Vanessa lives in Eugene, Oregon with her boyfriend and three cats, Freya, Orpheus and Gandalf. Vanessa works as the Licensing & Contracts Officer for the University of Oregon and is an attorney by training. In 2018, she bought her first home and is now facing the prospect of some pricey renovations or the possibility of selling this home and buying a different place. She and her boyfriend are also in the process of discerning whether or not they want to stay together for the long-term, which will understandably impact her finances. We’re off to the Pacific Northwest today to help Vanessa sort through these possible life changes.

What’s a Reader Case Study?

Case Studies address financial and life dilemmas that readers of Frugalwoods send in requesting advice. Then, we (that’d be me and YOU, dear reader) read through their situation and provide advice, encouragement, insight and feedback in the comments section.

For an example, check out the last case study. Case Studies are updated by participants (at the end of the post) several months after the Case is featured. Visit this page for links to all updated Case Studies.

The Goal Of Reader Case Studies

Reader Case Studies intend to highlight a diverse range of financial situations, ages, ethnicities, locations, goals, careers, incomes, family compositions and more!

The Case Study series began in 2016 and, to date, there’ve been 77 Case Studies. I’ve featured folks with annual incomes ranging from $17k to $200k+ and net worths ranging from -$300k to $2.9M+.

I’ve featured single, married, partnered, divorced, child-filled and child-free households. I’ve featured gay, straight, queer, bisexual and polyamorous people. I’ve featured women, non-binary folks and men. I’ve featured transgender and cisgender people. I’ve had cat people and dog people. I’ve featured folks from the US, Australia, Canada, England, South Africa, Spain, Finland, Germany and France. I’ve featured people with PhDs and people with high school diplomas. I’ve featured people in their early 20’s and people in their late 60’s. I’ve featured folks who live on farms and folks who live in New York City.

The goal is diversity and only YOU can help me achieve that by emailing me your story! If you haven’t seen your circumstances reflected in a Case Study, I encourage you to apply to be a Case Study participant by emailing your brief story to me at mrs@frugalwoods.com.

Reader Case Study Guidelines

I probably don’t need to say the following because you folks are the kindest, most polite commenters on the internet, but please note that Frugalwoods is a judgement-free zone where we endeavor to help one another, not condemn.

There’s no room for rudeness here. The goal is to create a supportive environment where we all acknowledge we’re human, we’re flawed, but we choose to be here together, workshopping our money and our lives with positive, proactive suggestions and ideas.

A disclaimer that I am not a trained financial professional and I encourage people not to make serious financial decisions based solely on what one person on the internet advises.

I encourage everyone to do their own research to determine the best course of action for their finances. I am not a financial advisor and I am not your financial advisor.

With that I’ll let Vanessa, today’s Case Study subject, take it from here!

Vanessa’s Story

Foster kittens

Hi Frugalwoods, my name is Vanessa! I’m 37 and currently live with my boyfriend, age 36, and three cats–Freya, Orpheus, and Gandalf–in Eugene, OR. I work as the Licensing & Contracts Officer for the University of Oregon. I am an attorney and use a lot of my legal training in my job but am not an attorney on behalf of the university–the university’s technology transfer office handles many of the intellectual property matters for the University in its research administration office.

Vanessa’s Career

In college, I studied science and thought I would be a research scientist, but a quarter-life crisis took me from science to law (thinking I would go into patent law, which requires a science/technical background). I was in private practice for a few years, but a couple of bad firm partners and a third-of-life crisis led me to technology transfer. So I’m still in the legal and scientific fields, but working for an educational institution. That choice brought me to Eugene and my current position where I’ve been for about five years. I also have a side hustle as an IP consultant and I donate plasma for additional income.

Settled in Eugene, Oregon

Travel Picture-Eiffel Tower

After spending my 20’s moving and reinventing myself and my career, I’m very happy being settled in Eugene. I bought my house in September 2018 and started developing roots. I don’t intend to move again unless my circumstances drastically change (e.g., it is for the job of my dreams, I become destitute and have to move in with my mom, etc.). I love to garden and one of the reasons I bought my house is that it has a large area to garden. My grandmother taught me to sew block quilts and I am slowly teaching myself how to sew more intricate patterns.

I also inadvertently got involved in cat rescue this past fall when my boyfriend found a feral mama cat and her litter. I helped foster and get those kittens adopted and would like to work more in spay/neuter and Trap-Neuter-Release (TNR) programs to help prevent and reduce the cat population in my area.

Getting involved in cat rescue made me realize that a lot of people who work in TNR are spending their own money out-of-pocket to provide these services. Unfortunately, our local county shelter shut down its TNR program with the start of the pandemic and the rescue I previously worked with focuses more on rescue/adoption. I’ve considered establishing a non-profit to allow these volunteers an opportunity to at least receive a tax deduction for their expenses.

What feels most pressing right now? What brings you to submit a Case Study?

My life is in a transition stage!

#1: The most significant thing is that I believe my boyfriend and I will be breaking up soon.

Bounty of the Garden!

We’ve been together for about four years and are facing a lot of challenges about whether or not our lives and values are really compatible. We are on a probationary period until May when we will decide, but I don’t think we will be able to work out the issues we have. My boyfriend is a non-traditional student who went back for his degree in 2019. He is neurodivergent and it took him three years to get his Associates, and it will likely take him a similar amount of time for his Bachelor’s.

Financially, he contributes $500 each month towards the mortgage and bills (I bought the house and the mortgage is in my name only); we split some of the house expenses, like food and pet expenses at approximately 50%, but most of the other household expenses (e.g., chimney cleaning, stump removal, etc.) I pay for myself. I am not completely sure how the loss of that $500 will affect my overall budget or if costs will proportionally go down.

#2: About a month ago, I was the victim of a hit-and-run.

Beginning garden rows

The other driver left his bumper and license, so my insurance and the police were able to locate him. My car (a paid-off 2010 Honda Civic) was considered a total loss. My car was an awesome car, and I thought I would drive her until she died from natural causes. Of course, this all happened during what may possibly be the worst time in history to buy a car. I went to the most reputable used car dealer I could find, but the cars I test drove for the amount I could get from my car settlement were questionable (over 150+ miles, over a decade old, some with broken parts).

I next turned to buying a pre-certified used car (like my old car), but those were $20K+ to buy a similar car in terms of years old/milage. I ultimately decided to buy a new 2021 Volkswagen Jetta. For a few thousand more, I have more peace of mind with the warranties and quality of the car. It was a huge splurge for me and a weight on my mind and soul. Please no commentary about the wisdom of this choice–I truly believe that despite the cost, this was the best decision for me in this whackadoodle market. This was all two days after I bought my first matching bedroom set and upgraded to a queen mattress. I bought the floor samples at a discount and I love the set. The payments are at 0% for 12 months and I am using my tax refund but still paying over the 12 months. Between the car and the furniture, this will be the first time in years I’ve had debt.

#3: Finally, my original reason for my applying is for advice about my house. Should I remodel or sell it and buy a different house?

Wallpaper and faux woodpaneling of room to bring up to permit or remodel

My house has an upstairs room (about 15ft x 25 ft) that looks straight out of the 70’s with faux wood paneling, colonial American-style wallpaper, ceiling panel tiles, and fluorescent lighting. I bought the house knowing I would at least freshen up this room, however, it is now evident that the staircase is not safe. The stairs lead up to a half landing where the only attic access is located. It is very difficult to get in and out of attic on the half landing. It also seems like the steps on the stairs may be uneven. Both my boyfriend and I have fallen (not seriously), but I would like to get the stairs redone and placed on a different side of the room. I started to collect bids for the remodel and was told by contractors that they think the work to put in the upstairs room was un-permitted. I did a permit search with the city, and there is no permit on file (although that’s not an absolute guarantee the work was un-permitted).

When I bought the house, no one–not my realtor, the seller/realtor, or the home inspector–said anything about un-permitted work. Of the contractors I’ve had look at the job: one ghosted me without a bid, one wanted to do “exploratory construction” to see what was happening, and one said his company didn’t want the work but his best guess was that to get the work up to code would be $100k-$150k and suggested a smaller construction company might be willing to do the work for less. I don’t know if that amount includes a premium (I know there is a lot of work for construction companies now), but I know materials have gone up significantly in the pandemic, and there were a lot of wildfires in my area in September 2020, which destroyed many homes, meaning construction companies are in high demand right now.

True heinousness of the wallpaper

The alternative to investing so much into this house (really at least half the amount of the mortgage) is to sell the house and get another one.

This question is less pressing right now, especially because of the car situation, and because everything is so much expensive right now; my own equity has gone up over 50% since I bought. I feel that whichever path I choose–remodeling or selling/buying–will be better done in a few years. I am very sentimental about my house because it is my first home and I have already put a lot of sweat equity into this house. There are also some unique features about this house that I like including significant garden space and a hot tub (came with the house), which I don’t know if I could get in a different house. I also don’t want to trade one set of problems for another in a different house.

What’s the best part of your current lifestyle/routine?

Attic entrance and half landing

What I love most about my current lifestyle is its regularity and consistency. Moving around in my 20’s made me lonely and isolated. Starting from scratch every year or two left me very vulnerable and sad. Being in Eugene has allowed me to grow friendships and community and let me start exploring hobbies like gardening and sewing that I couldn’t do before. I also believe it is very important to donate and volunteer for charity and it’s only with the stability of my current lifestyle that I’ve been able to start doing this.

What’s the worst part of your current lifestyle/routine?

The worst part of my current lifestyle is the anxiety about the future, especially with regard to my boyfriend. Additionally, while my job is super secure, there is absolutely a ceiling to advancement; my group is a small one (six people), so there isn’t room for job growth and development unless someone leaves, which is unlikely. I am getting burned out on this job because it is no longer challenging or interesting. I’m good at it, just bored. Eugene and its sister city Springfield are a medium-ish market, and I don’t know if I’d be able to find another job that pays as well as my current position. If I ever had to find a new job, it would probably have to be remote.

Room I need to get up to permit and-or remodel

I am also finding it difficult to balance the expenses of homeownership and frugality. I want to be a good steward of the home and keep it in good repair, but find there are constantly things I need/could spend money on. For example, I had a stump that needed to be removed. I bought a mini-chainsaw to help get rid of the branches and will use it in the future for pruning, but it always feels like there is a several hundred dollar purchase that “needs” to be made. Along with my goals of remodeling/selling the house and generally saving, it’s hard to find what a “good” balance is.

Where Vanessa Wants to be in Ten Years:

After the last two years of pandemic, 10 years from now seems like an eternity…

Finances:

-

Travel Picture: Provance

I would like my mortgage to be almost completely paid off. I recently stopped paying extra (which hurts, because I hate debt but I heeded Mrs. FW’s previous Case Study advice that there are better uses of money when interest rates are low, but I don’t think I’d otherwise have a choice with the new monthly payments).

- I think I am doing fine with retirement contributions (please let me know if I am not!) and will receive a pension when I retire based on salary at the time and years of service.

- I would like the opportunity to be able live comfortable (absolutely within my means) and have discretionary money to spend on charity, travel, etc. without worrying if it should be spent elsewhere.

Lifestyle:

Career:

- The career question is hard because I don’t know what opportunities there might be for me. My answer is that I would like a job that’s challenging and interesting but doesn’t occupy all my time or mental/emotional wherewithal.

- If possible, I would like to stay with my current group for at least the next few years, unless something drastic changes in the leadership or circumstances of my job.

Vanessa’s Finances

Income

| Item | Amount | Notes |

| Vanessa’s Net Income | $4,428 | Vanessa’s net salary after health/vision/dental insurance; life insurance; retirement contribution; taxes; parking. |

| Plasma Donation | $547 | I donate plasma twice a week. The donation center “compensates for my time.” The compensation varies every month and has been higher over the course of the pandemic. It is very difficult to predict how the compensation will change in the future. |

| Boyfriend’s rent payment | $500 | My boyfriend contributes this amount to the mortgage and utilities |

| Side Hustle | $500 | I do some IP consulting on the side. The income is irregular based on my client’s budget. |

| Monthly subtotal: | $5,975 | |

| Annual total: | $71,700 |

Mortgage Details

| Item | Outstanding loan balance | Interest Rate | Loan Period and Terms | Equity | Purchase price and year |

| Mortgage | $182,923 | 1.99% | 15-year fixed-rate mortgage | $62,090.47 | $245,013; purchased September 2018 |

Debts

| Item | Outstanding loan balance | Interest Rate | Loan Period/Terms | Notes |

| Car | $12,000 | 0.90% | Four years; this works out to be about $246/month | |

| Furniture | $2,729 | 0% | I pay 1/12th the initial amount to get the 0% promotional financing; this works out to be about $230/month | I bought my first bedroom set and mattress when I got my tax refund this year. This was naturally three days before my car was murdered. |

| Affirm mattress | $659 | 0% | I pay 1/12th the initial amount to get the 0% promotional financing; this works out to be about $60/month | |

| Total: | $15,388 |

Assets

| Item | Amount | Notes | Interest/type of securities held | Name of bank/brokerage | Expense Ratio |

| Rollover IRA | $103,324 | This account has all my rollover accounts from past jobs | FFFHX; TRRMX | Fidelity | 0.75%; 0.71% |

| 403(b) Account | $50,831 | I contribute 12%/month | FFOPX | Fidelity | 0.81% |

| Individual Account Program (IAP) | $22,285 | My university matches up to 5.25%/month | |||

| Brokerage Account | $21,777 | This is more of a glorified savings account. It has ETF funds based on an aggressive investment strategy. The thought was that given enough time, it would provide a better return than purely a savings account. It has also lost about 10% over the past few months. | ETF | SoFi | N/A; SoFi does not charge fees |

| Savings Account | $15,000 | This is what I consider to be my emergency fund. I typically transfer $500 every month and every few months transfer money into my SoFi brokerage account as bank. | N/A | Chase | N/A |

| Brokerage Account | $10,951 | This is where I invest in individual stocks. I had done well and at least have been able to hold on to any investment long enough to at least break even. It has lost about half its value over the last 6 months because I am invested in biotech stocks and they have taken a severe beating. | Individual stocks | Charles Schwab | N/A |

| Checking Account | $8,363 | This is where most of my transactions occur | N/A | Chase | N/A |

| Second Savings Account | $950 | This is my slush fund. I started it awhile back for mid-range house projects/purchases (up to a few thousand dollars). It has also become my pet emergency fund. I contribute $50 every month. | N/A | N/A | N/A |

| TOTAL: | $233,481 |

Vehicles

| Vehicle make, model, year | Valued at | Mileage | Paid off? |

| VW Jetta | $25,398 | 300 | No; the amount I owe is listed under “Debts” |

Expenses

| Item | Amount | Notes |

| Mortgage, taxes and insurance | $1,574.68 | Principal ($1,018.56), interest ($303.35) and escrow ($252.77) |

| Household | $411 | Includes all household supplies, house decorations, bedding, small appliances, cleaning products, home improvement items |

| Grocery | $322 | Includes all food and beverages (including alcohol) |

| Car payment | $246 | Details under “Debts” section |

| Furniture payment | $230 | Details under “Debts” section |

| Utilities | $182 | Includes electricity and water |

| Charity | $129 | Includes recurring donations and approximate one-off donations from individuals asking for help |

| Pets | $112 | Includes annual vet appointments, food, flea treatment, toys, treats (this is a shared expense with my boyfriend) |

| Medical | $97 | Includes co-pays, contacts, prescriptions, allergy shots |

| Restaurant | $92 | Includes take out from date night (1 date every 1-2 weeks) |

| Hobbies | $85 | Includes gardening and sewing supplies |

| Gifts | $62 | Includes birthdays, Christmas for family and friends |

| Gas | $62 | |

| Affirm mattress payment | $60 | Details under “Debts” section |

| Car Insurance | $59 | |

| Internet | $53 | Includes internet only |

| Firewood | $38 | Includes 2 cords of wood used for heating over the winter |

| Clothing | $18 | Includes clothes and shoes (I buy almost everything off eBay) |

| Garbage | $18 | Includes garbage service |

| Bar Fees | $15 | Includes state bar fees for New York and California |

| Subscriptions | $14 | Includes local newspaper ($8) and Paramount+($6; where I get Star Trek and is extremely valuable to me) |

| Entertainment | $10 | Includes video game, movies, etc. |

| Monthly Subtotal: | $3,890 | |

| Annual Total: | $46,680 |

Credit Card Strategy

| Card Name | Rewards Type? | Bank/card company |

| Alaska Visa | Travel | Bank of America |

Vanessa’s Questions for You

1) Short term: how can I reconfigure my budget to be more balanced?

- In doing the analysis for the Case Study, I saw how much of my budget goes to household goods (generally meaning charges from Target; Bed, Bath, & Beyond; the local hardware store and items like Christmas decorations, mini-chainsaws, chimney cleanings), especially if I want a larger discretionary budget for things like hobbies and traveling?

- Where should I readjust my budget if my boyfriend and I do breakup?

- My income from my side hustle and plasma donations are inconsistent. My side hustle is consulting for a start-up and they don’t necessarily pay on a regular basis (which I am ok with because they do eventually always pay) and the plasma donations are set by the company and can change every month. It is great to have the extra money, but it isn’t something I absolutely count on.

2) Medium term: What should I do about my new car/furniture payment?

3) What are the best saving methods for medium (a few thousand dollars) and large (tens of thousands of dollars) purchases?

- Right now I have a couple of investment accounts, but both of those (one stocks and one ETFs) are down right now. Is there a better strategy or in-between strategy between bank accounts that earn no interest and the temperamental stock market?

4) Long term: Should I remodel or sell my house?

- Either way, I think I will have to save for this because I would like to pay cash (or as much cash as possible) for either. Some of my cash reserves went towards my car’s down payment (about $6K so that my payments would be under $250/month).

- My heart says to keep the house and invest in its care and upkeep, but my head says it is probably not the best financial choice. Also, in say 5-10 years what might the conditions or situations be that could change my decision?

Liz Frugalwoods’ Recommendations

Vanessa’s in great shape and I think a lot of what we’ll be looking at today are longer-term plans, which are fun to map out! I commend Vanessa for thinking through her long term financial plans and am excited to think through these items with her!

Vanessa’s Question #1: Short term: how can I reconfigure my budget to be more balanced?

First area: house-related costs

I actually think Vanessa’s budget is already pretty balanced. I think the disconnect here is that Vanessa may be comparing her post-home ownership budget to her pre-home ownership budget and those two will never be in alignment. Home ownership is wonderful, it’s fun, it can be a great investment, it’s a secure place for your money, but it ain’t cheap. Having now owned two homes myself, I can tell you that something is ALWAYS breaking, something ALWAYS needs to be fixed or replaced and…. the expenses never end. This isn’t to scare Vanessa (or anyone else contemplating home ownership), it’s simply wise to assume it’ll be an ongoing, constant, forever monthly expense. It’s not a bad thing to spend money on needed repairs to a home, it’s just a fact of no longer being a renter.

I suggest Vanessa do the ol’ expense deep dive on all those Bed, Bath & Beyond, Target, hardware store, etc purchases and divide them up according to the below rubric:

1) Emergency, required:

2) One-time, including large appliances:

- For example: the mini chainsaw. Sure, you’ll have to replace it someday, but not annually.

3) Decorative:

- For example: throw pillows, Christmas decorations, etc. Most of these are also likely one-time.

4) Annual maintenance:

- For example: chimney sweeping.

I think re-assessing her budget according to these distinct categories might help Vanessa better metabolize the true costs of home ownership. This will also highlight areas that can be reduced/eliminated if desired (such as “decorative”) and things that need to be budgeted for on a regular basis (such as “annual maintenance”). If she’s not already using an expense tracking service, such as the free one from Personal Capital, doing so might help in this process (affiliate link).

Second area: Where should I readjust my budget if my boyfriend and I do breakup?

Travel Picture-Staircase in Arc de Triomphe

I think Vanessa will have to wait and see on this front. As it is, she’s shouldering the bulk of their household expenses, so I’m not sure the loss of his $500 contribution per month will be all that seismic since I assume things like household supplies (toilet paper, toothpaste, etc) and groceries will likely decrease.

If they do break up, I also encourage Vanessa to give herself some grace and time before being too worried about her new budget. A break-up (even if mutual and desired) is still a seismic change and Vanessa should ensure she takes time for self-care and rest afterwards. Once she’s a few months out from the breakup, she can do an analysis of her post-breakup expenses and how she might want/need to recalibrate.

In general, Vanessa is super frugal and her expenses are really low! Without her boyfriend’s rent payment and both of her side hustles, she’s still making more than she spends every month:

$4,428 (salary) – $3,890 (expenses) = $538

Given that, there’s no hair-on-fire situation for Vanessa to immediately solve if they do break-up. She can take her time to sort through things and determine how/if she wants to adjust her spending going forward.

Vanessa’s Question #2: Medium term: What should I do about my new car/furniture payment?

Orpheus on top of the berry pole

Exactly what you’re doing! Particularly with the 0% interest on the furniture, there are zero mathematical reasons to pay them off early. The thing that’s bad about debt are high interest rates. Debt with no interest rate isn’t bad, it’s a reallocation of resources. The caveat is that if either furniture loan incurs an interest rate at some point, then you might want to pay them off.

In terms of the car, I completely agree with Vanessa’s research and decision to buy a new car. It makes no sense to buy a used car for nearly as much (or as much!) as a new car. In the current ridiculous bananas car market, you might as well buy new. No reason to pay more for used! The only reason it USED to make sense to buy USED is because used cars used to be a TON cheaper than new cars. Now that they’re not, the entire car calculus is changed. So Vanessa, rest assured you made a great decision on this front: you chose a reasonably-priced, safe, new, reliable vehicle. Feel good about the research you did and the decision you made!

The car’s interest rate is also incredibly low at 0.90%. Even though the interest rate isn’t zero, I still agree with Vanessa’s assessment that it makes the most mathematical sense to deploy her resources into assets that will earn her more than a 0.9% return.

With debt-payoff on low or zero interest debts, it’s always a question of:

What’s the opportunity cost of paying off this debt?

In other words, if I don’t dump my money into this debt, what else can my money do for me? Hint: the answer is NOT “take on more debt to buy a boat!,” it’s more like “invest in my retirement, savings or brokerage accounts!”

But this is all a question of personal preference. Sure, it’s mathematically best not to pay off low-interest debt, but some people do so because they value the peace of mind of no debt OVER the potential financial returns of investing their money. Just be clear with yourself about whether you’re making a “peace of mind” or a “financially/mathematically best” decision.

Vanessa’s Question #3: What are the best saving methods for medium (a few thousand dollars) and large (tens of thousands of dollars) purchases?

This question is actually better asked in terms of time horizon, not dollar amounts. Here’s why:

This question is actually better asked in terms of time horizon, not dollar amounts. Here’s why:

1) If I want to buy a house sometime in the next, oh, two years or so, I’ll want to keep that money liquid (in a checking/savings account) so that I don’t lose any of it in the always unpredictable stock market.

2) If I want to buy a retirement condo in the next, oh, forty years or so, I’ll want to invest that money in the stock market (in a taxable brokerage account) so that it can grow over time.

Q: Why do I do this?

A: Market volatility.

If I were to invest all of the money I intend to use for my down payment on a house in the next few years, there’s a very real chance I’d lose some (or most) of that money.

- To be clear, I wouldn’t actually “lose” the money, it would just be fluctuating with the market.

- I would actually lose the money if I sold my stocks during a downturn and locked in that loss.

The stock market goes up and down. That is literally what it’s designed to do. You cannot panic when it goes down–that’s like panicking when a dog wags it’s tail because that is literally what a dog does. I’ll tell you when I’d actually lose my money: if I panicked and sold everything during a market downturn. Then, I’ve locked in a loss and yes, that is bad and yes, people do that because it is human nature to panic when you see your hard-earned $$$$ winnowed down during a downturn.

The stock market goes up and down. That is literally what it’s designed to do. You cannot panic when it goes down–that’s like panicking when a dog wags it’s tail because that is literally what a dog does. I’ll tell you when I’d actually lose my money: if I panicked and sold everything during a market downturn. Then, I’ve locked in a loss and yes, that is bad and yes, people do that because it is human nature to panic when you see your hard-earned $$$$ winnowed down during a downturn.

But if I don’t panic and don’t sell, I DON’T lock in the loss. Instead, I ride the market. I keep my money invested for decades because, history demonstrates that over time, the market goes up. Over time, history has shown a 7% average annual return. As long as I don’t panic and sell in a downturn. Now could history not repeat itself and the market fall off a cliff? Absolutely! Also, could we be hit by an asteroid? Absolutely! Investing is risky; living on Earth is also risky. Only YOU know your personal risk tolerance and only YOU can make the investment choices that align with your goals and your risk tolerance.

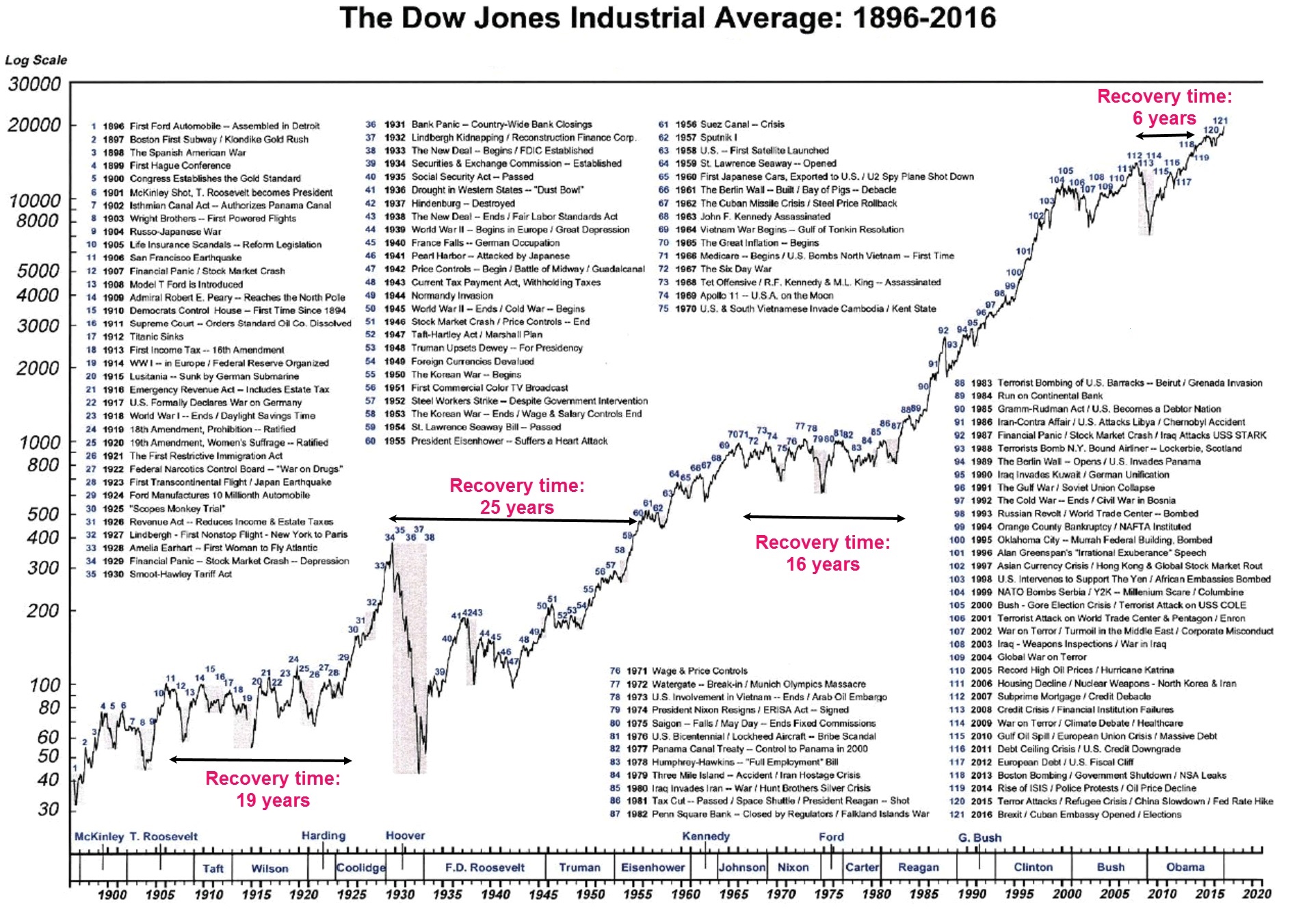

Here’s a graph of the Dow Jones Industrial Average’s behavior over a 120-year period (1896-2016):

This long-winded, cartoon-riddled answer is to illustrate for Vanessa (and everyone else) that investing is a question of your time horizon, more so than your dollar amount, as well as your risk tolerance.

Short Term Savings

Now that we’ve established the stock market is the place for our LOOOOONNNNNGGG term money, what do we do with our short term money? Several options:

- Checking account

- High-yield savings account

Picture of Foster Kittens 2

The stock market is not a savings account. It’s a long-term investment account. You only put in money you do not need anytime soon.

Things that are NOT savings accounts:

- ETFs

- Individual stocks

- 401ks

- Pensions

- Total market index funds

- Dogs wagging their tails

Things that ARE savings accounts:

- Savings accounts

Asset Allocation and Investing Strategy

Let’s do a rundown of where Vanessa has her money:

1) Cash:

Cat-Freya

Vanessa has three different liquid (AKA checking/savings) accounts totaling: $24,313

What is cash for? Everyone say it with me:

- Emergency fund (this should be three to six month worth of your living expenses).

- Living expenses.

- Saving for near-term larger purchases (vacations, new cars, a dress for your sister’s wedding, a new cat condo, etc)

Vanessa spends $3,890 a month, which means she should have an emergency fund of $11,670 (three months worth) to $23,340 (six months worth). Hence, her cash savings are spot on!

Suggested tweaks:

- Perhaps combine these three accounts into one? This is a personal preference and I like to have everything as consolidated as possible, but I know some folks prefer multiple ear-marked accounts. If there’s no pressing reason to have three different accounts, I’d combine for simplicity

- Move everything to a high-yield savings account(s). Interest rates are rising right now and one the only areas where this is advantageous are high-yield savings accounts. Make sure you’re earning something on your savings account–never settle for 0%. Even a small percentage makes a difference over time.

- For example, the American Express Personal Savings account currently earns 0.60% in interest. This is not a ton, but in a year, Vanessa’s $24,313 will have increased to $24,459 (affiliate link). That means she’d earn $146 just by having her money in a high-interest account!

2) Retirement:

Harvest Display

Vanessa’s three retirement accounts total $176,440. Let’s reference our favorite retirement rule of thumb:

Aim to save at least 1x your salary by 30, 3x by 40, 6x by 50, 8x by 60, and 10x by 67 (source: Fidelity).

Since Vanessa’s 37, let’s go with age 40. This means she should have:

[$4,428 x 12 =] $53,136 x 3 = $159,408

Vanessa is 100% spot on in this category as well! Woohoo, Vanessa is rocking it!

3) Taxable investments:

The rules around taxable investments are:

- Make sure you understand the basics of investing. I highly recommend the book The Simple Path to Wealth: Your Road Map to Financial Independence And a Rich, Free Life, by: JL Collins (affiliate link). It is a fantastic primer on investing.

-

Orpheus helping Vanessa transplant

Only invest money you don’t need in the near term.

- Remember that investing is for the long term.

- Don’t panic and sell when the market goes down.

- If you do this, it defeats the entire purpose of investing. You’d likely be better off not investing at all.

- Make sure you understand the fees/expense ratios of your investments. I did a deep dive on expense ratios in this post. All investment accounts have fees associated with them. If they don’t have a fee, they’re not an investment account. It’s crucial to have low fees because you can lose a TON of money to high fees over the decades of your investing career. Three brokerages known for their low-fee total market index fund options are:

- Fidelity

- Vanguard

- Charles Schwab

- I choose to invest in total market, low-fee index funds. Read The Simple Path to Wealth to understand why this is the choice I (and the vast majority of other FIRE folks) make.

I also want to highlight for Vanessa that investing in individual stocks is a hobby, not an investment strategy. Stock picking is something a lot of people enjoy doing for fun, but it’s not a wise financial move. Only do this if you have money to burn and really enjoy picking stocks. Otherwise, historical market data indicates you’re better off in a total market low-fee index fund.

Vanessa’s Question #4: Long term: Should I remodel or sell my house?

Cats-Orpheus (Top) Gandalf(Bottom)

Vanessa hit the nail on the head when she said that either way, she’l likely have to wait. Yep, yep, yep. If anything is more hot cocoa bananas than the car market right now, it’s the housing market. Now is not the time to buy a home unless you absolutely have to. Ditto for renovations you’ll be hiring someone else to perform. Contractors are fully booked and materials are either unavailable or expensive. Or more likely, both.

I think Vanessa is wise to think about this potential future decision and to start looking at homes for sale in her area. Never hurts to go to a few open houses to get a sense of what’s on the market. If nothing else, it could provide some renovation ideas and thoughts on how to deal with her unusual upstairs room.

Vanessa has an absolutely fantastic interest rate (1.99%!!!!!!!) on her mortgage, so she is sitting pretty right now. Don’t do anything to jeopardize this enviable situation!

Summary:

For the most part, Vanessa should just keep doing what she’s already doing! She’s made excellent financial decisions over the years. The few tweaks I suggest:

-

Travel Picture: Ecola State Park in Oregon

Do a deep dive into house-related expenses and create sub-categories for:

- Emergency, required

- One-time, including large appliances

- Decorative

- Annual maintenance

- Feel confident about not paying off the car, house and furniture at an accelerated pace because the interest rates are fabulously low.

- Read The Simple Path to Wealth: Your Road Map to Financial Independence And a Rich, Free Life, by: JL Collins, to broaden her knowledge and understanding of investing (affiliate link).

- Identify the time horizons for her larger purchases and determine if investing or cash will be wisest.

- Do an analysis of all accounts and consider:

- Consolidating cash accounts into one. Ensure this account is high-yield and earning interest.

- Consider eliminating the individual stocks account and instead focusing on low-fee, total market index funds.

- Wait on making the renovate or move decision. Spend this time gathering data: interview contractors, visit open houses, get renovation ideas, and save up!

- Know that you are doing a great job!!

Ok Frugalwoods nation, what advice do you have for Vanessa? We’ll both reply to comments, so please feel free to ask questions!

Would you like your own case study to appear here on Frugalwoods? Email me (mrs@frugalwoods.com) your brief story and we’ll talk.

Never Miss A Story

Sign up to get new Frugalwoods stories in your email inbox.

{kind=link}