Summary

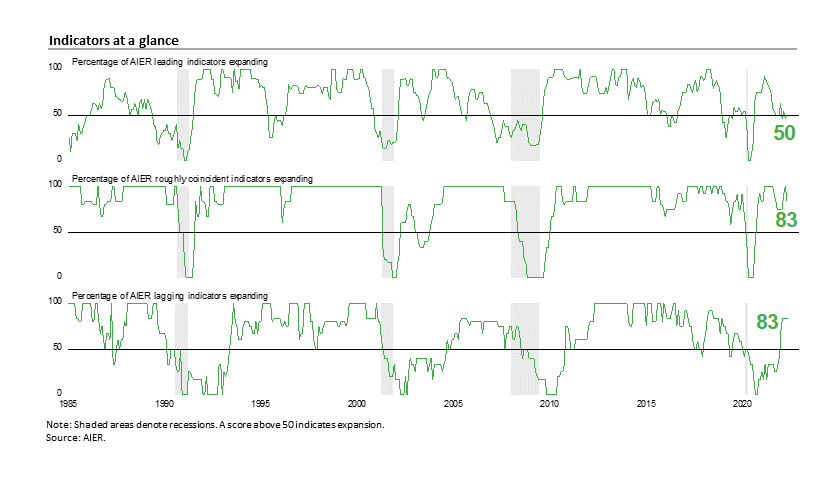

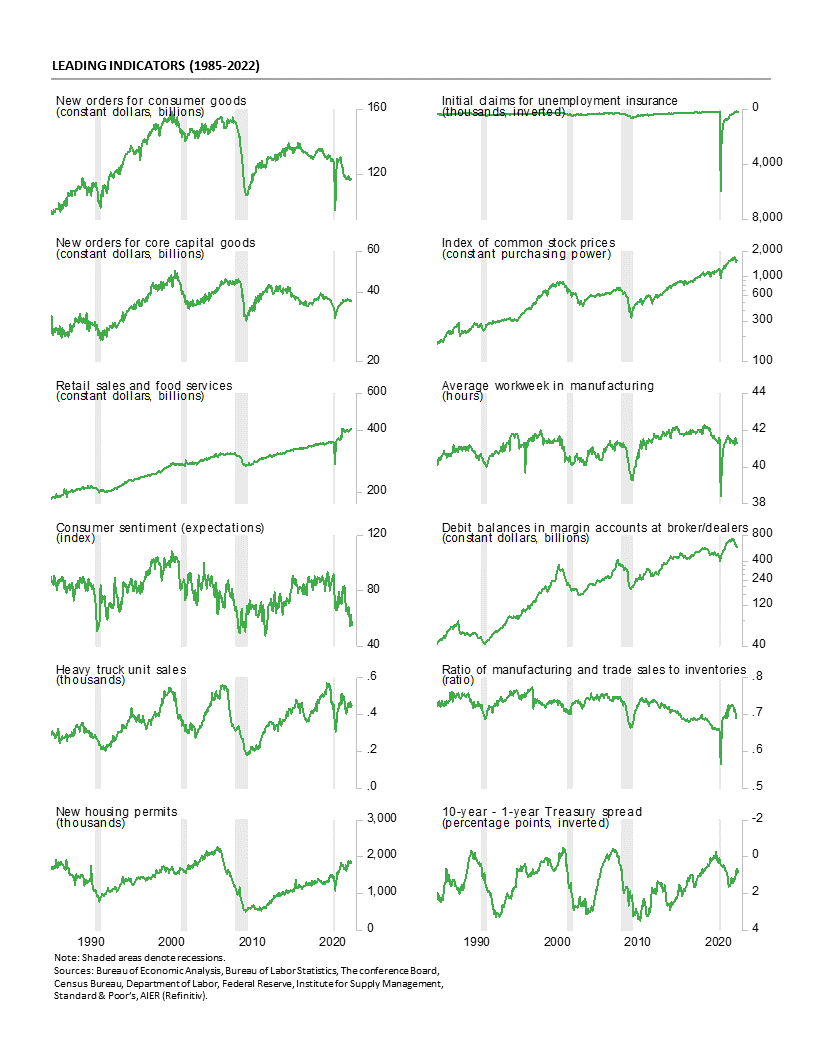

AIER’s Leading Indicators Index returned to a neutral 50 reading in May, rising four points following an eight-point fall in April. The Leading Indicators Index continues to fluctuate around the neutral 50 threshold, with the average over the last eight months holding at 51 (see chart). Over the last eight months, the Leading Indicators index has been above neutral twice, below neutral twice, and exactly neutral four times.

Board trends and risks of persistent upward pressure on prices, labor shortages and turnover, fallout from the Russian invasion of Ukraine, and lockdowns in China in response to outbreaks of COVID-19 remain significant forces impacting the domestic and global economies. Furthermore, a Fed tightening cycle raises the risk of a policy mistake. However, the strong labor market provides support for consumer incomes and spending, though it may also fuel a wage-price spiral.

While broad trends and risks continue, there are some signs of inflection in a few areas. Housing is showing some mixed signs while consumer sentiment has weakened, largely driven by the impact of persistent price increases. In addition, savings rates and spending as a share of income may be sending some early warnings. Caution is warranted.

AIER Leading Indicators Index Falls Back in May

The AIER Leading Indicators index posted a small bounce in May, gaining 4 points to 50 after falling 8 points in April. Over the last eight months, the Leading Indicators index has been above neutral twice, below neutral twice, and exactly neutral four times, putting the average reading over that time at 51.

Three leading indicators changed signal in May, with one weakening and two improving: the real retail sales indicator improved from a neutral trend to a favorable trend and the real new orders for consumer goods indicator improved from a negative trend to a neutral trend. Partially offsetting those positive results was a softening in the average workweek in manufacturing indicator, weakening from a positive trend to a neutral trend. Among the 12 leading indicators, five were in a positive trend in May while five were trending lower and two were trending flat or neutral.

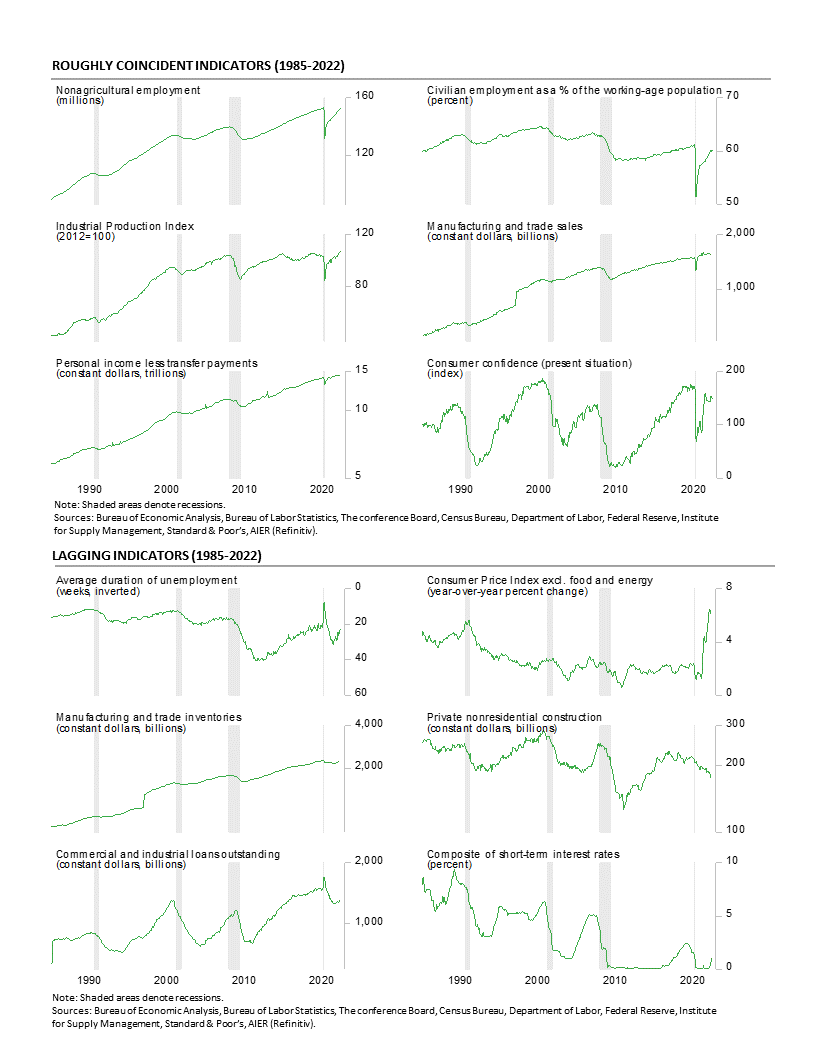

The Roughly Coincident Indicators index fell back in May, dropping to a reading of 83 following two consecutive gains that put the index at a perfect 100 in April. One indicator weakened in May. The real manufacturing and trade sales indicator fell from a positive trend to a neutral trend. Overall, all five indicators – nonfarm payrolls, employment-to-population ratio, industrial production, real personal income excluding transfers, and The Conference Board Consumer Confidence in the Present Situation – were trending higher in May while the real manufacturing and trade sales indicator was in a flat or neutral trend.

AIER’s Lagging Indicators index was unchanged for the fourth consecutive month, holding at 83 in May. February through May was the best four-month run since a four-month run at 83 from July through October 2018. No individual indicators changed trend for the month. In total, five indicators were in favorable trends, one indicator had an unfavorable trend, and none had a neutral trend.

Lingering materials shortages, labor shortages and turnover, and logistical problems continue to slow the recovery in production across the economy and are sustaining upward pressure on prices. Upward price pressures have resulted in a new cycle of Fed policy tightening, raising the risk of a policy mistake. Furthermore, the Russian invasion of Ukraine and recent lockdowns in China in response to a recent wave of COVID-19 have launched a new wave of potential disruptions to global supply chains.

The outlook is for continued economic growth, but risks remain elevated. Consumer spending has been a solid source of growth but there may be some signs that the rate of growth in consumer spending may be unsustainable. Housing is also showing some signs of fatigue as record home prices and surging mortgage rates temper demand.

Additionally, 2022 is a Congressional election year. Intensely bitter partisanship and a deeply divided populace could lead to turmoil as confidence in election results come under attack. Contested results around the country could lead to additional economic disruptions and government paralysis, again testing the durability of democracy. Caution is warranted.

Retail Sales Post Strong Gains in April

Retail sales and food-services spending rose 0.9 percent in April following a 1.4 percent gain in March, with the increase from a year ago coming in at 8.2 percent. The latest retail sales data incorporate annual revisions. Revised data now show stronger upward trends for total and core retail sales.

Furthermore, these data are not adjusted for price changes. In real terms, total retail sales were up 0.6 percent (adjusted using the CPI) following a 0.2 percent increase in March and are also now showing stronger upward trends.

Core retail sales, which exclude motor vehicle dealers and gasoline retailers, rose 1.0 percent for the month, following a 1.2 percent gain in March. The gains leave that measure with an 8.2 percent gain from a year ago. After adjusting for price changes, real core retail sales rose 0.5 percent in April, the fourth monthly gain in a row, and are up 2.0 percent from a year ago.

Categories were mostly higher for the month with nine up and four down in April. The gains were led by a 4.0 percent increase in miscellaneous store retailers. Nonstore retailers and automotive retailers followed with 2.2 percent increases, while food services and drinking establishments (restaurants) had a 2.0 percent rise.

Gasoline spending led the decliners, down 2.7 percent for the month. However, the average price for a gallon of gasoline was $4.37, down 0.7 percent from $4.40 in March, suggesting price changes accounted for some of the move. Sporting goods, hobby, musical instrument, and bookstores sales were off 0.5 percent, and food and beverage store sales were down 0.2 percent.

Overall, retail sales rose for the month and revised data show a stronger trend in recent months. However, rising prices are still providing some boost to the numbers. Furthermore, persistent elevated rates of price increases are starting to have a negative effect on consumer attitudes.

Inflation Fears and Declining Buying Conditions Extend the May Drop in Consumer Sentiment

The final May results from the University of Michigan Surveys of Consumers show overall consumer sentiment continued to fall in the latter part of May. The composite consumer sentiment decreased to 58.4 in May, down from 59.1 in mid-May and 65.2 in April. The final May result is a drop of 6.8 points or 10.4 percent. The index is now down 42.6 points from the February 2020 result and at the lowest level since August 2011.

Both component indexes posted declines. The current-economic-conditions index fell to 63.3 from 69.4 in April. That is a 6.1-point or 10.0 percent decrease for the month and leaves the index with a 51.5-point drop since February 2020 and puts the index at its lowest level since March 2009.

The second sub-index — that of consumer expectations, one of the AIER leading indicators — lost 7.3 points or 11.7 percent for the month, dropping to 55.2. The index is off 36.9 points since February 2020 and is at the second-lowest level since November 2011.

All three indexes are near or below the lows seen in four of the last six recessions.

According to the report, “This recent drop was largely driven by continued negative views on current buying conditions for houses and durables, as well as consumers’ future outlook for the economy, primarily due to concerns over inflation.” However, the report adds, “At the same time, consumers expressed less pessimism over future prospects for their personal finances than over future business conditions. Less than one quarter of consumers expected to be worse off financially a year from now.” Furthermore, the report states, “Looking into the long term, a majority of consumers expected their financial situation to improve over the next five years; this share is essentially unchanged during 2022. The report’s take-away, “A stable outlook for personal finances may currently support consumer spending. Still, persistently negative views of the economy may come to dominate personal factors in influencing consumer behavior in the future.”

The one-year inflation expectations ticked down slightly to 5.3 percent in May, down from 5.4 percent in April. The one-year expectations has spiked above 3.5 percent several times since 2005 only to fall back. The five-year inflation expectations remained unchanged at 3.0 percent in May. That result remains well within the 25-year range of 2.2 percent to 3.5 percent.

The weakening trend in consumer attitudes reflects a confluence of events with inflation leading the pack. Persistent elevated price increases affect consumer and business decision-making and distort economic activity.

Strong Retail Spending May Not Be Sustainable

With retail sales continuing to run above the recent eight-year trend, measured as a share of disposable income and disposable income excluding government transfers, retail sales are 3.7 percent and 4.7 percent, respectively, above the pre-pandemic ranges of 3.0 percent to 3.4 percent for total disposable income and 3.8 percent to 4.2 percent for disposable income excluding transfers that persisted for the 2011 though 2019 period.

At the same time, the personal savings rate has fallen sharply, coming in at 4.4 percent of disposable income in April, well below the five-year average rate of 7.4 percent through December. That is the lowest rate since a 3.8 percent rate in August 2008, in the middle of the severe 2008 – 2009 recession.

Furthermore, total consumer credit outstanding rose by $52.4 billion to $4,539.0 billion in March, a 1.2 percent increase from the prior month. From a year ago, total consumer credit is up 7.3 percent.

Within the total, revolving credit, primarily credit cards, added $31.4 billion to $1,097.5 billion, a 2.9 percent gain for the month and a 12.8 percent jump over the past year. Nonrevolving credit added $21.1 billion to come in at $3,441.5 billion, a 0.6 percent gain for the month and a 5.7 percent gain from a year ago. Revolving credit made up 24.2 percent of total consumer credit while nonrevolving accounted for 75.8 percent.

New Single-Family Home Sales Plunged in April as Prices and Mortgage Rates Continue to Rise

Sales of new single-family homes plunged in April, declining 16.6 percent to 591,000 at a seasonally-adjusted annual rate from a 709,000 pace in March and just slightly ahead of the 582,000 pace at the bottom of the lockdown recession. The April drop follows a 10.5 percent decline in March, a 4.7 percent fall in February, and a 1.0 percent drop in January. The four-month run of decreases leaves sales down 26.9 percent from the year-ago level (see first chart). Meanwhile, 30-year fixed rate mortgages were 5.3 percent in late May, up sharply from a low of 2.65 percent in January 2021.

Sales of new single-family homes were down in all four regions of the country in April. Sales in the South, the largest by volume, fell 19.8 percent while sales in the Midwest dropped 15.1 percent, sales in the West decreased 13.8 percent and sales in the Northeast, the smallest region by volume, sank 5.9 percent for the month. From a year ago, sales were up 17.1 percent in the Northeast but were off 12.4 percent in the West, down 25.5 percent in the Midwest, and off 36.6 percent in the South to the lowest level since December 2016.

The median sales price of a new single-family home was $450,600, up from $435,000 in April (not seasonally adjusted). The gain from a year ago is 19.6 percent versus a 21.0 percent 12-month gain in April. On a 12-month average basis, the median single-family home price is still at a record high.

The total inventory of new single-family homes for sale jumped 8.3 percent to 444,000 in April, putting the months’ supply (inventory times 12 divided by the annual selling rate) at 9.0, up 30.4 percent from April and 91.5 percent above the year-ago level. The months’ supply is at a very high level by historical comparison and is approaching peaks associated with prior recessions. The plunge in sales, high months’ supply, and surge in mortgage rates should weigh on median home prices in coming months and quarters. However, the median time on the market for a new home remained very low in April, coming in at 2.8 months versus 3.9 in March.

Housing Activity Shows More Signs of Deterioration

The selling rate of existing homes decreased 2.4 percent in April, to a 5.61 million seasonally adjusted annual rate. The selling rate is down 5.9 percent from a year ago.

The selling rate in the market for existing single-family homes, which account for about 89 percent of total existing-home sales, fell 2.5 percent in April, coming in at a 4.99 million seasonally adjusted annual rate, the first month below 5 million since June 2020. From a year ago, the selling rate is down 4.8 percent.

The single-family segment saw slowing sales in two of the four regions. Sales slowed 6.5 percent in the West and 5.6 percent in the South, the largest region by volume, while sales rose 3.7 percent in the Northeast, the smallest region by volume, and accelerated 4.2 in the Midwest. Measured from a year ago, sales were slower in all four regions (-11.1 percent in the Northeast, -8.3 percent in the West, -3.5 percent in the South, and -0.8 percent in the Midwest).

Condo and co-op sales slowed by 1.6 percent for the month, leaving sales at a 620,000 annual rate for the month, their slowest pace since July 2020, versus 630,000 in March. From a year ago, condo and co-op sales were 13.9 percent slower.

Condo and co-op sales were slower in two regions in April, -11.1 percent in the Midwest and -8.3 percent in the Northeast, but unchanged in the West and 3.6 percent faster in the South. From a year ago, sales were slower in all four regions (-19.4 percent in the South, -11.1 percent in the Midwest, -8.3 percent in the Northeast, and -6.7 percent in the West).

Total inventory of existing homes for sale rose in April, increasing by 10.8 percent to 1.03 million (the first result above one million since November) leaving the months’ supply (inventory times 12 divided by the annual selling rate) up 0.3 month at 2.2, the highest since October, but still extremely low by historical comparison.

For the single-family segment, inventory was up 12.3 percent for the month at 910,000 but is 7.1 percent below the April 2021 level. The months’ supply was 2.2, up from 1.9 in the prior month.

The condo and co-op inventory was unchanged at 118,000, leaving the months’ supply at 2.3, up from 2.2 in March. Months’ supply is 17.9 percent below April 2021.

The median sale price in April of an existing home was $391,200, 14.8 percent above the year ago price. For single-family existing home sales in April, the price was $397,600, also a 14.8 percent rise over the past year and a record high. The median price for a condo/co-op was $340,000, 13.1 percent above April 2021 and a record high.

Housing is likely to be volatile over the coming months as fundamentals adjust to changing market conditions. Increased opportunities for employees to work remotely are likely to impact demand while supply chain issues and labor difficulties impact supply. Furthermore, record-high prices and the recent surge in mortgage rates will likely push some buyers out of the market.

Robert Hughes

Robert Hughes joined AIER in 2013 following more than 25 years in economic and financial markets research on Wall Street. Bob was formerly the head of Global Equity Strategy for Brown Brothers Harriman, where he developed equity investment strategy combining top-down macro analysis with bottom-up fundamentals.

Prior to BBH, Bob was a Senior Equity Strategist for State Street Global Markets, Senior Economic Strategist with Prudential Equity Group and Senior Economist and Financial Markets Analyst for Citicorp Investment Services. Bob has a MA in economics from Fordham University and a BS in business from Lehigh University.

{kind=link}