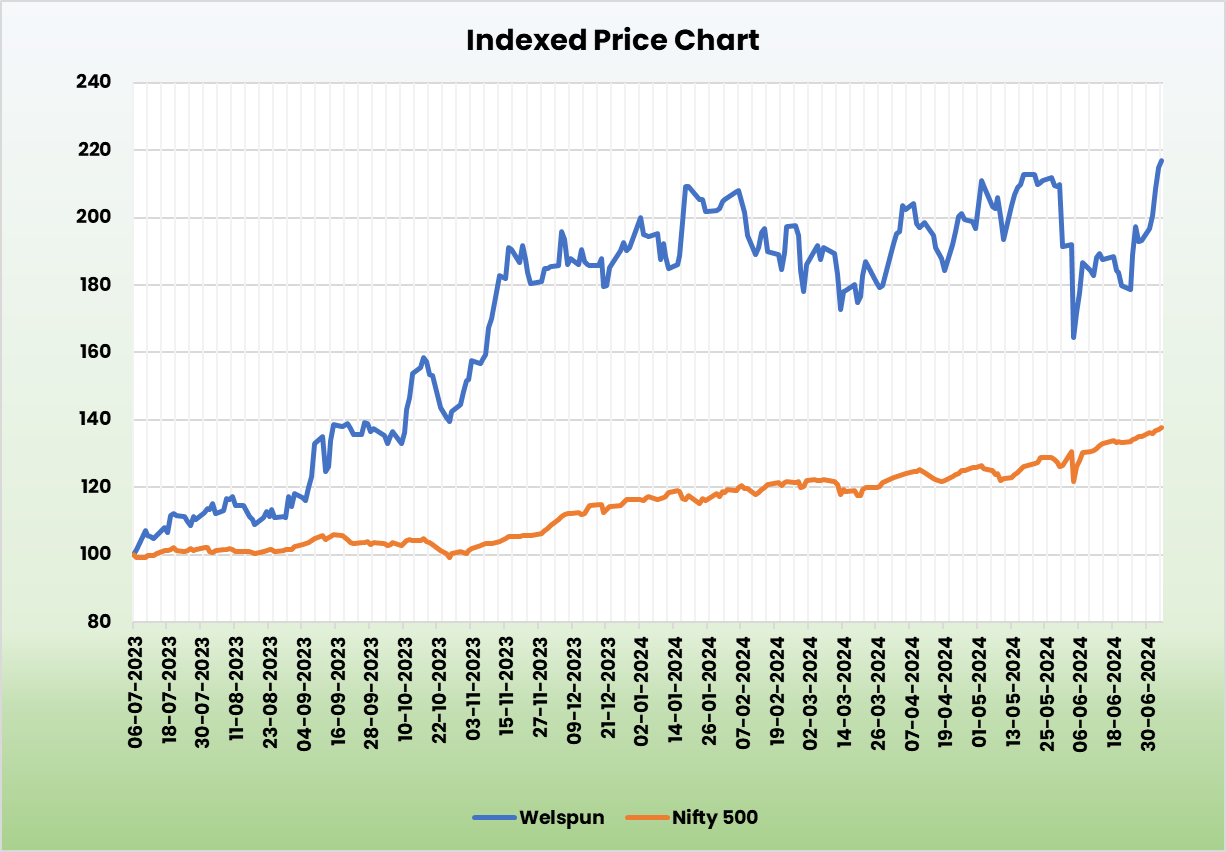

Welspun Corp Ltd. – Leader in Line Pipes

Incorporated in 1995, Welspun Corp Ltd. (WCL) is a market leader in line pipes and operates in various sectors including infrastructure, building materials, warehousing, retail, advanced textiles, home solutions, and flooring. As the flagship of the Welspun Group, WCL is among the world’s largest manufacturers of large diameter pipes, serving clients across 6 continents and 50 countries with tailored onshore and offshore solutions. The company boasts 5 state-of-the-art manufacturing facilities in Gujarat, Madhya Pradesh, Karnataka, and the USA.

Products and Services

- Carbon Steel Line Pipes: Welspun offers SAWL, SAWH, and HFW pipes, and ductile iron pipes for water infrastructure needs.

- Industrial and Construction Materials: The lineup includes TMT rebars (8mm to 32mm), pig iron, stainless steel, and alloy products for automotive, energy, defense, nuclear power, and aerospace industries.

- Home Solutions: Welspun provides water tanks and uPVC interiors for home applications.

Subsidiaries: As of FY23, the company has 15 subsidiaries, 1 joint venture, and 2 associate companies.

Growth Strategies

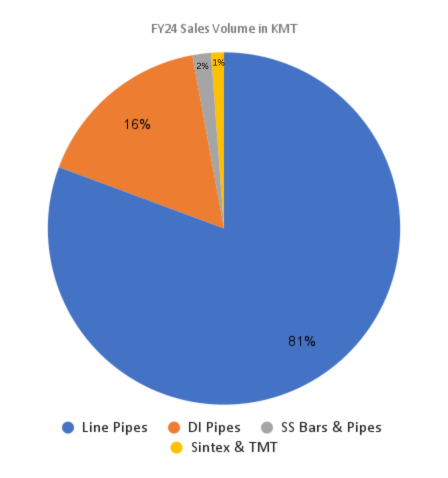

- Line Pipes Growth: Driven by government-backed oil, gas, and water distribution schemes, Welspun saw a 49% YoY volume increase, selling 9,80,000 tons in FY24. It leads the US market with a 20%-25% share and has orders confirmed until Q3FY25.

- Major Projects: Executed a key Permian pipeline order, with 2-3 more expected. Exploring a new line of plastic pipes.

- Strategic Acquisition: Acquired Sintex’s plastic products business in FY23, enhancing market presence through its vast distribution network.

- Diversified Portfolio: Includes home textiles, advanced textiles, flooring, retail, infrastructure, DI pipes, stainless steel pipes, pig iron, and TMT rebars. Qualified by BHEL and NTPC for supercritical boiler tube grades.

Operational Performance

Q4FY24

- Revenue: Rs. 4,544 crore, up 10% from Rs. 4,132 crore in Q4FY23.

- EBITDA: Rs. 413 crore, down 14% from Rs. 483 crore in Q4FY23, due to product mix and US operations.

- Profit After Tax: Rs. 268 crore, up 14% from Rs. 236 crore in Q4FY23.

FY24

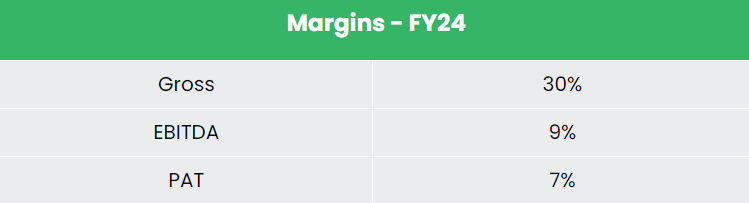

- Revenue: Rs. 17,582 crore, up 74% from Rs. 10,078 crore in FY23.

- EBITDA: Rs. 1,804 crore, up 124% from Rs. 805 crore in FY23.

- Net Profit: Rs. 1,110 crore, up 436% YoY.

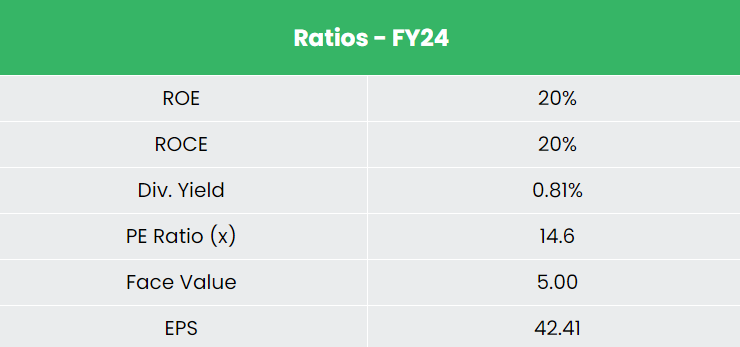

- ROCE: Improved by 1200 bps to 20%.

- Debt Reduction: Reduced by 66% to Rs. 387 crore from Rs. 1,138 crore in FY23.

Financial Performance (FY21-24)

- Revenue and PAT Growth: Achieved a CAGR of 34% and 21% respectively over the period FY 21-24.

- ROE & ROCE: Average 3-year Return on Equity (ROE) is around 12%, and Return on Capital Employed (ROCE) is approximately 14% for FY 21-24.

- Capital Structure: Maintains a robust capital structure with a debt-to-equity ratio of 0.35.

Industry outlook

- Energy Demand: India ranks third globally in energy and oil consumption. Projections indicate a 40% surge in oil demand to 6.7 million barrels per day (mb/day) by 2030, rising to 8.3 mb/day by 2050.

- Gas Pipeline Infrastructure: The government is enhancing the gas pipeline network to efficiently transport natural gas, connecting sources to consumer markets. Expansion of this grid is crucial for expanding the gas market.

- Upcoming Projects: Projects like the Kochi–Koottanad–Bangalore–Mangalore Phase II pipeline, set to launch in 2025, highlight ongoing infrastructure developments aimed at supporting economic growth.

- Government Support: Significant investments in infrastructure are supported by the government’s goal of achieving a US$ 5 trillion economy, with a strong emphasis on water distribution for household and irrigation purposes, alongside broader infrastructure development.

Growth Drivers

- National Gas Grid: Government initiative to ensure widespread distribution of natural gas across India.

- Ministry of Jal Shakti: Aimed at providing tap water connections to all households.

- National Perspective Plan (NPP): Designed to interlink rivers, increasing water availability for domestic, industrial use, and irrigation.

Competitive Advantage

Compared to competitors like APL Apollo Tubes Ltd, Shyam Metalics & Energy Ltd,etc.

Welspun growth is the most undervalued stock generating stable returns on capital employed and better earnings from the sales generated.

Outlook

- Financial Targets for FY25: Welspun aims for a Rs. 17,000 crore topline, Rs. 1,700 crore EBITDA, and 20% ROCE.

- Strategic Focus on DI Pipes: Supporting India’s water access goals with substantial DI pipes orders and capacity expansion.

- Emerging Opportunities: Expanding into hydrogen, carbon capture, and ammonia transmission pipelines.

- Market Expansion: Strong growth expected in Saudi Arabia’s oil, gas, and water sectors, with significant new projects.

Valuation

Welspun Corp Ltd’s robust position in the pipeline business, strong US market presence, continuous growth in Saudi Arabia, and expanding opportunities in DI pipes and Sintex provide strong growth prospects for the company. Based on these factors, we recommend a BUY rating on Welspun Corp Ltd with a target price (TP) of Rs. 723, reflecting 17x FY26E EPS.

Risks

- Forex Risk: Significant operations in foreign markets expose the company to forex fluctuations, potentially impacting financial results.

- Socio-economic Risk: Socio-economic instability can lead to increased input costs (e.g., raw materials, freight), potentially affecting margins and profitability.

Note: Please note that this is not a recommendation and is intended only for educational purposes. So, kindly consult your financial advisor before investing.

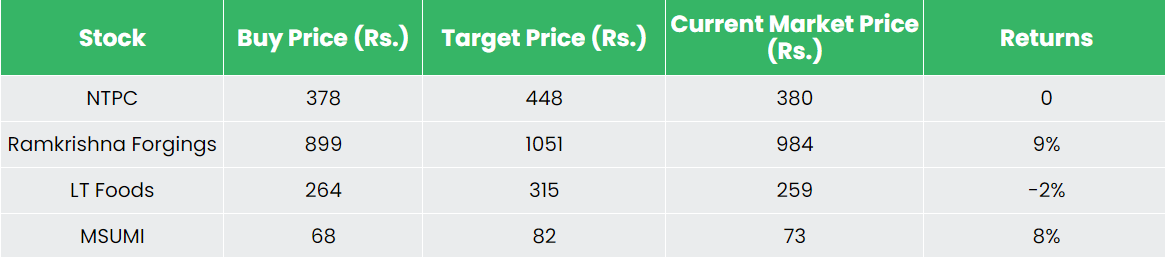

Recap of our previous recommendations (As on 05 July 2024)

Motherson Sumi Wiring India Ltd

Other articles you may like

Post Views:

121

{kind=link}