Executive Summary

The arrival of robo-advisors into the financial technology landscape more than a decade ago led many to believe that the combination of (relatively) low fees and digital presence offered by robos would entice many consumers to eschew human advisors and turn to these automated tools. However, since the introduction of robo-advisor technology, client behavior has suggested that these original predictions of robo dominance and the downfall of human advisors have not been borne out.

A new 2022 Vanguard Group report by Paulo Costa and Jane Henshaw helps explain why this turned out to be the case. By surveying households (with at least $100,000 in investable assets) that use human advisors, robo-advisors, or both, the authors found that clients of human advisors were not only more satisfied with the overall service they receive compared to clients of robo-advisors, but also that these clients perceive their human advisors to offer more value in three specific dimensions: portfolio value (i.e., optimal portfolio construction and client risk-taking), financial value (i.e., attainment of financial goals), and emotional value (i.e., financial peace of mind).

While clients of human advisors reported more perceived value from their advisors than did clients of robo-advisors in these areas, the Vanguard study also found that clients do have a preference for human advisors and digital tools to handle different aspects of financial advising. For example, the highest-ranked functions where clients preferred human advisors included feeling understood, having a connection/relationship, working in their best interests, and being empathetic to the client’s needs. On the other end of the spectrum, the areas where clients preferred digital tools included simplifying their portfolio for organized, cohesive management; diversifying their investments; managing capital gains and taxes effectively; and preventing details from being overlooked. Notably, these results were similar across client demographics, including age, wealth, and whether they currently use a human or robo-advisor.

These results suggest that human advisors who recognize and focus on the areas that clients want an actual person to handle – while potentially outsourcing other tasks that clients prefer to be handled through digital tools – could help strengthen their relationships with current clients (by allowing them to focus on the specific areas that involve connecting with clients) and promote firm growth into the future (by freeing up their time to work on business development). In fact, the study found that clients of robo-advisors are quite willing to work with a human advisor in the future, with 88% of these respondents saying they would be willing to do so (while only 4% of clients of human advisors said they would switch to a robo-advisor if they had to leave their current advisor).

Ultimately, the key point is that the Vanguard study shows not only that consumers continue to seek out human advisors, but also that those who do become clients feel that they receive high levels of service. Further, the results suggest that human advisors who focus on the areas where human support is most valued (including active listening and understanding their goals) while leveraging digital tools for other tasks are likely to attract more clients, including those who may currently be using a robo-advisor!

The arrival of robo-advisors into the financial technology landscape more than a decade ago led some in the advisor community to believe that the robos’ combination of (relatively) low fees and digital presence could entice many consumers to eschew human advisors and turn to these automated robo-tools. However, since the introduction of robo-advisor technology, client behavior has suggested that these original predictions of robo dominance and the downfall of human advisors have not been borne out. In fact, improvements in automation technology (including robo-advisor services built for human advisors) have made human advisors more efficient and profitable despite pressure on fees (perhaps partially brought on by the presence of robo-advisors).

A new 2022 Vanguard Group report by Paulo Costa and Jane Henshaw helps explain why this turned out to be the case. Using a survey of households with at least $100,000 in investible assets that use human advisors, robo-advisors, or both, the authors found that clients of both human and robo-advisors are typically satisfied with the service they receive (with 84% of human-advised and 77% of robo-advised clients reporting that they were satisfied).

But within the various parts of the financial planning process, consumers have different expectations of the services robo-advisors (and related automated tools) provide and those that are provided by human advisors. In addition to the different expectations consumers have of robo and human advisors, the survey results also show that consumers report greater benefits when working with a human advisor across several dimensions of financial advice (including portfolio management, financial planning, and behavioral management), signaling that client outcomes may be improved by working with a human advisor. This is further reflected by the willingness reported by robo-advisor clients to switch to a human advisor (and the lack of consideration among those with human advisors to switch to a robo-advisor).

This does not necessarily mean that human advisors should forsake robo tools; in fact, advisors who are able to best leverage these technologies for clients who prefer automated services can focus on the parts of the financial planning process that human advisors can provide best… and they may also attract and retain more clients going forward!

Three Domains Of Value That Advisors Provide

Traditionally, investment management has been one of the primary services provided by financial advisors. But with the development of financial planning as a profession (and the burgeoning rise of financial advicers), other elements of clients’ financial situations (e.g., tax planning, insurance planning, estate planning) have been added to the value proposition of working with an advisor. And beyond these dollars-and-cents categories of financial planning, human advisors are able to address the behavioral and emotional elements of a client’s financial life. So, while robo-advisors are able to automate much of the investment management process, human advisors are able to provide unique support in many other key areas.

The Vanguard report examines these areas through a three-part, value-of-advice framework (first introduced by Cynthia Pagliaro and Stephen Utkus) to assess how human advisors and digital advisors stack up in the eyes of their clients. This framework divides the value of financial advice into three domains:

- Portfolio value (i.e., optimal portfolio construction and client risk-taking);

- Financial value (i.e., attainment of financial goals); and

- Emotional value (i.e., financial peace of mind).

Using this framework, the survey results reported that human advisors were considered to be superior to robo-advisors across all three dimensions.

Dimension 1: Portfolio Value

Consumers often engage financial advisors (whether human or digital) when they realize they need help managing their portfolios. Perhaps the investor made ill-timed trades during a volatile period in the market, or they simply want to unload the responsibility of managing their investments.

An advisor can provide significant value to these clients through several techniques: constructing a portfolio to reflect the client’s preferences for risk and return, investing in a tax-efficient manner, managing the fees of the underlying investments in the portfolio, rebalancing and trading within the portfolio when appropriate, and managing the ‘behavior gap’ involved in investing.

According to respondents in the Vanguard study, both human and robo-advisors add value to their portfolios. While it was impossible for the researchers to compare the respondents’ actual investment returns with what they would have earned without an advisor, they were able to ask those surveyed about their returns with the advisor and what they estimate they would have made had they invested on their own. Clients of human advisors noted that they averaged 15% annual returns in the previous three years, but estimated that their portfolio would have only grown by 10% without an advisor (a 5-percentage-point gap). Those using robo-advisors said that they had 24% annual returns in the previous three years, but would have had 21% annual returns investing on their own (a 3-percentage-point gap).

So while the clients of robo-advisors reported higher absolute returns than clients of human advisors (perhaps because they have a higher risk tolerance), the key point is that clients of human advisors perceived that they received a greater benefit, as measured by the relative percentage-point gap between actual managed and estimated unmanaged performance, from working with their advisor than did the clients of robo-advisors.

Dimension 2: Financial Value

Of course, while portfolio performance is important, it is only one part of the financial planning process. Considering a client’s investment returns alone does not indicate whether they are making progress on their overarching financial goals. Which is a critical element for clients engaging a financial advisor; in fact, clients often report that getting help to achieve their financial goals is the most important part of working with an advisor. Accordingly, advisors have several ways to help clients get where they want to be financially, including monitoring saving and spending behavior, managing debt levels, retirement income planning, insurance and risk management, and estate planning.

Importantly, the Vanguard study found that clients of human advisors actually do perceive that they are closer to achieving their goals compared to those working with robo-advisors: clients of human advisors said they were 59% of the way to achieving their financial goal, but estimated that they would have only reached 43% of their financial goal had they not worked with an advisor (a 16-percentage-point gap). Whereas those working with robo-advisors noted that they had met 50% of their financial goal and thought they would have been at 45% of their goal had they been on their own (a 5-percentage-point gap).

Thus, if attaining the median financial goal of $1 million is used to quantify advisor value, then the value gap perceived by clients of human and robo-advisors was $1,000,000 x 16% (human advisor value gap) – $1,000,000 x 5% (robo advisor value gap) = $110,000!

Given that robo-advisors are a relatively recent development compared to human advisors, it’s possible that one of the reasons clients of human advisors assessed they were closer to achieving their goals was merely the amount of time receiving the benefits of working with an advisor. As while clients who had worked with a human advisor for at least 10 years showed the largest percentage-point gap (23%) between how close they were to achieving their goal and how close they would be investing alone, even those who reported working with a human advisor for only two years or less reported an 11-percentage-point gap between how close they were to achieving their goal and where they would have been without an advisor (greater than the 5-percentage-point gap for all clients of robo-advisors). Which suggests that, combined with the greater perceived portfolio benefits of working with a human advisor, clients also perceive that their human advisors add more value in helping them achieve their overall financial goals!

Dimension 3: Emotional Value

Many clients work with advisors not just for the tangible benefits (e.g., portfolio performance or achieving goals), but also for the peace of mind from knowing that a qualified expert is looking out for their financial best interests.

According to the Vanguard study, when clients compared their attitudes between having their advisor manage their investments with self-managing their portfolios themselves, clients with human advisors reported having more peace of mind knowing that their advisor was looking after their investments than those working with robo-advisors.

While 80% of clients with human advisors reported having peace of mind knowing that their advisor was looking after their investments, only 24% said they would do so if managing their investments on their own (a 56-percentage-point gap!). For clients of robo-advisors, 71% reported having peace of mind, with 59% expecting they would do so investing on their own (a 12-percentage-point gap).

While the gap between human and robo-advisors in emotional value could reflect the type of investors who use each service (e.g., perhaps clients who worry more may be more likely to choose a human advisor than a robo-advisor in the first place), the study demonstrates that human advisors can add significant emotional value to clients who would otherwise be concerned that their investments were off track!

Where Human Advisors Provide The Most Value

Even though clients of human advisors report more perceived value from their advisor than do clients of robo-advisors, this does not necessarily mean clients believe human advisors are superior in the wide range of tasks an advisor might perform. In fact, according to the Vanguard study, there were several areas where clients preferred digital tools over humans, suggesting that some clients might have a more favorable impression of a human advisor who takes on the responsibilities they feel are best performed by a human while delegating other tasks to digital tools.

Clients Prefer Human Advisors For Soft Skills, Robos For Functional Tasks

The Vanguard researchers presented respondents with a wide range of potential interactions with their advisor and asked them to identify whether they would prefer that function be carried out by a human or by robo tools. While clients preferred human advisors for most tasks, the strength of this preference varied widely, and they actually preferred digital delivery of certain tasks.

In terms of the relative preference favoring human advisors, the highest-ranked functions included feeling understood, having a connection/relationship, working in their best interests, and being empathetic to the client’s needs. Other areas where human advisors had a relative advantage included supporting clients through market volatility and life events and making sure the client understood their financial plan well. These results are perhaps not surprising given human advisors’ advantage over robo-advisors in being able to speak with and be emotionally accessible to clients on a person-to-person level.

On the other end of the spectrum, areas where clients preferred digital tools to human advisors included simplifying their portfolio for organized, cohesive management; diversifying their investments; managing capital gains and taxes effectively; and preventing details from being overlooked. This possibly reflects greater trust in automation and a more mechanical approach to calculating appropriate asset allocations and tax analyses (which is reflected in the wide range of advisor technology offerings in these areas!).

It is interesting to note that these results are not specific to age and wealth demographics. In fact, when looking at different generations (Millennial, Gen X, and Boomer) and levels of wealth (mass affluent, high net worth, and ultra-high net worth), the study found that respondents across these measures had highly correlated responses to the types of functions they prefer done by humans or by robo tools (e.g., the correlation between responses by Millennials and Boomers was 0.95 and the correlation between mass affluent and ultra-high net worth respondents was 0.97).

Even though there are differences in the type of advisor individuals of different ages choose (e.g., Millennials made up 46% of robo-advisor clients surveyed but only 17% of human-advised clients), individuals across the demographic spectrum surveyed share roughly similar views on the types of functions they would prefer to be carried out by human or robo advisors.

In addition, current clients of human advisors and digital advisors gave highly correlated (0.96) responses as well, indicating broad agreement among clients as to the services that they would prefer to be performed by humans and by digital tools.

These results indicate that, regardless of age or wealth, clients of human financial advisors do not necessarily expect (or want!) their advisor to take on every potential responsibility in the financial planning process, preferring them to focus on the more psychological and emotional elements of planning while deferring to digital tools for efficiency and portfolio optimization.

At the same time, because there are many functions where clients (both with human advisors and robo-advisors) prefer humans, there is an opportunity for human advisors to bring on clients of robo-advisors who might be interested in having these needs met.

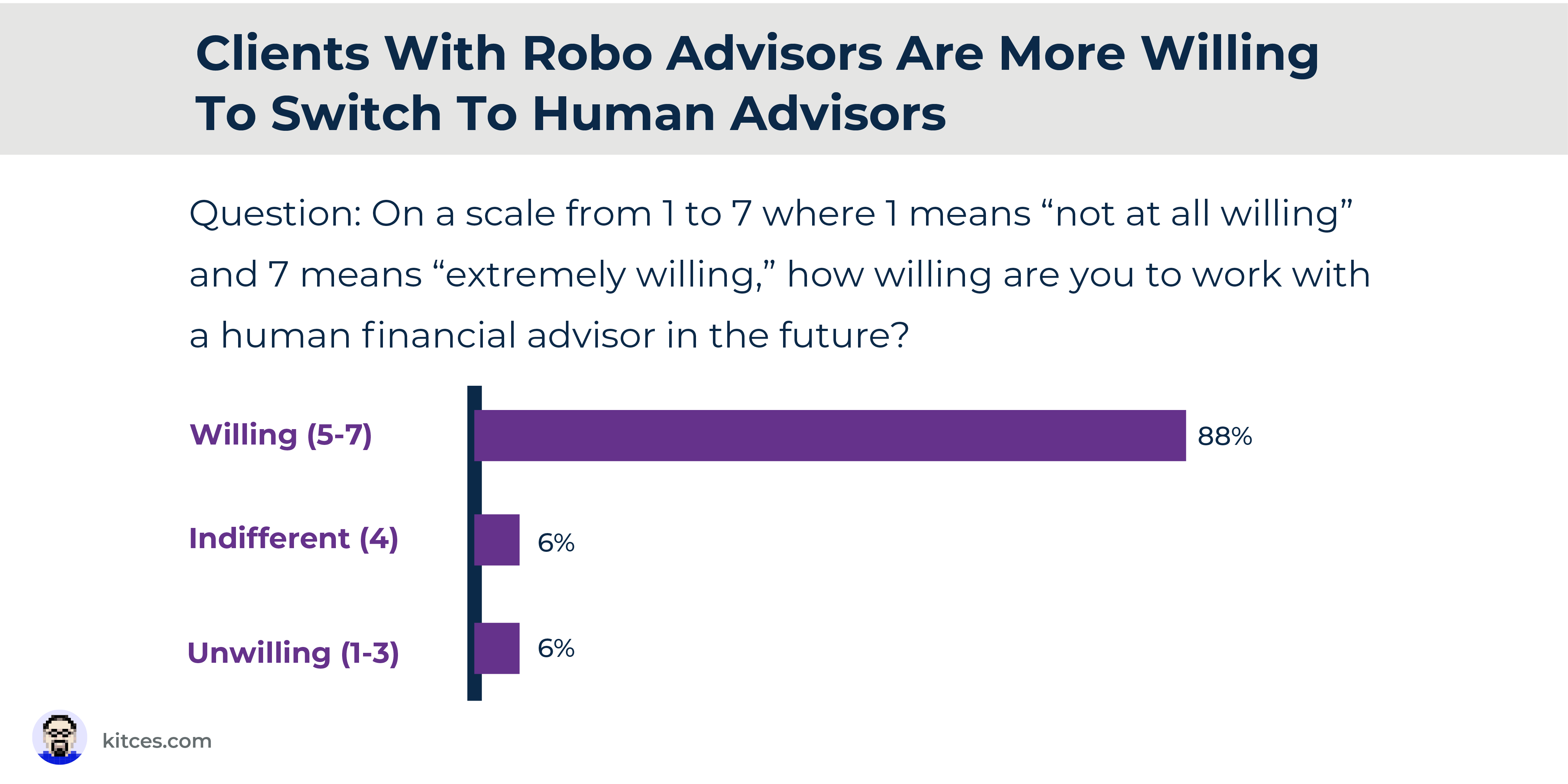

Robo-Advisor Clients Would Consider Switching To Human Advisors

The arrival of robo-advising platforms into the financial advice space originally led to some concern among human advisors that their clients (and future prospects) would be lured away by the robos’ (often) lower fees and sleek digital tools. But the last several years have shown that this was not to be the case, with human advisors thriving while many of the robo-advisors have stagnated, suggesting there really is something unique that clients value about human advice.

These observations are borne out by Vanguard’s study, which asked respondents with human advisors to identify the type of advisor they would choose if they had to leave their current advisor. The study found that 76% of respondents with human advisors would choose another human advisor, while 17% would move to a service combining a digital and human advisor, and only 4% would move to a robo-advisor. This finding indicates that clients of human advisors are not just loyal to their own advisor, but to the concept of working with a human advisor more generally (and suggests that robo-advisors are unlikely to pick up many former clients of human advisors).

On the other hand, the study found that clients of robo-advisors are quite willing to work with a human advisor in the future. In fact, 88% of these respondents said they would be willing to do so, while only 6% said they would be unwilling to work with a human advisor.

When considered alongside the study’s results regarding preferences for human- versus robo-provided services, these results suggest that clients of robo-advisors could be amenable to working with a human advisor, perhaps one that provides the psychological support that humans provide best and who leverages the portfolio construction and automation tools they are used to using with a robo-advisor.

How Human Advisors Can Leverage Their Strengths

The Vanguard study demonstrates not only that there remains a place for human advisors in a world of robo-advisors and other digital offerings, but also that human advisors have a distinct advantage in the minds of clients who seek a range of advice-related services. Recognizing and focusing on these strengths while potentially outsourcing other tasks to digital tools could help human advisors strengthen their relationships with current clients and promote firm growth into the future.

The Importance Of Listening

One of the unique attributes of working with a human advisor is their ability to listen to the client’s needs and concerns. In the Vanguard study, respondents reported strong preferences for certain listening-based interactions with humans rather than digital tools, including feeling understood, being listened to, and being given empathetic attention to their personal situation and needs. Of course, the ability to provide clients with these interactive qualities requires skill, particularly in active listening.

For example, an advisor who focuses more on explaining their services to a prospect than on listening to the prospect’s concerns is much less likely to give the prospect a feeling of being heard when compared to an advisor who spends most of the conversation listening to the prospect to develop a genuine, empathetic connection with them. These skills are especially important when working with client couples, as it is important for both individuals (who may each have very different attitudes and opinions about financial planning) to feel heard by the advisor.

While many advisors have tended to be more comfortable meeting with clients face-to-face, the recent shift toward virtual meetings can actually help advisors create intimacy with clients (though there are pitfalls to avoid). For example, research shows that virtual client meetings create a lower barrier to entry for otherwise-nervous clients who want to meet and provide more flexibility in how and when meetings happen, as they offer increased logistical convenience and reduce any stress around actually going to the meeting itself.

However, meeting virtually does offer its own challenges, as advisors may find it more difficult to read the client’s or prospect’s body language and nonverbal cues, which heightens the importance for the advisor of removing distractions (e.g., computer and phone notifications) to better focus on active listening.

Outsourcing Portfolio Management

While some financial advisors come from a background in investments and enjoy specializing in portfolio management, other advisors may instead prefer to focus more closely on other parts of the financial planning process. And judging by the Vanguard data, many clients do not expect (or even want) their advisors to be actively managing their portfolios. This suggests that while some investment-focused advisors might be able to attract clients who do want active management, many advisors could save time (and perhaps attract and retain clients more effectively) by outsourcing portfolio management.

In fact, amid stalled growth in direct-to-consumer offerings (and the high costs associated with client acquisition), some robo-advisors have shifted to a business-to-business model instead, serving advisors in order to grow the assets using their portfolio management offering. In addition, a range of digital advice platforms for RIAs provides advisors with a range of potentially time-saving digital tools, including digital onboarding, risk profiling, portfolio construction, and account aggregation. When combined with portfolio management features like automated rebalancing and tax-loss harvesting, these digital tools cover many of the functions that respondents to the Vanguard survey preferred to be completed by digital tools rather than humans.

So whether a firm creates a tech stack of these tools (or builds their own), incorporating technology for portfolio management (among other areas) can potentially allow advisors to focus on other planning areas while giving many of their clients added confidence in how their money is being invested.

How To Attract Young Clients

As the popularity of robo-advisors grew, the trend attracted consumers with characteristics that were different from those seeking human advisors. In fact, according to the Vanguard study, while more than 60% of those who currently work with a robo-advisor said they have the time, willingness, and ability to manage their own investments, less than 40% of those working with human advisors said the same.

In addition, clients with robo-advisors tend to be younger; while 83% of the human-advised respondents consisted of older Boomer and Gen X clients, only 53% of respondents with robo-advisors consisted of clients from these same generations.

So while younger clients tend to use robo-advisors more frequently than Boomers (as noted earlier), the study also showed that a client’s age was not a significant factor in terms of what services clients want humans to provide and those they want to be completed by digital tools.

In addition, the finding that a majority of robo-advisor clients expressed openness to working with a human advisor in the future suggests that human advisors do have an opportunity to work with more of today’s younger clients, but that doing so would likely require either building out a service model that attracts young clients (and justifies the likely higher fee than they would be paying with a robo-advisor), or perhaps just waiting for their financial situations to be sufficiently complex that they decide to seek out a human advisor.

Either way, the Vanguard study suggests that today’s robo-advisor clients could be tomorrow’s clients of human advisors as their situations (or the offerings of human advisors) change.

Ultimately, the key point is that the Vanguard study shows not only that consumers continue to seek out human advisors, but also that those who do become clients receive high levels of service. Despite the presence of robo-advisors for the past decade, consumers continue to recognize the value that only human advisors can provide.

Further, the results suggest that human advisors who focus on the areas where human support is most valued (including active listening and understanding their goals) are likely to attract more clients, potentially including those who currently use a robo-advisor but would be open to working with a human advisor.

In the end, the study reaffirms that predictions of the looming demise of human advisors with the introduction of robo-advisors were greatly exaggerated, and that advisors who are best able to showcase what makes them human (and who can also leverage the available robo technology) in their practices are likely to see even greater success in the future!

{kind=link}